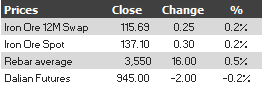

Find the iron ore price table for November 6, 2013 below:

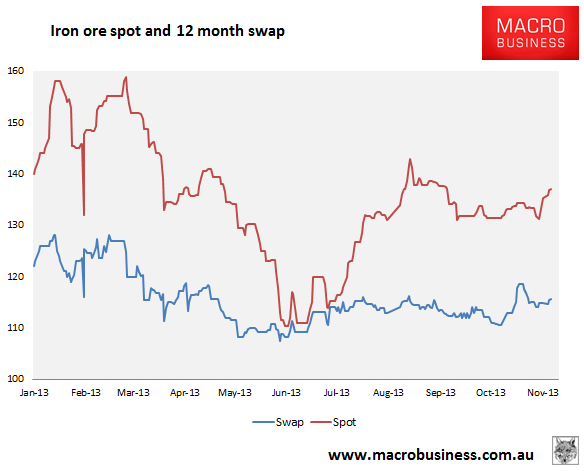

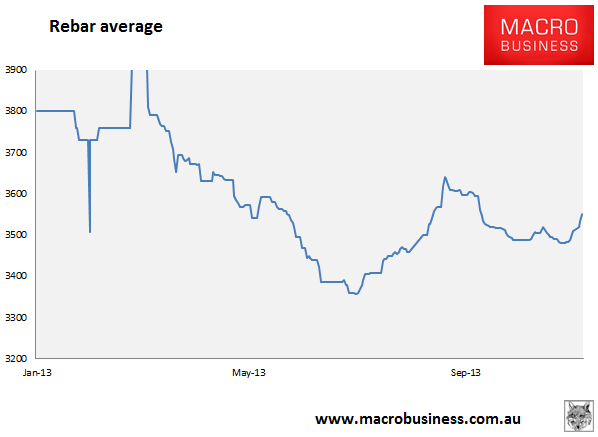

And the charts:

Rebar is looking impressive though futures have rolled over.

In news, India can’t get out of its own way:

The Indian government’s move to expedite the resumption of iron-ore mining in the western coastal province of Goa has come unstuck with the Supreme Court considering setting up fresh panels to look into various aspects of mining, including a cap on the volume of extraction.

According to the Supreme Court, two panels should be established: one to determine the environment’s carrying capacity for mining activities and the other to determine conservation of nonrenewable natural resources for future generations.

The court’s decision to undertake fresh studies effectively ends the federal and provincial governments’ hopes of resuming iron-ore mining in Goa within the next few months.

…In a related development, India’s Planning Commission was scheduled to hold a meeting on November 7, with representatives of various mining-related Ministries to address the issues plaguing the mining sector, including the ban on iron-ore mining and framing guidelines for approaching the courts on the issue before it.

Committees, injunctions, inquiries and no iron ore. Meanwhile, Australians take it to the bank in a graphic illustration of the success of capitalism:

Since June 30, the best performing top 200 Australian stocks have been Mount Gibson Iron, up 111 per cent, Arrium, up 93 per cent, and Andrew Forrest’s Fortescue Metals Group, up 92 per cent. In the same period, Australian iron ore prices have risen just 13 per cent, illustrating the surprise around the sustained price strength.

In dollar terms, Rio Tinto and BHP Billiton will be reaping the most benefits, but their size and diversity have diluted the effect on their share prices.

Since June 30, BHP is up 21 per cent, or $33bn, and Rio is up 25 per cent, or $21.7bn.

The strength in prices comes as a seasonal pullback in steel production usually seen in September and October remains absent.

“China has been restocking after record levels of iron ore imports over the past few months,” Deutsche Bank strategist Xiao Fu said.

“We expect the pace of restocking could slow. However, we are still below the 2011-12 (inventory) peaks, which suggests that the restocking cycle could last for another two or three months.”

I agree. The risk now, I think, is Q2 next year. That’s when the supply deluge proper hits and will coincide with an emptying Chinese infrastructure pipeline, which is depleting fast as we speak. Even a favourable outcome from the Plenum, that seems likely to endorse real estate development, will not prevent these pressures.