By Leith van Onselen Business Spectator’s new economics writer, Callum Pickering, has presented a rather confusing take on whether the Australian housing market is a bubble. On the one hand, Pickering argues emphatically that housing is not a bubble, since prices have moved in line with incomes over the past decade:

I don’t buy into the bubble narrative. House prices are high but they have moved in line with income growth over the past decade. House prices in Sydney, our most expensive city, are in real terms below their level a decade ago. Income growth over the next few years should ensure that the current level of house price growth will not be sustainable.

On the other hand, Pickering argues that Australia’s economy is dangerously exposed to housing:

The Australian housing market is worth over $4 trillion and housing debt accounts for over 90 per cent of all household debt and around 60 per cent of all household wealth. Our investment profile flies in the face of all investment advice. As a nation, our wealth is woefully concentrated.

To borrow a dreaded phrase, the Australian housing sector is ‘too big to fail’. The sector is a systemic risk to the broader economy…

We have experienced 22 years of uninterrupted economic growth, living up to our ‘lucky country’ moniker, but that will end eventually. It will be at that point that housing stops being a driver of growth and becomes a noose around our collective necks.

Realistically, all it will take for house prices to fall significantly is the underperformance of the non-mining sector over the next few years. The circumstances for this are already in motion, with the exchange rate ‘uncomfortably high’ and uncertainty surrounding the Fed’s taper. If the Australian dollar does not depreciation then we may face the most arduous economic conditions since the early 1990s and a housing market to match.

I don’t understand how someone can state that Australia is “woefully concentrated” in housing, that housing is “too big to fail”, and that it risks becoming “a noose around our collective heads” as the mining boom unwinds, and yet still maintain that housing is not a bubble? Surely if no bubble was present, then Australia wouldn’t have so much to worry about?

The problem, as I see it, is that Pickering is confusing Australia’s structural housing bubble – that is, the massive longer-term overvaluation relative to fundamentals like incomes, GDP, construction costs, and rents – with a possible cyclical bubble – that is, shorter-term trends in prices.

On the former, which is what commentators like Steve Keen, Phil Soos, Catherine Cashmore, and myself tend to focus on, I fail to see how Australian housing could not be viewed as being in a bubble. To highlight, consider the below long-run charts.

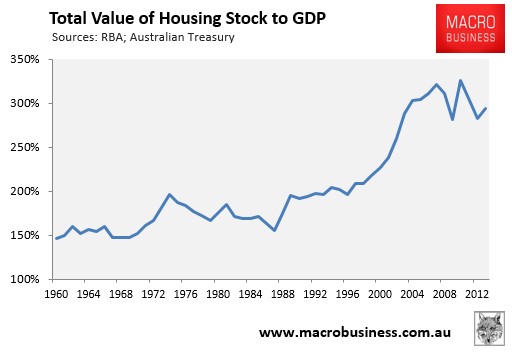

First, the value of the housing stock relative to Australia’s GDP:

Sure, there’s been no movement over the past decade, but what about the 50% uplift in the decade prior?

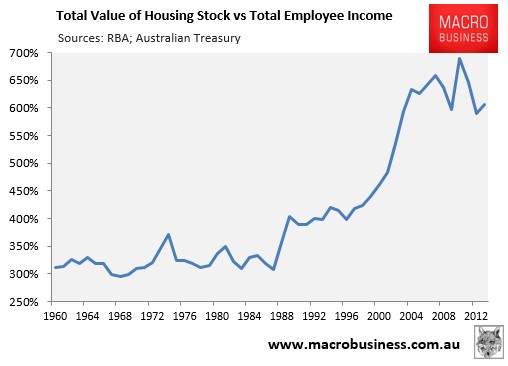

It’s a similar story with respect to incomes, whereby there’s been minimal movement over the past decade, but a huge uplift previously:

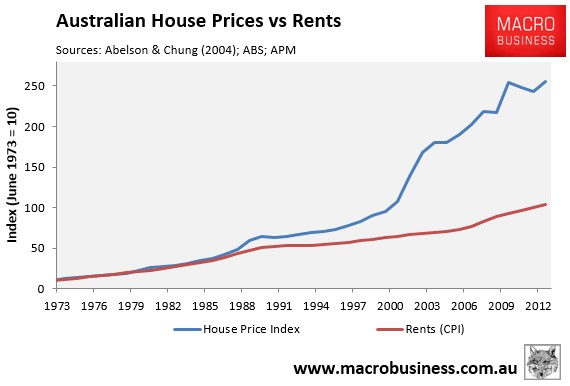

Finally, house prices have massively decoupled from rents, which also suggests significant overvaluation:

Put simply, focusing on the past decade only and then declaring there is no Australian housing bubble ignores the large structural overvaluation that has developed over the past 15 to 20 years. It also ignores the fact that housing values have been supported by the once-in-a-century commodity price and mining investment booms, which are unlikely to be sustained.

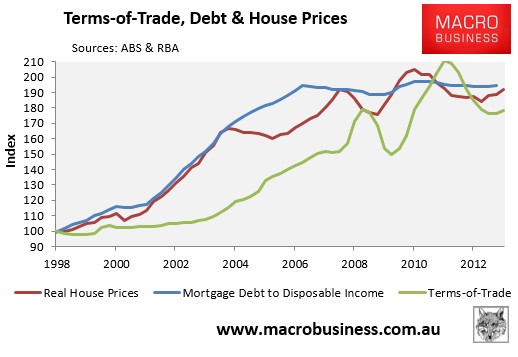

Arguably, the sharp rise in commodity prices and the terms-of-trade from 2003, complimented by the more recent mining investment boom, spared Australian housing from experiencing a significant correction. The extra disposable income generated from the commodity boom arrived just as the growth of mortgage debt was beginning to wane, enabling Australian home prices to remain stronger for longer (see below chart). So while rising housing debt was the key driver of Australian home prices up until 2004, strongly rising incomes from the commodity boom played the major role thereafter.

The flipside is that Australia risks a significant housing correction in the event that commodity prices experienced a protracted downturn brought about by the slowing Chinese economy or an increase in global commodity supplies. Such an event would likely cause a sharp reduction in national income, jobs and government revenues as the terms-of-trade deteriorates and planned mining investments are cancelled.

Judging by his comments above, Pickering clearly understands these risks, which is why emphatically declaring that there is no housing bubble appears inconsistent. For if there was no bubble, housing wouldn’t be “too big to fail” and a “systemic risk to the broader economy” should the non-mining sector underperform over the next few years.