Recent reports released by the Grattan Institute and the Productivity Commission looking into the sustainability of the Federal budget as Australia’s population ages have generated some much needed debate on Australia’s retirement system, which is looking increasingly unsustainable.

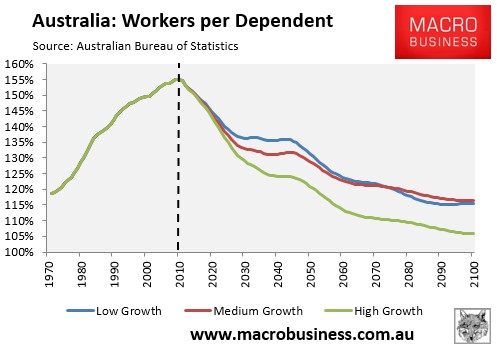

Just to recap, the Australian Bureau of Statistics (ABS) released it latest population projections earlier this week, which revealed that the proportion of workers supporting dependents peaked in 2010, and now faces decades of decline under each of the ABS’ population growth scenarios (see next chart).

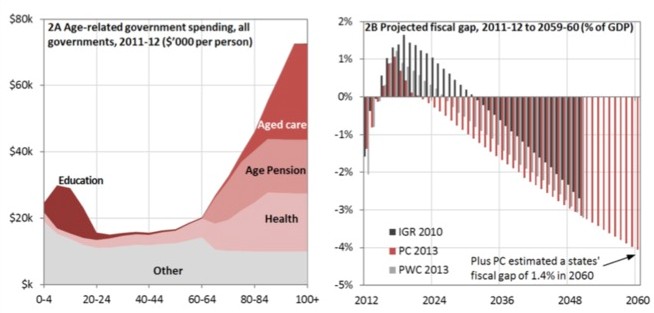

This shrinking of the tax base, along with growing health, aged-care, and pension costs is projected to push government budgets into deep deficit, unless fundamental reforms are made to the way that taxes are collected and entitlement spending (see next chart).

Now a raft of reform proposals have come to light, including amongst other things: lifting the retirement age to 70; including the family home in the means test for the aged pension; curbing superannuation concessions for higher income earners; and establishing a government-backed reverse mortgage market.

Today, professor of public policy at the ANU, Andrew Podger, has outlined further reform proposals in an article published in The AFR, including requiring superannuation to be taken as an annuity instead of a lump sum, and taxing superannuation when it is withdrawn rather than at the contribution stage:

…superannuation benefits continue to be dominated by lump sums so that individuals bear the risk of longevity, a risk the market has proven unable to manage. The government unwittingly protects people from the worst outcome of longevity by allowing them to get the age pension if their superannuation savings run out.

Another weakness is that the tax incentives for superannuation are poorly designed. They are too generous for high income earners. They are also overly complicated because they involve the opposite of the orthodox approach, which exempts contributions and taxes benefits…

Firstly, we need to direct superannuation benefits into lifetime indexed annuities, by helping the market manage longevity risk…

Age pensions would no longer be the default insurance against longevity – the individual’s own contributions would be used instead.

Secondly the excessive tax concessions should be curtailed. The Henry Report offers one solution based on retaining tax-free benefits (as required by his terms of reference). This involves taxing contributions at the individual’s marginal tax rate less about 20 per cent – leaving most paying the current 15 per cent, but high income people paying around 30 per cent, and lower income people no tax on their contributions.

A better option in my view, is to stop taxing contributions and to start taxing benefits in full as income – that is far more consistent with the concept of spreading lifetime earnings and taxing them when spent. It would also raise the tax on high income superannuants. This would avoid the need to impose artificial limits on contributions, including the suggestion by the Grattan Institute to lower the cap to $10,000, surely an obstacle to people taking advantage, when their children are no longer dependent, to accelerate savings in order to maintain living standards.

Requiring superannuation savings to be withdrawn as an annuity (income stream) rather than a lump sum is a sensible reform. Back in August, CPA Australia argued that a significant number of baby boomers are planning to run-up debts as they head towards retirement, and then withdraw their super as a lump sum to pay off debts and, rather than invest for income, spend most of the remainder on consumer goods or a holiday before falling back on the aged pension.

The existing system does, indeed, incentivise such behaviour, since it allows someone to retire at 60, withdraw their super tax free as a lump sum, use the money to pay-off their mortgage (with the family home excluded from the assets test) or consumption, and then go on the aged pension from 65 years.

Encouraging Australians to turn their retirement nest eggs into income streams so that they don’t run out of superannuation too early – either by burning through their retirement savings or living longer than expected – is, therefore, a positive step.

Indeed, some other nations discourage retirement savings from being withdrawn as a lump sum. For example, according to a recent report on The Business, the Dutch require all retirement savings to be taken as an annuity (income stream), whereas three quarters of retirement savings in the UK must be taken as an annuity.

However, a key problem in Australia is that there is a dearth of annuity-style products, and those that are available are typically inflexible or priced unattractively. Essentially, Australia’s superannuation system has been orientated around lump-sums, rather than providing a stable income stream in retirement, as it should.

As such, there is a potential role for Government. If the market is unable to provide suitable annuity-style options, then the Government should look to provide such a service, with the retiree handing over their funds for a guaranteed income stream. Such a system would likely be far more cost effective than having retirees blow their lump sums and then become reliant on the aged pension. A carrot-and-stick approach could also be adopted whereby superannuation lump sums are taxed, whereas annuities are concessionally treated.

Professor Podger’s proposal to tax superannuation when it is withdrawn rather than at the contribution stage also makes sense. It would overcome concerns about tax concessions overwhelmingly favouring high income earners and would allow workers to better smooth their incomes over their lifetimes.

The main problem with this proposal, however, is that it would be incredibly difficult to implement, since it would require a 180-degree change in how superannuation is taxed and open a Pandora’s box of concerns around double taxing of contributions already paid and grandfathering provisions, and would directly contravene the Government’s promise of tax-free super after 60. For these reasons, a simpler approach like offering a flat superannuation concession, as outlined in the Henry Tax Review, would be simpler.

In any event, the growing debate around retirement policy is welcome. With Australia’s population ageing fast, and the proportion of workers to non-workers set to decline significantly in the decades ahead, the Government will ultimately be forced to scale back entitlements as the tax base shrinks. Therefore, it is better to begin the reform process now rather than waiting until there is a Budget crisis.

unconventionaleconomist@hotmail.com