Followers of iron ore markets will recall that following last year’s September price collapse, a huge rebound in prices transpired through the Oct-Jan period. Last year’s cycle was more exaggerated than normal but the pattern is familiar. Most year’s Chinese steel mills destock iron ore in Q4 as the winter months slow construction activity and steel production slows.

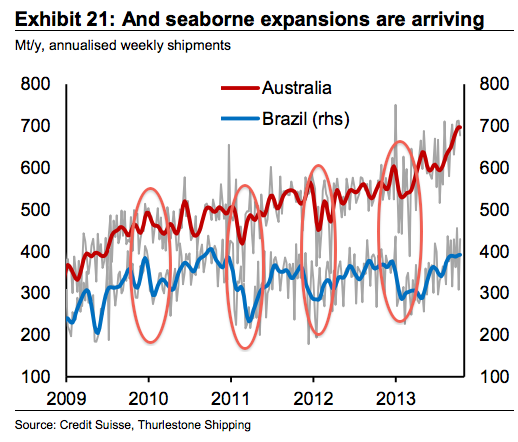

A second factor then plays into the subsequent restock. The early months of the new year are peak cyclone seasons in the Pilbara and in Brazil and the resulting disruptions to shipping mean mills like to stockpile raw materials to an extent. This is very apparent in shipping stats, chart from Credit Suisse (my circles):

The final factor in the cycle is Chinese mills then rebuild steel stocks in the early months of the year as demand returns.

So, if the same runs its course this year, will we see a price spike? CS doesn’t think so because steel mills already “have already built imported inventory to 30 days cover”, steel production should ease back, domestic ore is readily available and Australian expansions are rolling out.

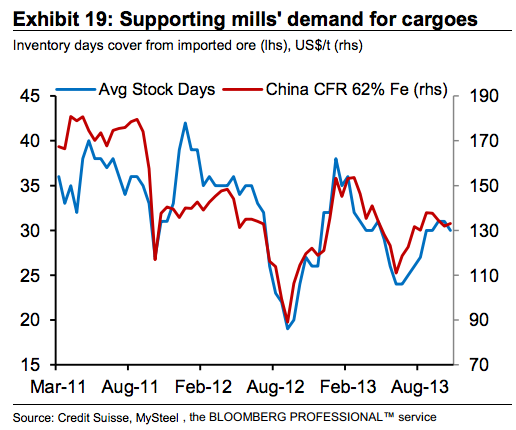

Here is where mills’ stocks are at now:

You will note that previous early year restocks have peaked at or close to 40 days so if the pattern is repeated then we will see increased demand. Mac Bank still sees the price spike coming and I’ve been scared into thinking it might be imminent by the recent jumps in the swaps market. The CS argument makes plenty of sense provided the restock is modest but I still think price firmness into year end is probable.