The RBA’s occasional Statement of Monetary Policy is out and is making its way inexorably towards MB. Here is the money passage:

The forecast for the domestic economy has been revised to account for some developments working in different directions. Based on company statements and the Bank’s liaison, mining investment looks like it might decline more than was previously anticipated. Also, the appreciation of the exchange rate since the previous Statement means that the traded goods sector will be a bit more constrained than was envisaged at that time. Working in the other direction are the improvement in housing market conditions and the recent pick-up in measures of business and consumer confidence. The net effect of these developments is that GDP growth is now expected to remain below trend through next year, before picking up through 2015. The forecast for growth to pick up about a year from now is based on the stimulatory effect of low interest rates, the expectation that growth in Australia’s trading partners will be close to, if not above, average, further strong population growth and the need to add to the capital stock after a long period of subdued investment (outside of the resources sector). The recent improvement in sentiment, if sustained, bodes well for the willingness of businesses to invest and expand their operations.

With the economy expected to expand at a below trend pace over the coming year, employment is expected to continue to grow at a slower rate than the population. Accordingly, the unemployment rate is likely to continue to drift higher for a year or so, but is forecast to decline through 2015 as nonresource activity picks up.

Overall, the inflation outlook is little changed since the previous Statement. Inflation, on an underlying basis, is forecast to remain at or below the centre of the target range over the forecast period. This reflects slightly higher-than-expected inflation of late, offset by the effect of slightly softer labour market conditions on domestically generated inflationary pressures. Also, the depreciation of the exchange rate since earlier in the year is expected to push prices of tradable items gradually higher in coming quarters, but by slightly less than was expected three months ago.

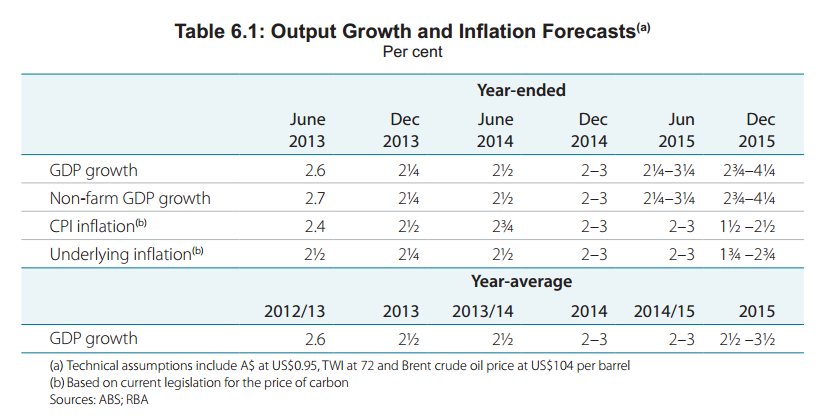

The key growth change was to cut 2014 growth to between 2% and 3% from 2.5% to 3.5%:

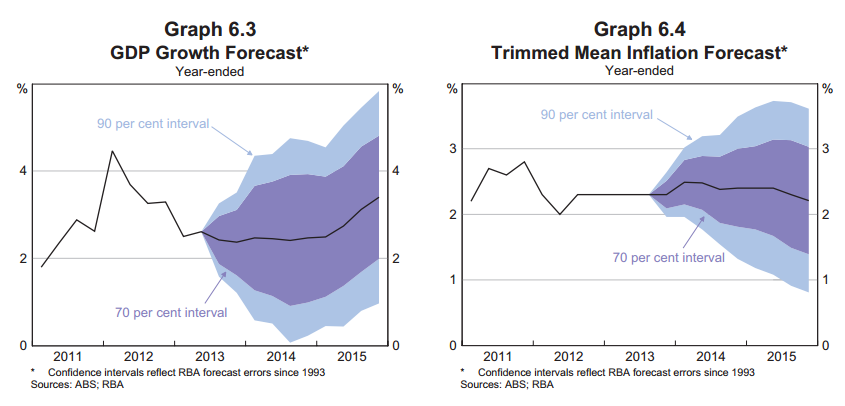

And the charts:

What colours this SoMP more than anything is extraordinary degree of uncertainty. The risks section is almost comical in its scope:

In China, after the authorities had signalled concern about the rapid expansion of financing earlier in the year, there was a noticeable decline in the extent of new borrowing. In August and September, however, growth of bank and non-bank lending rebounded.

