House prices up (well, in Sydney anyway), stocks at cyclical highs, iron ore hanging in. Time for a dose of Charlie Aitken, now approaching lunar orbit:

Goldilocks meet Santa

Every night I read a fairy tale to my little daughter. I try to avoid the Brothers Grimm as their stories are pretty grim. Who leaves their kids in the woods! Twice!

My daughter’s favourite story is Goldilocks & the three bears. We must have read it 100 times. I asked her the other day what the moral of the story was and she said “the bears are big and slow”….

I am not so sure that is the moral of the story but my gut tells me equity market investors are in for a fairy tale ending to 2014. In strategy terms, I am calling it Goldilocks meet Santa.

While there are always unpredictable events in markets, the unknown unknowns, if I look at the known knowns from now until Christmas I am genuinely struggling to find a serious speed hump ahead. In fact, we could easily see a blow-off upside move, led by Wall St, as professional investors scramble to look more invested and shorts are forced to cover.

Let’s start with the top down global macro drivers the work into the micro.

Central Banks: taps turned fully on

The recent circus in Washington pretty much ensures the FED will have to delay tapering bond purchases until Q1 2015. The BOJ is fully deployed while the BOE is also maintaining a strong pace of bond purchases. Between them the major central banks will be buying $150b of bonds per month globally and those who sell the central banks $150bi of bonds per month will redeploy those funds into risk assets, but most likely equities.

In Australia, the AUD/USD cross rate bouncing due to the delay of Fed tapering ensures the RBA can’t raise rates despite stronger domestic data. In fact, the AUD/USD bounce will force the RBA to increase jawboning against the AUD and further emphasise their easing bias.

The overall point is central banks are going to remain in fully accommodative mode until year end.

Politicians: off the front pages

No offence intended to any political leaders who read these notes, but when you guys aren’t on the front pages the markets go better. In an Australian context if a political leader is on the front pages from this point it should be either repealing a tax on growth (Carbon, MRRT) or announcing a growth initiative. Other than that, be quiet and confidence will improve. We want Australian’s to talk about house prices, not politics.

Global economic data: improving

I expect data from China, Eurozone, UK and Australia all to show continued recovery growth and unemployment recovery in the months ahead. The US data will show a pause due to the government shutdown, but that’s an aberration.

In an Australian context you can sense Chinese data prints are going to be stronger, confirming the low point of Chinese GDP growth is behind us. This will be occurring alongside clear evidence of Australian East Coast economic data turning up.

I also expect Australian house prices to keep rising into year end, with 80%+ auction clearance rates to continue. I remain a bull on Australian retail sales in the crucial Xmas selling period.

Commodity Prices: rebounding

While WTI Oil prices have peaked as some of the political tension premium comes out (Syria, Iran), and that is effectively a tax cut for the world, the prices of other industrial commodities will continue to advance.

Iron ore, copper, coking coal and US natural gas all look good into year end and I expect to see consensus analyst upgrades to that suite of commodities into year end.

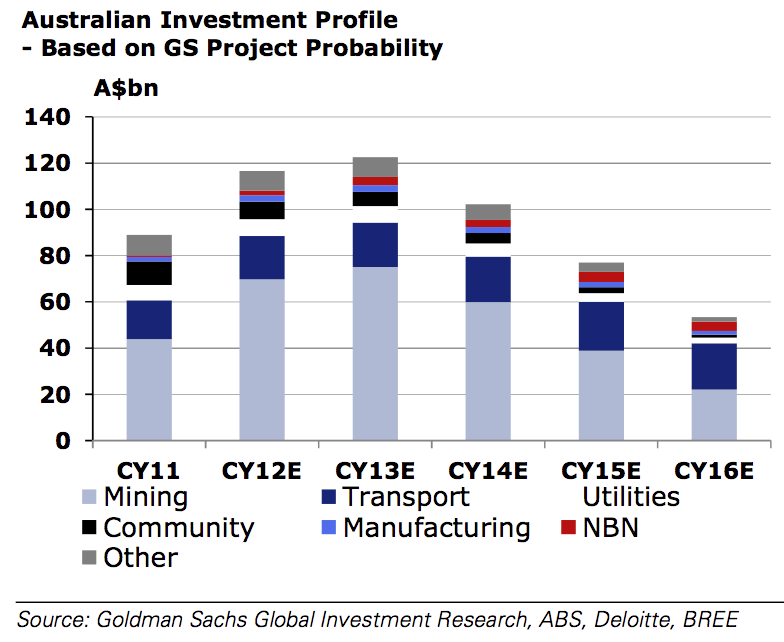

Of particularly relevance to Australia is the iron ore price. With less than 2.5 months to trade this calendar year the chances of seeing spot iron ore prices at the much hyped “$70” price appear zero. In fact, it appears to me that seaborne iron ore is taking a greater share of the Chinese domestic iron ore market and the spot iron ore price should be closer to double the $70t target price of the commodity forecasting dart throwers.

This is pretty simple: Australia is producing greater volumes of iron ore into the seaborne market and the price is gently rising, not collapsing as so widely expected. The Chinese aren’t using this stuff for landscaping gardens and I suspect one of the biggest features of the final qtr. of 2014 will be a series of upgrades from iron ore forecasters. That will lead to major consensus FY14 upgrades for Australian miners and Australian GDP growth.

