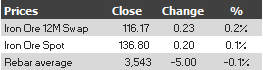

Find below the iron ore price table for November 15, 2013:

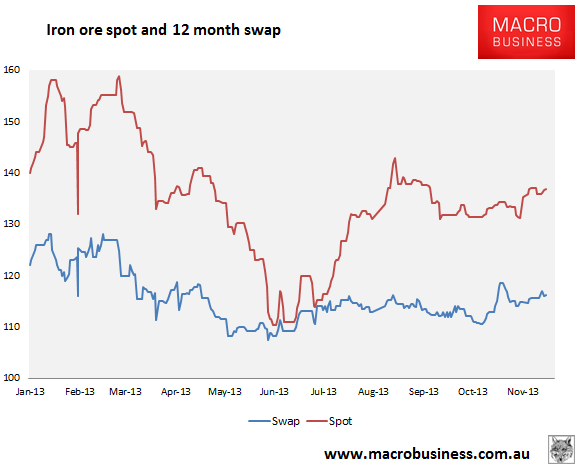

And the charts:

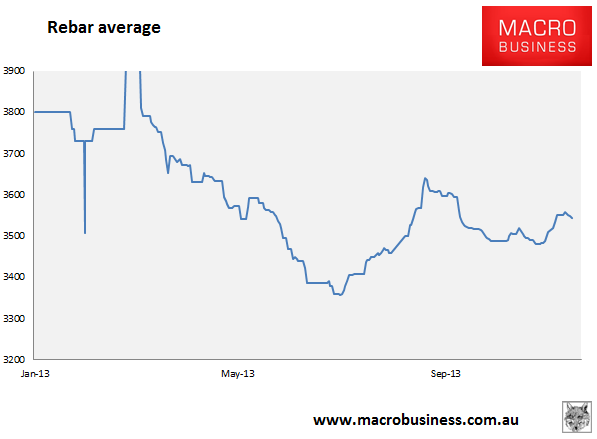

Rebar is rolling over. Futures have plunged and are threatening a new low:

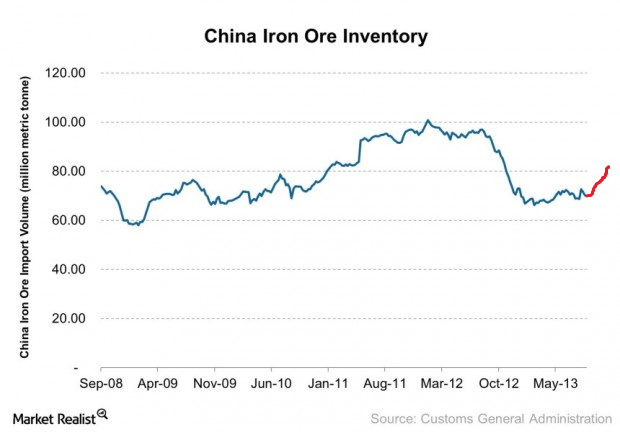

So, again, we have the dichotomy of weak fundamental demand and strong iron ore prices asserting itself. Some can be explained by renewed hoarding activity at ports. Last week saw port inventories jump again to above 80 million tonnes for the first time this year and the recent uptrend has been sharp:

But beyond these movements, the real problem has been overproduction. And on that front the Plenum was not kind. From the SMH:

The Chinese government’s decision to crack down on industrial overcapacity, especially in the steel sector, is most likely to have an impact on Australia’s iron ore industry, which exported $39 billion worth of ores to China last year.

”As China’s economy slowed, extra capacity became a major issue, one that the central government is now resolved to tackle,” the official Xinhua News Agency reported.

China’s steel industry, which collectively earned only 2.27 billion yuan or $397 million, for the first six months of the year is one of the worst-performing industries with a collective profit margin of 0.13 per cent. Under China’s new economic policy, Beijing will not prop up the inefficient steel sector with favourable policies such as subsidised electricity, water or land prices, and will demand consolidation in the sector.The State Council, China’s cabinet, issued orders to ban new projects, reappraise projects under construction and close down unauthorised or polluting production facilities.

Chinese local governments, whose support has been crucial to the steel industry’s survival, are likely to be challenged under the new market-centred economic policy. Zhao Zhenhua, an economist from the Central Party School, an influential think tank, said the excess industrial capacity was due to local interference.

”What appears to be overcapacity is in fact a revelation of blind competition among local governments,” Xinhua reported Mr Zhao as saying.

We’ve seen this all before but this time it does look serious. Any successful implementation will definitely cut demand for iron ore and concentrate buying power in fewer Chinese hands as well. On balance I also thought the broader reform package was iron ore neutral to negative depending upon implementation.

Lot’s of cross-currents in the market now. An end of year restock and rising hoarding are positives but falling steel prices and shifting policy are hefty negatives. With iron ore equities having enjoyed a very powerful rally I’d be cautious.