I’ve been resisting this story all day but have the report now and can say that I agree!. Goldman Sachs sees a weak Australian economy next year. From the SMH:

“Relative to the acceleration forecast in the global economy, in Australia we expect economic growth to decelerate in 2014, anticipate further easing required by the RBA, forecast additional fiscal drag and see a corporate sector set on a path of investment restraint,” Goldman Sachs analysts said.

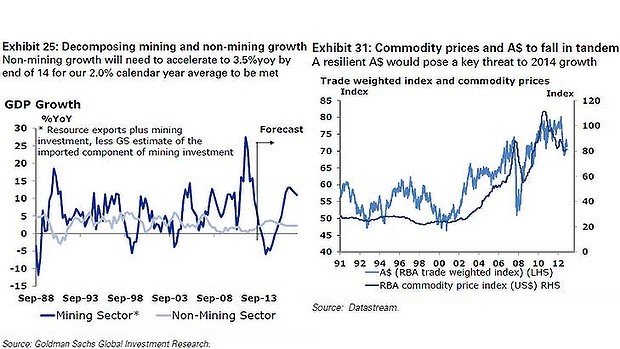

Despite the soft Australian outlook, the analysts said the recovery in the non-mining sectors of the economy had started and was expected to broaden and strengthen, “supported by historically loose financial conditions, an ongoing upswing in housing investment and near-term decline in the [Australian dollar] which should provide important support to corporate earnings”.

…A lower outlook for the Australian dollar as well as expectations of improving global growth would lead to 2014 financial year earnings growth of 9 per cent, and 10 per cent earnings growth in financial year 2015, Goldman Sachs analysts said.

“We see little room for further multiple expansion given stretched valuations and poor earnings momentum. We expect returns will skew to the second-half given Australia’s 60 per cent+ weight to defensive yield leaves it with taper risk,” the analysts wrote.

They continue to recommend being overweight on beneficiaries of a weak Australian dollar and improving economies in the US and Europe, on high-quality resource firms and in gaming stocks such as Crown’s.

They remain underweight on banks, and high-yield low-growth sectors such as REITs and utilities.

Regular reader will know that that is straight from my own playbook. What the story doesn’t report is that this is only half GS’s top trade for 2014 is long S&P500 and short AUD:

Advertisement

Core to both our economic and market views for next year, is that a US growth acceleration will materialize, with real GDP growth expected to reach 3.5% mid-year, and remain there for the duration of 2014…At the same time, we think the main case for US equities is that the gap between real bond yields and earnings yields remains unusually high, in an environment where recovery should continue to convince investors that the economic backdrop no longer justifies this.

…The ideal hedge against this risk would be a position that: a) is correlated with US/DM equities, b) that we expect to pay off even in our central case, and c) that is likely to perform better under scenarios in which US yields rise more rapidly. While there are several potential implementations for this “earn the risk premia, hedge the risk” notion, a short AUD position generally meets these criteria well.

I agree with both of these trades but for different reasons. I do not expect the taper. And if I’m wrong, completely expect a swift bond market unwind to hit US growth and necessitate more QE later in the year. Either way, US equities will love it as they move into the next phase of the bubble.

The Australian dollar will fall regardless in my view as China slows, local growth struggles (GS reckons 2%), the terms of trade keep falling, so does the capex cliff and the RBA’s is forced to wrestle with the wild thing it has unleashed in realty.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.