From UBS today comes one of my pet hates about Australian household wealth:

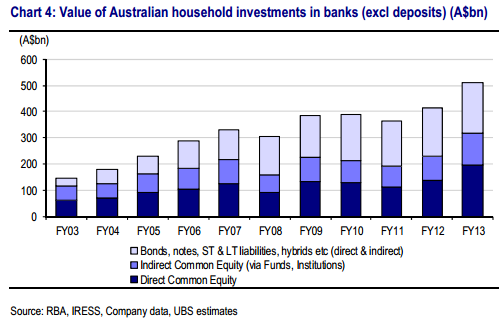

The Australian banks are large, very large. It is well known that all four major banks are in the top 20 global banks by market cap, and that the banks represent 30% of the ASX 200. But think about it from a household’s perspective. We estimate that total Australian household direct and indirect exposure to Aussie Bank securities (equity, hybrids, bonds, notes & short term debt) has now reached $500bn. To put this into perspective, this compares to $762bn in household deposits. Exposure to bank securities now represents 21% of all Australian household financial assets (excluding deposits) compared to 13% a decade ago.

While these statistics are an indication of the success of the banking sector over the last decade, it also highlights significant wealth concentration for many Australian households. Is it appropriate that ~21% of their net worth outside housing deposits is invested in four highly correlated banks? (Many households with direct bank equity holdings will be much higher than 21% of financial assets). Will this become an increasing concern for fund trustees and financial planners? Further, given the Australian banks are highly leveraged to the property market (~70% of all Australian bank credit exposures are to housing, construction, CRE or other financial services companies) on a look-through basis this further increases the concentration of household net worth to residential and commercial property.

There has been much discussion recently about APRA’s intentions to introduce additional D-SIFI capital requirements, with announcements expected by year-end. We consider the banks to be well capitalised. However, given the banks’ highly concentrated credit exposures, their privileged position within the economy and the significant exposure Australian households have to banks (loans, deposits, payments & securities) we view the debate around systemic importance as valid.

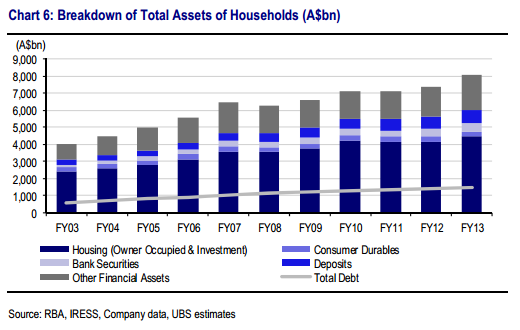

Strangely, what UBS does not note is that housing is also a bank-associated asset. And if we add it all together, banks and company constitute three quarters of Australian household assets:

Advertisement

In short, UBS has discovered the politico-housing complex. It concludes:

We believe that as superannuation fund trustees and financial planners review their portfolios, the large exposure to bank securities may become a concentration risk. We believe that this could potentially lead to some asset allocation recalibration away from banks in coming periods.

While many retail investors are reluctant to sell their winners or crystallise capital gains tax, concentration risk is a real issue that will need to be addressed over time.

This remains a concern, especially given investors’ desire for fully franked dividends. However, the answer is likely to be ‘everywhere else’, as portfolio are likely to be recalibrated and redistributed across the asset classes.

This is also more likely to be an issue for bank ordinary equity and hybrids than indirect investments in debt securities, especially as many baby boomers who are large bank shareholders approach retirement.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.