Equity earnings: upgrade cycle

Yield curves globally continue to point to a cyclical growth recovery, particularly in Australia. However, consensus analyst forecasts for cyclical companies, particularly in Australia, remain very timid. It appears cyclical analysts wait for hard data or hard earnings confirmation to upgrade their forecasts. Obviously this is not how to add value in cyclical stocks.

I also believe that coming out of a 5 year down cycle that cyclical earnings, dividend and free cash flow are underestimated. Cyclical companies are running costs very close to the bone. As prices and volumes pick up, and costs remain strongly contained, we will all be pleasantly surprised at the leverage these cyclical stocks deliver.

I expect to see consensus upgrades to all forms of Australian East Coast cyclicals, banks, market linked earners, tourism, TMT, and big miners into year end. Then we will all realise the ASX200 isn’t trading on “17x FY14 earnings” that the bears so regularly spurt out.

M&A: picking up

Mergers and acquisitions have been the missing piece of the equity market rally. However, I expect to see that all important piece start arriving into year end. Boards get FOMO as badly as investors and you will see Boards start to deploy some risk/growth capital via M&A.

The threat of takeover activity is an important support factor in a bull equity market. It plays havoc with the minds of shorters.

M&A also delivers windfall profits to shareholders that then get reinvested. It’s a very important factor in a sustained bull equity market

Buybacks/special dividends: picking up

Another way of Boards expressing FOMO is via accelerating stock buyback programs and/or paying out excess cash via special dividends. Most companies globally and locally are under-geared and can generate EPS positive outcomes via buying back stock. In an Australian context the majority of Australian companies are holding excess franking credits which in reality belong to shareholders. I expect more of those excess franking credits to find their way to shareholders via special dividends.

Shorts: more pain ahead

2013 has been, in Queen Elizabeth’s words, an “annus horribilis” for shorters, globally and locally. I expect that to continue. I continue to believe it’s a legitimate investment and trading strategy to target large, stale, open short positions. As I have written before, it’s like watching one of those National Geographic documentaries where the herd turns on the predator.

In Australia, shorter’s have gotten pretty much nothing right. In fact, they have mostly been spectacularly wrong. Australia is the “Killing fields” for shorters and as GDP growth recovers I expect that to continue. The short pain trade in Australia has been so big in selected Australian stocks this year that I suspect many shorters may simply rule Australia off from this point as a place to short.

IPO’s: stag profits increasing

Globally and domestic IPO debut premiums are increasing. Another crucial feature of a bull equity market is day 1 IPO premiums. Stag profits are good for the equity asset class and remind those parked in cash what they are missing out on. The trend of successful IPO’s is very important. I expect to continue into year end.

AGM Season: benign

The Annual General Meeting season in Australia is underway and I expect it broadly to pass without incident in terms of guidance. In recent years the AGM season has been a profit-warning-a-thon, but this year it will be benign. I don’t expect or need Boards to talk up the outlook, I just need a non-negative AGM season. Pass the Tim Tams.

Broker Conference Season: benign

In recent years the broker conference season has also been a profit-warning-a-thon, but this year it will also be benign. Again, I don’t expect or need CEO’s to talk up the outlook, I just need a non-negative broker conference season. Pass the PowerPoint preso.

Sentiment: improving

Investor, analysts and commentator sentiment is going to swing further from what could go wrong to what is going right. As you know I think we are in for a period where “everything goes right” for Australia which would be a nice change from the last 5 years which were interrupted by regular sentiment speed bumps, exacerbated by woeful political leadership.

Forecasting sentiment is actually the key to everything and I believe we are moving from a consensus glass half empty approach to glass half full approach. The difference between the two is about 4 P/E points.

The great rotation: accelerating

Fund flows will continue to head towards equities (and residential property). Out of fixed interest/cash into risk assets will continue to accelerate, while at the same time compulsory superannuation contributions rise.

Domestically, the great rotation from cash is a trickle, but I am forecasting it to become a torrent as Australian’s parked in cash get textbook FOMO.

Banks are lowering TD rates, property and equity prices are clearly rising. Yet as we sit here total cash holdings of Australian investors, and Australian corporates for that matter, are at record highs. Amazingly,that record cash holding is at record low after-tax cash real yields.

The cash and fixed interest dam wall is cracking and we are all underestimating its power as it re-enters traditional risk assets.

Australian Bank reporting season: record profits and dividends

The Australian Banks will give investors clear evidence why their money should be in bank equities not bank deposits. The pending bank full year reporting and dividend season is going to be a cracker. That is obviously important for a wide variety of reasons.

Fully franked dividend growth alongside the risk of special dividends is going to be the key. These bank boards are fully aware what their shareholder army wants and they will feed them it again.

The Australia Bank reporting season has every chance of being the catalyst that drives the ASX200 into a new higher trading range.

All true or half true even if only in a short term cyclical sense and remarkably evidence free. Stocks could indeed run riot over the next few months. Only two problems, this:

And this:

I don’t want to get cocky. I underestimated the impact of the election on confidence and pent up demand can push a boomlet for a little while. But the structure has to change to get it past a few quarters. An economy can’t run on confidence alone.