In the end, economics is not rocket surgery. The overnight news from the US confirms that its housing market has hit the interest rate wall. From the NAR:

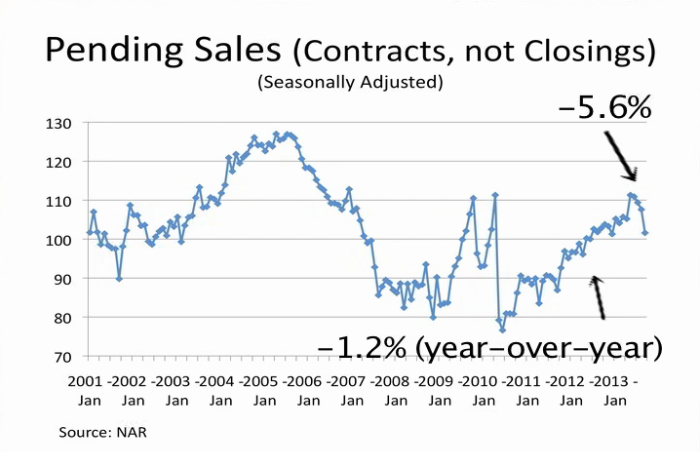

The Pending Home Sales Index,* a forward-looking indicator based on contract signings, fell 5.6 percent to 101.6 in September from a downwardly revised 107.6 in August, and is 1.2 percent below September 2012 when it was 102.8. The index is at the lowest level since December 2012 when it was 101.3; the data reflect contracts but not closings.

…The PHSI in the Northeast dropped 9.6 percent to 76.7 in September, and is 6.4 percent below a year ago. In the Midwest the index fell 8.3 percent to 102.3 in September, but is 5.7 percent higher than September 2012. Pending home sales in the South slipped 0.4 percent to an index of 116.2 in September, but are 2.0 percent above a year ago. The index in the West dropped 9.0 percent in September to 97.3, and is 9.8 percent lower than September 2012.

Total existing-home sales this year will be 10 percent higher than 2012, reaching more than 5.1 million, and are likely to hold even in 2014. The national median existing-home price is expected to rise 11 to 11.5 percent for all of 2013, but moderate to a 5 to 6 percent gain in 2014.

As I’ve said before, I do not expect a crash, though there is a risk that the all-cash buyers of Wall Street will pull out as returns decline.

But the stall will mean lower economic growth. Inevitably, household spending growth will slow and it has been the largest growth segment of the Us recovery, especially lately:

Advertisement

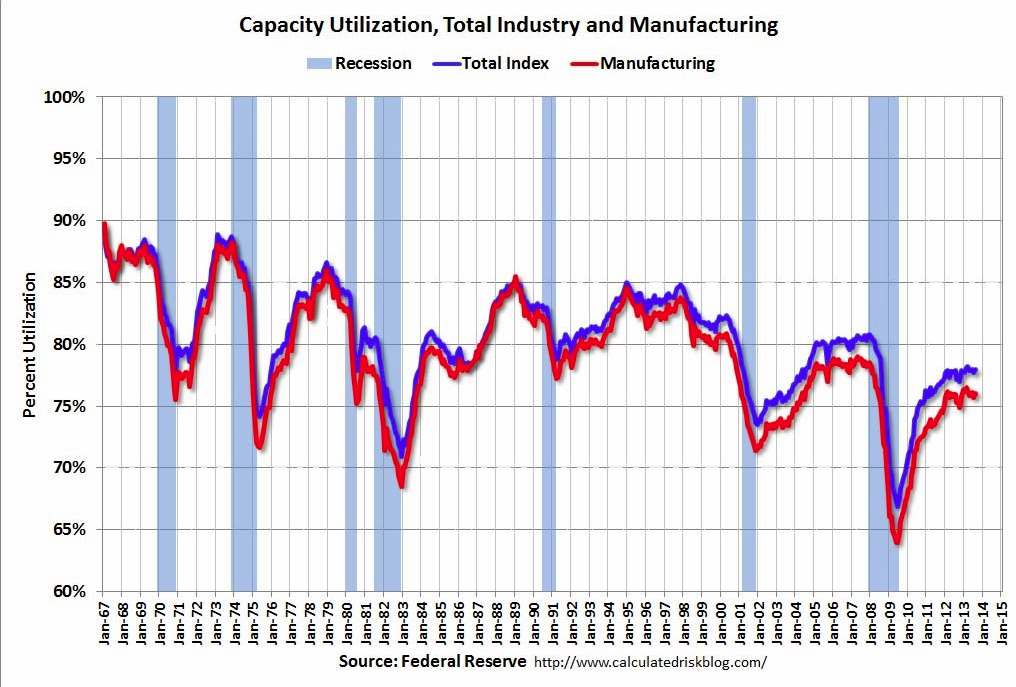

Don’t get me wrong. I do not expect the US to suddenly slump and its housing construction rebound should continue at a reasonable if muted pace. And there was more promising data in Industrial Production numbers which beat and climbed firmly. From Calculated Risk:

Industrial production increased 0.6 percent in September following a gain of 0.4 percent in August. For the third quarter as a whole, industrial production rose at an annual rate of 2.3 percent. Manufacturing output edged up 0.1 percent in September following a gain of 0.5 percent in August, and increased at an annual rate of 1.2 percent for the third quarter. Production at mines moved up 0.2 percent in September and advanced at an annual rate of 12.9 percent for the third quarter. The output of utilities rose 4.4 percent in September following declines in each of the previous five months. The level of the index for total industrial production in September was equal to its 2007 average and was 3.2 percent above its year-earlier level. Capacity utilization for total industry moved up 0.4 percentage point to 78.3 percent, a rate 1.9 percentage points below its long-run (1972-2012) average

Advertisement

Capacity utilisation at these levels means little income growth but at least it’s stable.

In my view the US has already recovered and this 2%+ growth is the new normal. It does not suggest any imminent change to QE.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.