That is the question! Morgan Stanley addresses it today:

Consensus price forecasts are overly bearish. The average price of US$136/t (62% Fe, CFR North China) in the iron ore spot index between 1Q-3Q 2013 surpassed even the most bullish of analysts’ forecasts. Both supply and demand fundamentals helped support the strong price performance, and we think similar conditions will continue, at least into the first half of next year. Nonetheless, consensus forecasts, at US$108/t, remain well below the current level and our expectations.

Although we believe market concerns over price into 2014 are warranted, they are overly pessimistic. Indeed, supply growth is coming, and we have factored in nearly every tonne the key suppliers have guided over the next two years. We have also included a return of Indian exports over the next two years, albeit modest. On the demand side, we forecast very conservative growth in 2014 Chinese steel demand, +3.1%, to 779Mt. Outside of China, we believe steel output growth will see its best year since 2011, led by modest rebounds in production in India, East Asia and North America.

Market tightness through 1H14. Based on the above assumptions, we forecast a continuation of the current apparent seaborne market deficit well into next year. As a result, we’ve given moderate upgrades to the 1Q14 and 2Q14 forecasts, to US$130/t and US$120/t, from US$125/t and US$117/t, respectively.

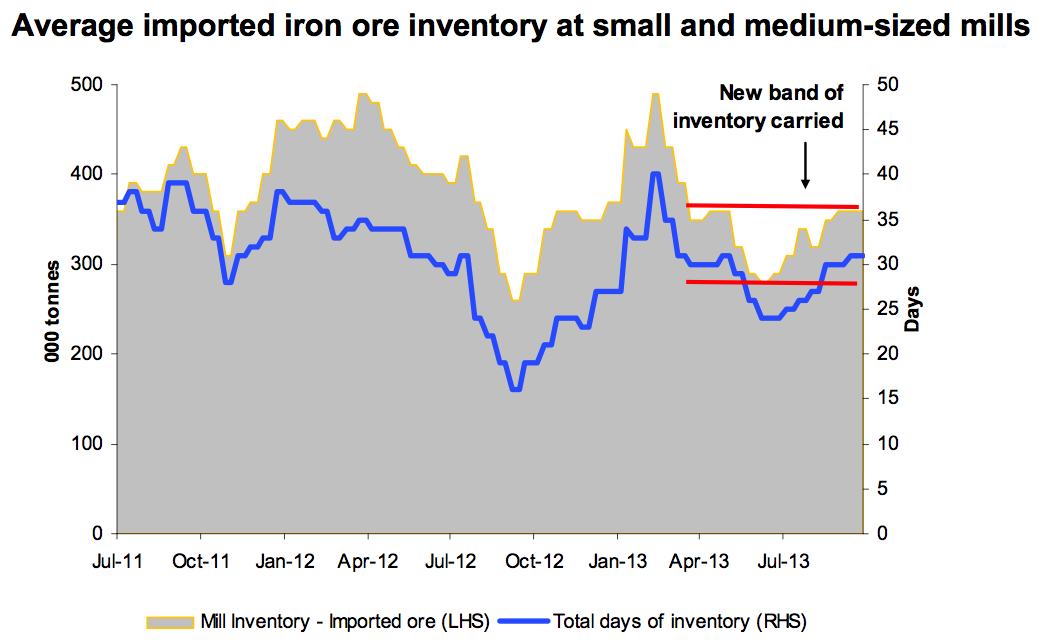

The spot iron ore index has been remarkably less volatile in 2013.Compared to the roller coaster ride in 2H12, the spot iron ore price index in 2013, as well as Chinese domestic steel prices, have swung less dramatically. In 3Q12, the iron ore and steel prices experienced sharp declines after steel mills went on a “buyers strike” by severely limiting spot purchases of iron ore for a matter of weeks while inventory levels were high (note the July-Oct 2012 period in the right-hand side chart below).

We believe the primary reason the price has been less volatile this year is because steel mills are carrying a much lower level of iron ore inventory. As a result, their ability to both destock (or deliberately withhold purchases) and restock has been limited. The decision to carry less inventory has been strategic and market driven: Strategic in the sense that Chinese steel mills have had restricted cash flow availability and tighter balance sheets as a consequence of centrally driven credit restrictions. Market driven in the sense that any industrial user of commodities tends to run with less inventory during periods of price volatility.

As a result, we believe Chinese steel mills will carry 25-35 days of iron ore inventory, on average, going forward.

I would only add that mills are also running leaner supplies for two more reasons. Their margins suck as they overproduce and they know oversupply is coming so why stockpile?

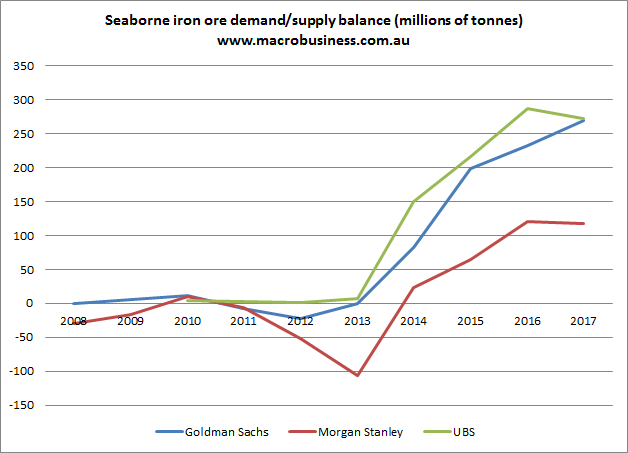

Here’s my up dated supply balance chart in which MS has suddenly opened a large gap with others:

Advertisement

My view is unchanged. Plenty of supply coming, demand growth to remain low and a deteriorating price all next year.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.