Canstar has come out with some rather dubious analysis today attempting to justify Australia’s high housing costs:

AUSSIE mortgage sizes may have quadrupled in the past few decades but experts say today’s borrowers are enjoying far better economic conditions.

New research by financial ratings firm Canstar found the national average mortgage size is 4.5 times higher than it was in 1990 – $305,000 compared to $69,100 – but current lower interest rates and increased wages have made housing more affordable.

The data showed the average wage for a male in 1990 was $28,407 compared to $70,569 – about 2.5 times higher – but repayments as a proportion of income were then 42 per cent, compared to the current 36 per cent.

And the average standard variable rate in 1990 was 17 per cent compared to just 5.95 per cent now.

Canstar’s research manager Mitchell Watson said the changed conditions have made mortgage conditions better now when comparing the average mortgage size and repayments as a proportion of income.

“Back then loan amounts were much lower, housing prices were lower as well but interest rates were extremely high compared to now,” he said.

“It did place further stresses on the household income than it did at this point in time.

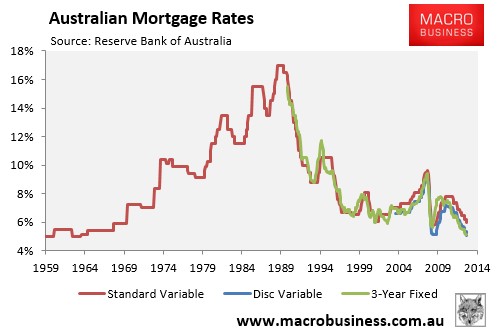

I hate this type of analysis. As you can see, Canstar has drawn its conclusion by comparing repayments on mortgages taken-out today against repayments during the period when mortgage rates were the highest in Australia’s history (see next chart).

This is misleading on a number of levels.

First, interest rates in 1990 did not stay at 17% for long and a home buyer back then got to enjoy the benefit of a massive drop in mortgage rates over subsequent years and a corresponding rise in house prices. Does anyone honestly believe that today’s first home buyer is likely to face similar conditions in the years ahead, whereby mortgage rates more than halve and values rocket?

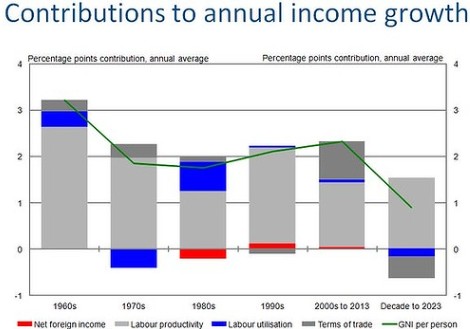

Second, as noted by the Australian Treasury last week, average income growth is expected to be the weakest in 50 years over the coming decade, which is going to make paying-off today’s mega mortgage more difficult (see next chart).

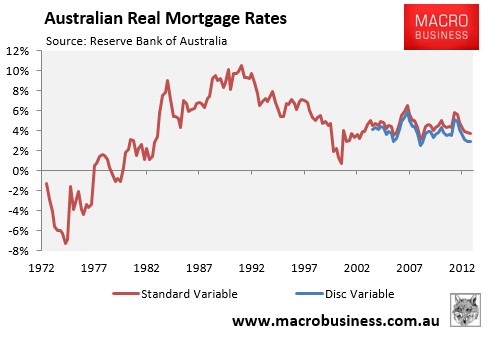

Third, when adjusted for inflation, real mortgage rates – 2.9% (discounted) as at September 2013 – are the lowest since late-2008 and the early-2000s, but well above levels that existed prior to the early-1980s (see next chart).

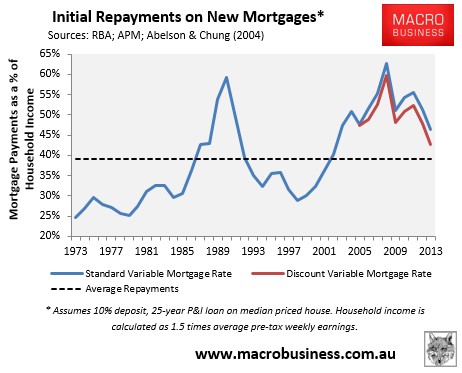

Finally, while initial repayments on new mortgages are lower than the late-1980s and early-1990s, they remain above the 40-year average (see next chart). Therefore, current housing conditions are hardly “favourable”, particularly given the coming shock to incomes.

What should also become clear from the above two charts is that the 1970s was a dream time to purchase a home (provided you qualified for a mortgage). Not only were homes highly affordable at roughly three times incomes, but a purchaser was in the fortunate position to have had their debts inflated away via high inflation and centrally indexed wage rises that outpaced the cost of credit.