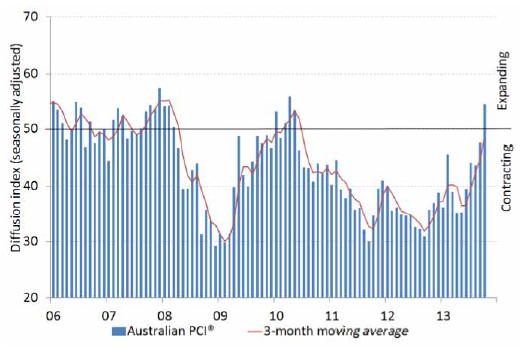

The national construction industry returned to growth in October 2013 for the first time in overv three years, driven by a higher rate of expansion in new orders and activity. In response, both employment and deliveries from suppliers increased after sustaining monthly contractions since mid-2010.

The seasonally adjusted Australian Industry Group/Housing Industry Association Australian Performance of Construction Index (Australian PCI®) increased by 6.8 points in October to 54.4 points. This was above the critical 50 points level that separates expansion from contraction and signalled the industry’s strongest performance since April 2010 (55.8 points).

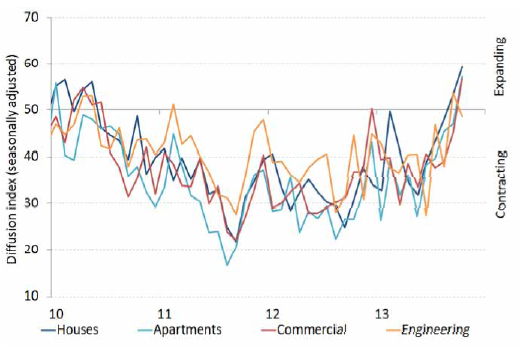

The upturn in October was underpinned by higher levels of activity across all four major sectors of the industry. Activity in the house and apartment building sectors increased solidly for a second consecutive month, with index levels for both sectors at their highest since the commencement of this survey in September 2005. These results are consistent with rising levels of new orders as reflected in the recent strong growth in total residential building approvals. In addition, commercial construction and engineering construction activity recovered in October, after continuous contractions for 39 and seven months, respectively.

Businesses reporting an improvement in activity generally attributed this to stronger levels of demand and an associated increase in tender opportunities. In addition, house and apartment builders noted that owner-occupier enquiries and buyer confidence were firming, with activity also benefitting from continued improvement in investor activity. However, the operating environment clearly remains tough for many businesses, with impediments such as tight credit conditions and a lack of public sector building works cited as the main constraints on activity.

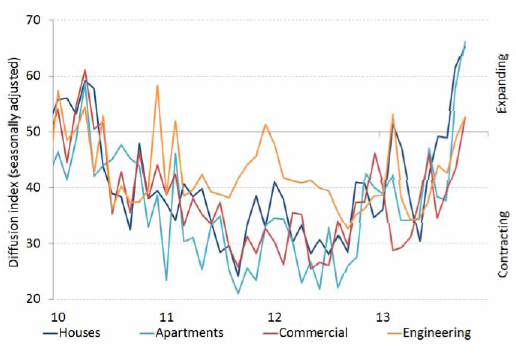

The components show an interesting mix in which engineering orders are still not declining but dwelling orders are pouring it on. The first chart is for activity and the second for new orders:

Advertisement

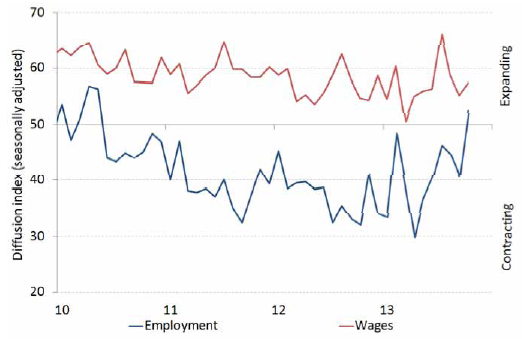

Most importantly, employment has surged into the positive:

It’s up, up, up across the board:

Advertisement

This is a red hot release that shows the RBA has finally gotten some rebalancing going before the worst of the capex cliff kicks in. I still don’t think it will be enough but it offers hope. Charlie Aitkin and cyclicals to the moon!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.