It remains to be seen how sustained this rebound will be. A renewed effort to address the build-up of debt could slow the pace of borrowing and so some forms of economic activity. On the other hand, failure to contain the build-up of risks in the financial system may strengthen activity in the near term but presents risks to the economy further out. Policymakers also face challenges calibrating and implementing structural reforms: a program of significant reforms could raise the potential growth of the economy, but a failure to reform could constrain future growth.

Following the two and a half week partial shutdown of the US Government, there has been only a temporary resolution of the fiscal problems, with further agreement needed by early next year to continue funding government operations and increase the debt ceiling. While the most recent events appear to have had little impact on the ongoing recovery in economic activity, the potential for another shutdown or protracted debt ceiling negotiations could contribute to ongoing uncertainty for firms and households, and hamper the recovery. Moreover, uncertainty about the timing of withdrawal of the extraordinary monetary stimulus in the United States has increased. This has resulted in some substantial moves in financial market prices and sentiment. When expansionary monetary policy settings are eventually pared back in the United States, financial conditions couldtighten disproportionately in developing economies, with the possibility for negative effects on economic activity. How policymakers in these economies prepare for, and respond to, these possibilities will have a bearing on growth outcomes.

…For the Australian economy, there remains substantial uncertainty about the transition as mining investment declines and other sources of growth pick up. While the prospects for resource exports remain strong, there is considerable uncertainty around the forecasts for mining investment. This uncertainty manifested itself more recently with a reassessment of the prospects for coal investment. While there could be further cost overruns, there is little planning and development underway for new projects, which would suggest little upside risk to the profile for mining investment activity in the near term.

The forecasts encompass a recovery in non-mining business investment that is more muted than in past cyclical upturns. While this seems likely in the near term given current economic conditions and leading indicators, the low level of non-mining business investment in recent years, together with the freeing up of labour from mining investment projects and stimulatory financial conditions, could eventually see non-mining investment pick up at the faster rates seen in some past upturns. While a faster recovery would seem more likely if the recent improvement in business confidence is sustained, past experience indicates that it is very difficult to predict when such a strong cyclical upswing in business investment may occur.

If housing market conditions strengthen more substantially, the associated boost to wealth and sentiment could result in lower saving and stronger than-expected consumption growth. If this were accompanied by a return to increasing household leverage, it could raise concerns from the perspective of financial stability, although to date growth of housing credit overall remains moderate. On the other hand, there is a risk that households become more cautious in the face of slower income growth, resulting in weaker consumption growth.

The weak outlook for growth of public demand is consistent with the fiscal consolidation underway and that which is planned. The forecasts imply that growth of public demand over the next few years will continue to be the weakest seen for at least 50 years. It is possible that with below-trend growth in the economy in the near term, governments will not restrain spending growth to the extent assumed.

A significant uncertainty for the forecasts is the path of the exchange rate. The forecasts are, as usual, predicated on a constant exchange rate. The exchange rate appreciated significantly during the past decade as higher commodity prices led to a boom in mining investment. The higher exchange rateshifted demand toward external sources, so relieving pressure on domestic capacity to accommodate the substantial increase in mining investment. The decline in mining investment, even if commodity prices remain high, will result in a reduction in the capital inflow that has been funding that investment and a reduction in domestic demand, and so could well result in a lower exchange rate. A further depreciation similar in magnitude to that seen earlier this year could be expected to see growth return to trend, or even above trend, sooner than forecast and assist with the required rebalancing of growth in thedomestic economy. A depreciation of this size could also see inflation move into the top half of the target range for a time.

And I’ve edited out Japan and a discussion about local confidence. In other words, anything is possible.

Amid the fog, the Australian dollar fell 30 pips.