Fitch Ratings says the federal government’s move to raise the debt ceiling was unlikely to result in any near-term loosening of policy and they did not expect Australia’s AAA-rating to be threatened.

The credit rating agency said overnight that while the debt ceiling hike to $500 billion was a “significant increase in comparison with recent adjustments”, “it does not constitute a loosening of fiscal policy or an imminent jump in the debt burden”.

“One reason why we do not believe the hike in the debt ceiling signals an imminent loosening of fiscal policy is because we expect the new Coalition government will remain on track to reaching a modest budget surplus by 2016-17. This would also be broadly in line with the roadmap set by the outgoing Labor government,” Fitch Ratings’ Art Woo and Aninda Mitra said.

“The absence of any deep ideological divide between political parties on core aspects of fiscal management is a key factor underpinning Australia’s strong sovereign credit profile.”

Over the next three years, all things equal, the odds favour that the Australian Budget is going to be under ongoing stress as mining investment plunges, the growth rebalancing to other sectors falls short, the dollar remains too high and the terms of trade keep falling as China enters its reform process.

Don’t get me wrong. I wouldn’t downgrade Australia yet, either. The public debt stock is still low enough that it can carry plenty of ineptitude going forward. But nor would I say I expect the surplus. I’d warn it’s needed and express my concerns therein.

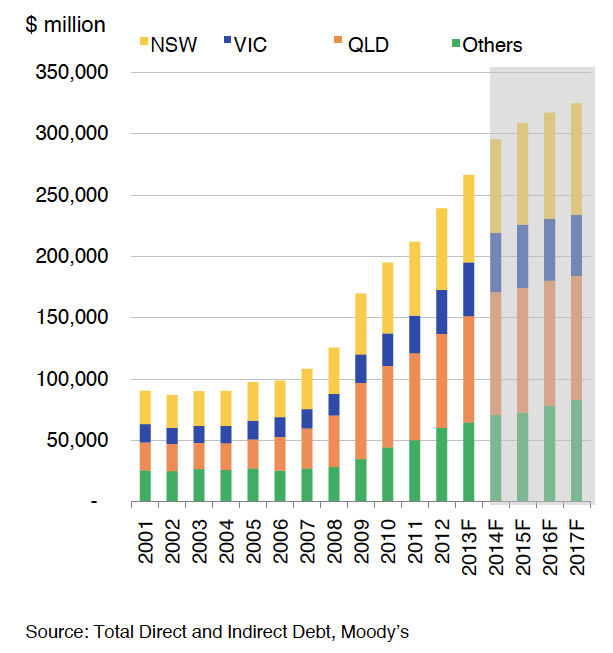

Interestingly that’s exactly what Moody’s has done with state debt today:

Advertisement

Moody’s Investors Service says that the sector outlook for the Australian states and territories remains negative, as it has been since 2010, given still wide deficits and increasing debt levels.

The sector outlook is separate to the individual rating outlooks for each Moody-rated jurisdiction. Specifics behind the negative sector outlook include the challenges each state and territory government is facing to slow expenditure growth in line with less robust growth in each jurisdiction’s own-source revenues and in

Commonwealth-backed GST transfers. Nevertheless, Moody’s notes that encouraging signs on expenditure control have recently emerged.

At the same time, Moody’s says that the Australian states and territories outperform their peers in Canada and Germany, showing, for example, lower debt burdens. In the case of the Australian entities, the latter are expected to peak in 2014.

On the other hand, Moody’s says that more recently the Australian states have exhibited a slower pace of recovery than their peers in Canada and Germany in terms of their cash deficits as percentages of their revenues.

With this year’s budgets, all states and territories postponed the timeline for achieving budget surpluses. Queensland, Victoria and South Australia now expect balanced budgets in the next few years, while Tasmania, New South Wales, the Northern Territory and Western Australia still project deficits.

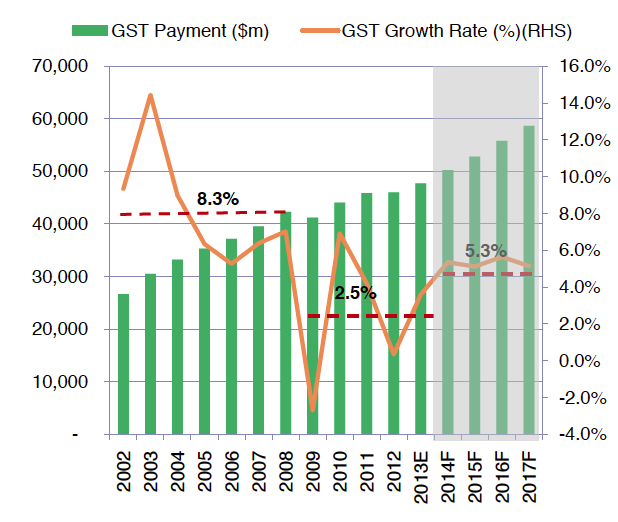

Over the medium term, Moody’s says challenges include risks to GST-based revenue, given that it is the largest source of state revenue, but is growing at a slower pace because of greater spending on GST-exempt items.

