The SMH has a brief quote from Barclays today which is useful:

So how many times has the RBA intervened in recent years? The most recent intervention, at least one that the RBA has officially acknowledged, was in 2008 during the financial crisis, says Barclays chief economist Kieran Davies.

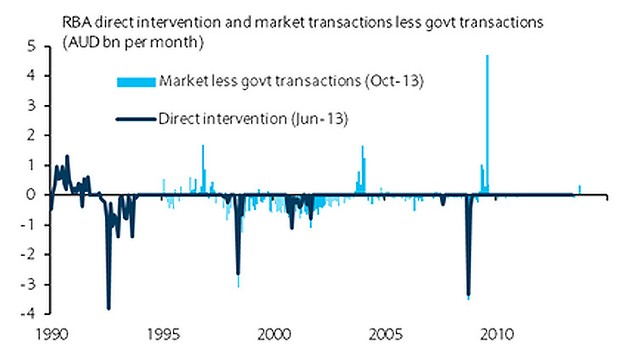

In 2008, the central bank bought $3.7 billion during the global financial crisis. In 2007, it also bought $300 million.

“This intervention was an attempt to calm disorderly markets, where the bank was trying to ensure the depreciation of the exchange rate at the time was orderly, without “excessive price gapping’,” Davies says.

Unofficially, the RBA is also believed to have intervened in FX markets in 2012, when it accepted an estimated $1 billion deposit from another central bank.

Davies adds that as Stevens has been at pains to stress the Reserve Bank has not undertaken large-scale intervention, the central bank may have made small-scale ones.

“In this respect, the RBA’s monthly data on its FX transactions suggest the bank could have intervened by selling $300 million in October. … The RBA has said that reserve rebuilding transactions are ‘designed’ to avoid influencing the market, but presumably in current circumstances the bank would be pleased if such transactions helped push the exchange rate lower and gave the market the impression it was intervening.”

Note the bank has never sold dollars in volume since the float, only bought them. It has been far too busy fighting the last war for two years now. The SMH went on:

The RBA itself has analysed this issue and said that any impact was very hard to pin down and that it could be short-lived and sometimes counter-intuitive, Davies notes:

For example, the RBA found that selling $1 billion was actually associated with a 0.7 per cent appreciation of the exchange rate the next day.

However, intervening over more than one day had the desired effect, with a $1 billion sale lowering the exchange rate by 0.5 per cent.

Given the size of FX markets nowadays, analysts say any intervention could be too small to effect any meaningful change.

In February, New Zealand’s Finance Minister Bill English said he would not risk using the country’s limited funds to intervene to lower the strong dollar.

”We just don’t want to take that kind of risks. We are a small country,” English added. ”We’ll be out in the war zone with a peashooter.”

Advertisement

Sure, but Bill English has also had the foresight to force local planning reforms to de-bottleneck housing as well as support the RBNZ’s installation of macroprudential tools which will definitely lower the currency over the long term.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.