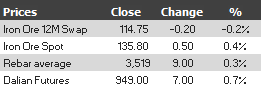

Find below the iron ore price table for November 4, 2013:

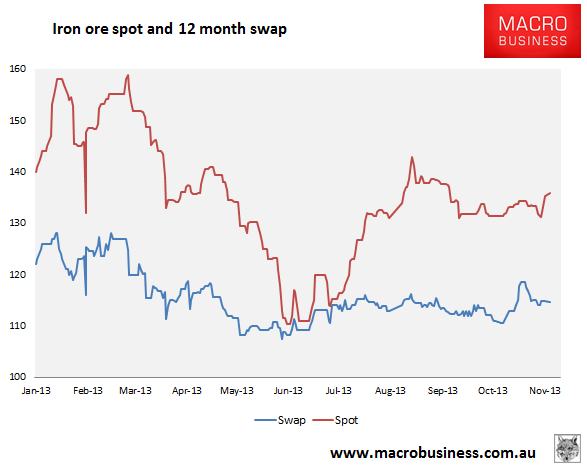

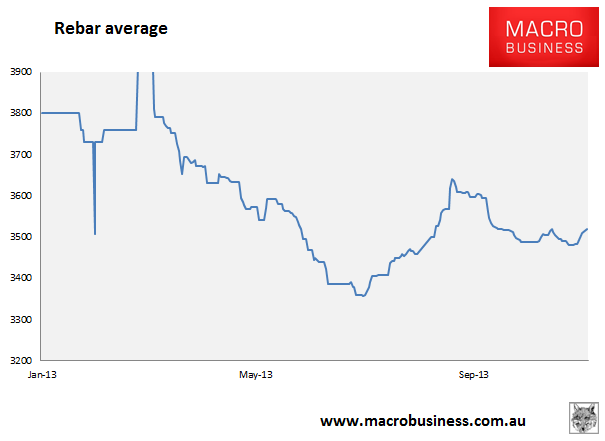

And the charts:

Rebar continues to recover and Dalian futures along with it. I think we’re beyond the seasonal destock window and headed into a year-end restock that will lift prices some, if not as powerfully as last year.

I am, in fact, lifting all of my forecasts for iron ore today. There are three reasons. Chinese demand remains robust enough to see off cyclical factors. Moreover, my take on the developing policy reform in China is that it will take quite a long time for it to diminish fixed asset investment dependence. Indeed, it looks to me like authorities will try to grow consumption more quickly rather than shrink investment overly.

Rumours and ruminations of hukou reform, boosting public housing to address affordability while allowing wider realty to flourish illustrate that China is not going to shift real estate development from its central place in its economic model any time soon. Infrastructure is certainly likely to fall as interest rates and banks are liberalised but it will take time for the net result to flow back to iron ore demand.

The second reason is that I’m of the view that the Pilbara cartel is proving a bigger factor in prices than I reckoned. My working model for the decline of the iron ore price has been the two coals. But both have a far wider distribution of suppliers and I think time is proving that to be a crucial factor. Basically I agree with the Chinese take on things, that as markets stand the Pilbara cartel can control prices to an extent. More so since the Chinese destocked their great iron ore hoard last year, prematurely. The last six months of spooky price stability around $130 is convincing in this regard.

The third reason is that although I still see a resumption of Indian iron ore exports, it’s clearer every day that the bureaucracy of that country has a hold on the miracle commodity and will let go only very slowly.

So, for next year, I’ve been viewing the iron ore price as likely to trade in an average price band from $90-$110, with downside risks. I’m going to add $10 to that today. I still expect ore to trade lower throughout the year as the supply deluge arrives in earnest and by late next year we may be in for some of the shakeout I’ve been tracking now for three years as the interests of the Pilbara cartel begin to diverge.