Morgan Stanley has a note out today that nicely captures a number of cross-currents in the economy, housing, and cyclical stock markets sectors:

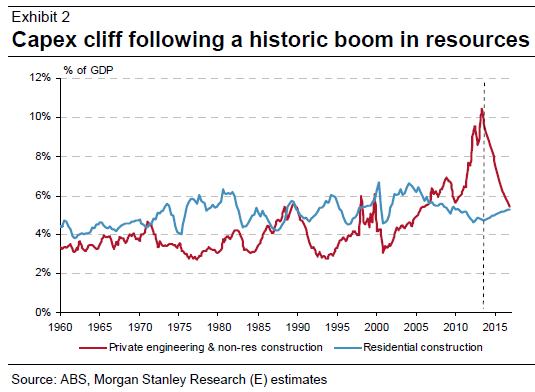

The RBA needs to transition the economy after an unprecedented resources investment boom, with the subsequent “capex cliff’’ likely to strip 1.5% points from GDP in CY14 and CY15. While a November 5 ‘cup-day’ cut looks unlikely, we note the RBA’s frustration with the AUD’s resilience and see these dynamics holding the cash rate at or below 2.5% for much longer than the market is pricing. This sets the scene for a sustained cycle in housing-linked activity to build.

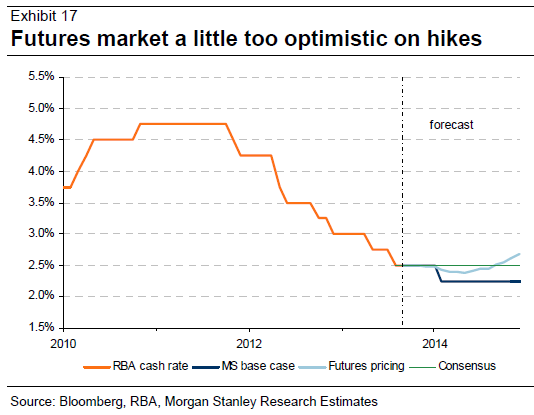

The RBA has already taken the cash rate to a record low of 2.5%, and we are out of consensus in seeing another cut to 2.25% in 1Q14 as odds-on. However, we see the length of the easing cycle as more important than the depth, with the RBA historically hiking rates nine months after the trough vs up to 21 months this cycle.

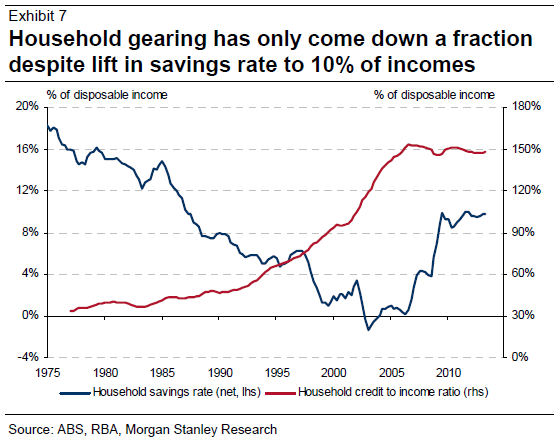

Leverage, the ‘cost of transition’: With the consumer likely to remain cautious and non-mining investment lagging, we focus on an interest rate-driven lift in housing activity and the potential for a publicly funded infrastructure program to provide pockets of growth in a sub-trend GDP environment. Importantly, we believe the RBA will tolerate some give-back of the recent improvement in household balance sheets as the cost of transitioning the economy without recession.

AUD attention: The RBA’s efforts to engineer a broader rebalancing with the help of a lower AUD have been thwarted by its bigger counterpart, the Fed, particularly following September’s ‘taper-later’ decision. AUD strength forces the RBA to cut further or hold longer.

This scenario indeed looks like a dream for housing-linked names – particularly those with leverage to NSW and QLD that have not seen a cycle sustained since the early-2000s.

Our base case is an optimistic one, and sees the combination of a kick start to the East Coast Recovery through housinglinked activity being transformed into a multi-year recovery (without an unsustainable house price boom) by a targeted infrastructure spend across Federal and State governments. However, like the REM song, we need to consider whether this outlook turns out to be ‘just a dream’. We see three risk scenarios:

1) Too hot to handle: With a surge in house prices forcing rate hikes, despite the aggregate economy remaining weak. We see this scenario as unlikely, as the optimism and activity required to generate a house price boom should itself generate associated activity through the real estate and housing-linked industries. The key to avoiding this scenario will be ensuring adequate supply of land and infrastructure, in our view.

2) No demand follow-through: Alternatively, a household deleveraging scenario would see little follow-through on the demand side, with the recent pick-up in supply pushing house prices lower, which in turn holds back investment appetite and keeps the consumer on a cautious tack (high savings). Weak income growth is the cyclical threat, given rising unemployment and an ongoing focus on productivity and competitiveness. Adding to this, demographics are an unavoidable headwind, with the baby boomer cohort heading into retirement, which strips away the tax benefits of negative gearing in their investment property portfolios, and should lead to net selling pressure in the housing market.

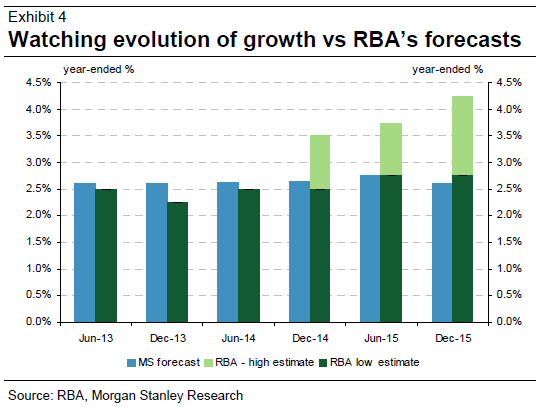

3) Broader success: A swifter recovery in the broader economy, combined with lighter than feared headwinds from the capex cliff could combine to see the RBA lifting rates sooner than we expect (e.g. in line with futures pricing). This would be a healthy scenario for the Australian macro outlook, but would be a risk to our rate view of ‘lower for longer’ and would make a multi-year recovery in housing-linked activity more reliant on supply reforms than interest-driven demand.

My own view is similar but with the added caveat that because the RBA will not want to see household balance sheets stretch very far there is a reasonable likelihood that macroprudential policy comes onto the radar. Basically I don’t think the Australian economy can lift credit growth very far before the major banks’ will have to start borrowing more money offshore and that’s red line for regulators (I think!). There is also the clear and present danger of an investor-led blowoff which comes at a much higher risk of financial instability than a genteel rise in household leverage.

This argument gives you an idea of how far some of the bubbly cyclical sectors in the stock market can yet run.

Advertisement

For me, then, the cycle is more like “moderate for longer”. But only so long as Sydney can be slowed. If not it’s boom and bust, my friends!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.