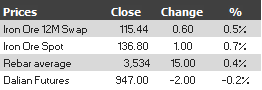

Here is the iron ore price table for November 5, 2013:

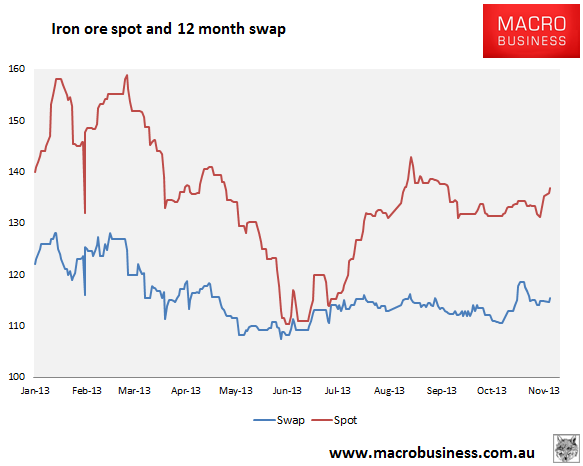

And the charts:

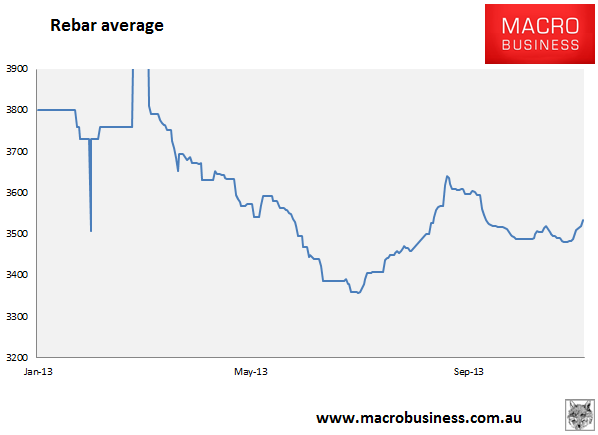

And rebar average:

Futures were down slightly. The Baltic Dry capesize index is ripping again.

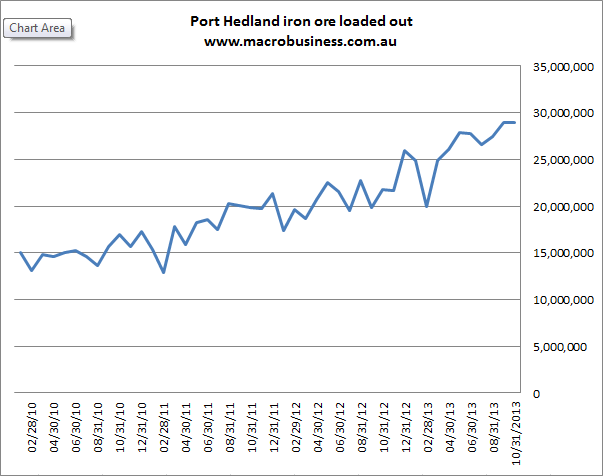

Port Hedland reported another huge month yesterday for ore volumes, down slightly MoM but up a massive 30% YoY:

Shipments to China were at a record 25.2 million tonnes.

In news, it’s all about the rally in miners. Though in reality, it’s all about the rally in just one:

From the SMH:

…the analysts at Macquarie, who are traditionally bullish about iron ore, wrote on Monday that Fortescue looks ”considerably cheaper” than BHP based on a price-to-equity ratio.

”Despite the 80 per cent rally over the past four months, we continue to see value in FMG,” they wrote.

Fortescue has a gross debt pile of $US12 billion, and the market has long debated whether the company will be able to service that debt over the next decade as iron ore prices gradually decline.

But Macquarie said Fortescue’s recovery over recent months had been so strong that the debate was likely to shift to what the miner would do with its spare cash, rather than the debt challenge.

The bonanza is not confined to the Pilbara, with South Australian iron ore exporter Arrium Limited closing at $1.45 on Tuesday, after fetching less than 70¢ in June. The company formerly known as OneSteel hasn’t tested these levels since the winter of 2011, when it was better known for its struggling steel assets than its growing iron ore business in South Australia.

When animal spirits attack!