Oh dear, that didn’t last very long:

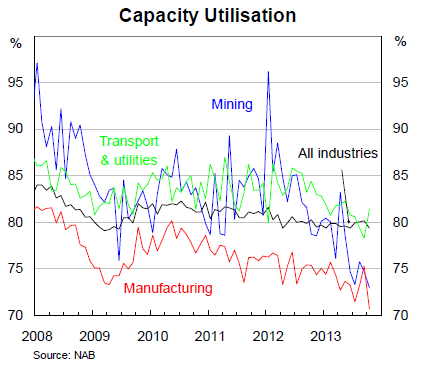

Firms reassess their confidence on the outlook as business conditions undershoot again. Capacity utilisation falls sharply – especially in manufacturing, construction, mining and retail – despite low interest rates and improved housing and equity markets. Other forward indicators deteriorate, paring back earlier gains and implying a continuing soft outlook for domestic demand. Price inflation outpaced by costs growth suggesting margins still tightening. Rate cut still expected in 2014 but – given RBA comfort with current settings – delayed till mid 2014. Unemployment key to how many cut(s) required.

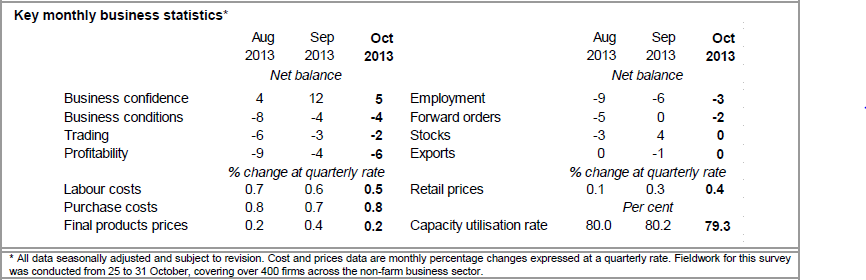

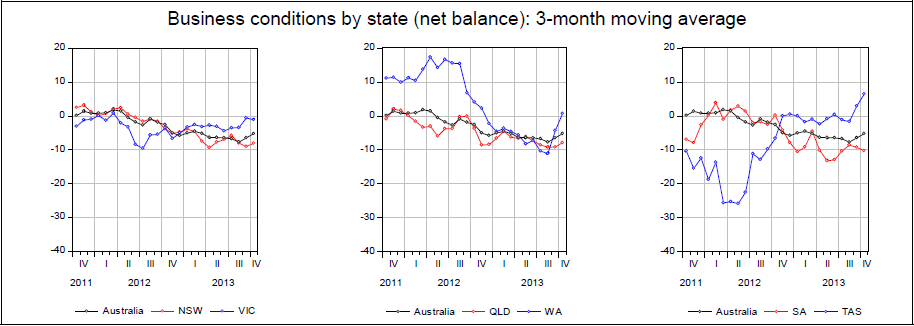

- Business confidence fell back significantly in October, partly unwinding the sharp improvement reported in the prior two months. Businesses may have reassessed their expectations about future activity in the changed political environment given the continued weakness in actual business conditions. Nonetheless, overall confidence remains relatively higher than the well below-average levels over the previous three years. That is, despite the reversal of the previous gain in confidence, low interest rates and improving asset market may still be helping. Transport & utilities and finance/ business/ property were especially confident, while wholesale was relatively pessimistic. Confidence levels were very similar across states, though lower in Victoria.

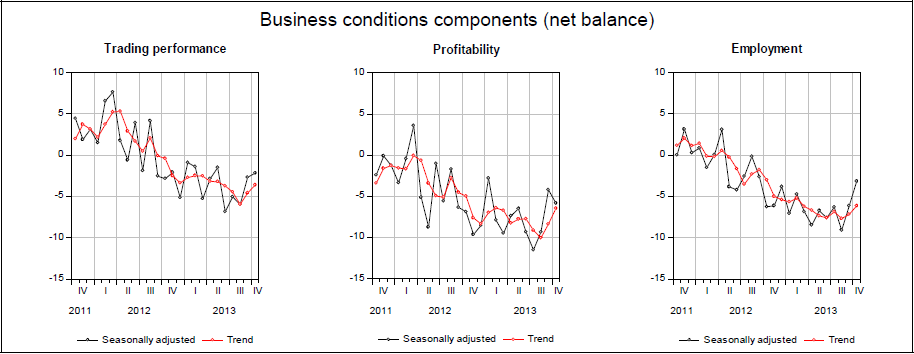

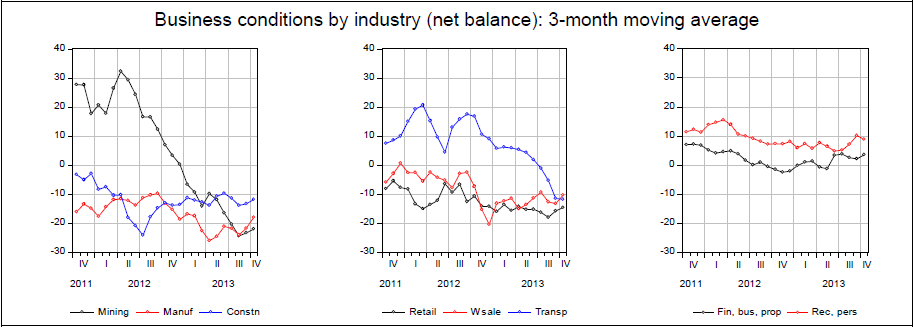

- Business conditions were unchanged at a lacklustre -4 points in October, though outcomes were somewhat varied across industries. Conditions in mining improved significantly, consistent with higher commodity prices, but they remained subdued overall. Elsewhere, conditions remained positive in recreation & personal services and finance/ business/ property but these industries reported a marked step down in activity compared to recent outcomes. Forward indicators do not paint a favourable picture for the outlook, with capacity utilisation falling to a four year low and the level of forward orders, capex and stocks also declining. While employment conditions lifted to a one year high, the index remained negative implying further jobs shedding.

- The survey implies underlying demand growth (6-monthly annualised) of around 2¾% in Q3 and GDP growth of around 2½%. Our wholesale as a leading indicator implies only a slight improvement in near-term activity.Labour costs growth continued to soften, consistent with the slack in the labour market, while purchase costs growth lifted a touch. Overall prices growth softened modestly in October, and when combined with relatively stronger cost pressures, this outcome suggests margins continued to tighten.

Here are the internals:

It’s not all bad. Employment is still up strongly, to only horrible levels:

But it isn’t going to improve unless the following two charts turn around:

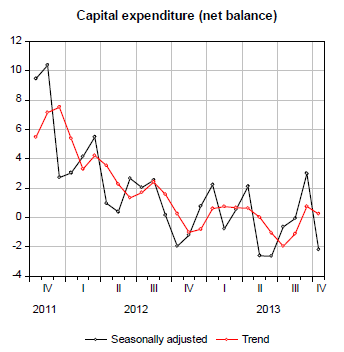

And they are unlikely to do so with the capex cliff steepening into next year.

Here’s some more charts:

This is a worrying report with a cyclical turn in place but with nowhere to go.