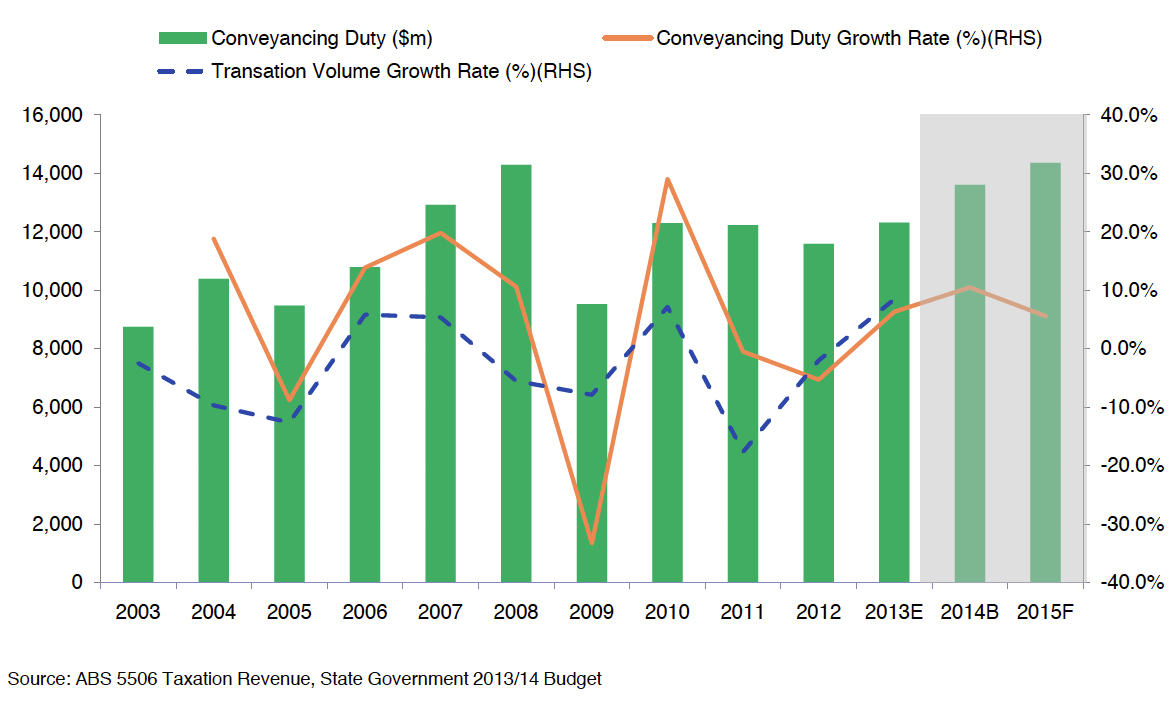

Moreover, the volatility in conveyancing revenues presents another challenge to the ability of each jurisdiction to balance its budget.

While some progress is apparent in expenditure control, as noted, another key risk is the strength of each jurisdiction’s resolve to maintain a lower level of expenditure over multiple years.

Finally Moody’s indicated that despite the risks noted each state and territory government’s inherent credit strengths are such that any rating adjustments would not be major.

The “risks” section is the killer. GST projections are boom time aggressive:

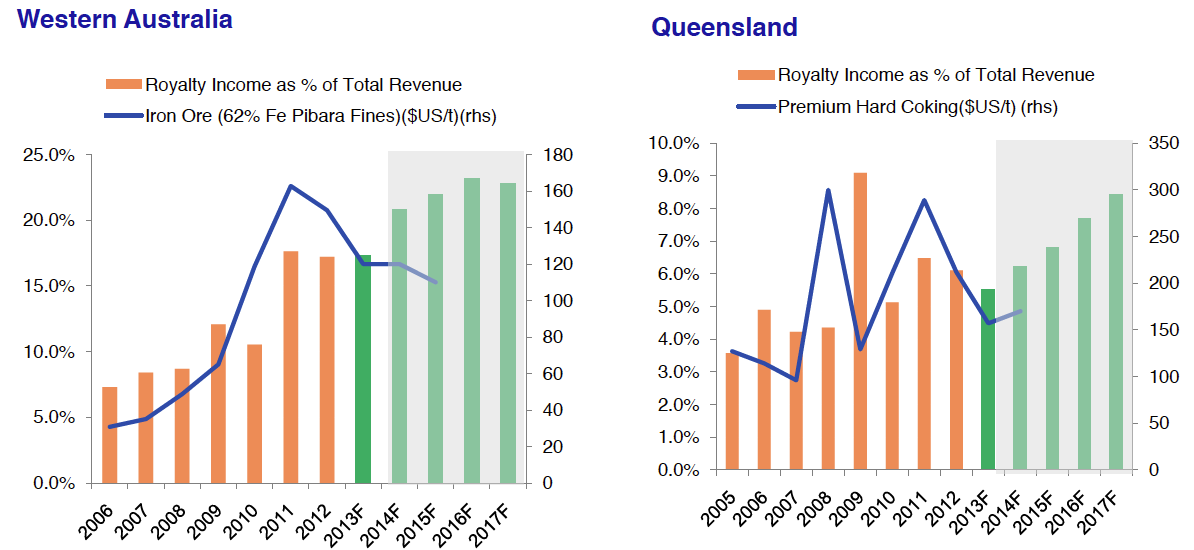

Royalties forecasts are only extremely aggressive:

And stamp duty is very aggressive:

That’s one hell of a boom ahead in all major components of state revenues!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Over the medium term, Moody’s says challenges include risks to GST-based revenue, given that it is the largest source of state revenue, but is growing at a slower pace because of greater spending on GST-exempt items.