There is plenty of buzz today around new housing following the last few day’s of data but plenty of errors as well. The Kouk continues his unwavering support for a renewed housing cycle:

As the level of mining investment falls away and leaves a potential pock mark on the pace of economic growth, housing construction needs to take up some of that slack, thereby ensuring bottom line GDP growth is sustained somewhere near the 3 per cent trend.

…Another critical element behind the need for there to be a solid and sustained lift in housing construction is related to demographics. Australia’s population is increasing by around 1 million people every 2.5 or three years through a mix of immigration and natural increase. This is around 400,000 per annum. This means Australia needs to build a lot more houses for these extra people to rent or buy.

Assuming the average size of each household is 2.5 people, this means there has to be a net increase in the housing stock of around 160,000 each year. When knock-downs and rebuilds are added to this, Australia needs to build close to 185,000 dwellings a year to meet ongoing demand. If there is not a construction increase to meet this extra demand, perhaps linked to state or local government zoning laws or infrastructure requirements, and new construction falls short of this, then good, old-fashioned supply shortages will underpin an unwelcome lift in house prices.

This is not altogether right. The fundamental assumption that the number of people per house won’t change is wrong if economic growth does not accelerate, which is likely as the mining boom comes undone. Even the kind of decent if sub-trend growth that is being forecast by BREE, at 2.5% for the next four years, will not be enough to prevent rising unemployment. That will mean less folks per household as people move in together so hard definitions of housing shortages need to be taken with a big grain of salt.

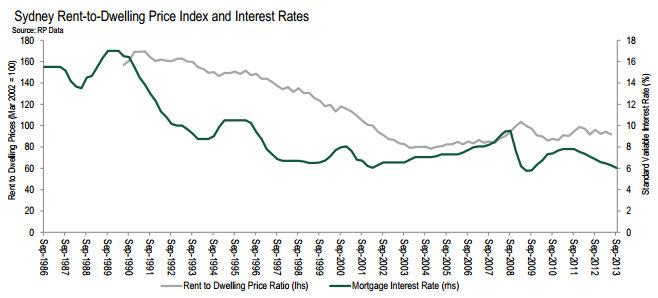

The one exception to this, or mitigation of it, is Sydney, where the imbalance is very large. Perth too but it has already responded with a new wave of construction and its demand is under increasing strain as the mining bust marches on. The other cities are all well or over-supplied already.

Advertisement

So, if that’s the case, and the price rises are now largely happening in Sydney, then surely there is no bubble? That’s what Stephen Kirchner of the Centre for Independent Studies thinks at the AFR:

…Dwelling prices have benefited from recent reductions in official interest rates by the Reserve Bank. Asset prices, including house prices, are one of the key mechanisms through which changes in monetary policy are transmitted to the rest of the economy. Far from being a problem, the responsiveness of dwelling prices to changes in official interest rates provides the central bank with useful leverage over the economy.

…Many commentators have singled out the role of investors as a factor driving house prices, including those who may be negatively gearing, foreign investors and, more recently, self-managed super funds.

Investors play a particularly important role in supplying the rental market. The dwelling stock, including rental housing, must ultimately be owned by someone. Reducing incentives for investment in housing will do more to harm housing supply than limit demand.

Kirchner concludes macroprudential is therefore a bad idea. One wonders why a think tank does not have time to do research. As we all know, investor’s dollars overwhelming go into existing property:

Advertisement

The exception is foreign investors and macroprudential would lower the dollar and bring in more of them. The HIA mounts a similar argument in a new note today:

The current relatively fast pace of appreciation in median house prices in Sydney reflects strong fundamentals and a catch-up from years of under-performance.

Current house prices appear in line with market fundamentals.

Rising house prices are providing a positive signal to residential developers and builders and Sydney is currently one of only two capital city markets where a strong recovery in new home building is underway.

It is crucial that new residential supply in Sydney continues to grow in 2014 and 2015. This outcome will require on-going focus on policy reform.

Advertisement

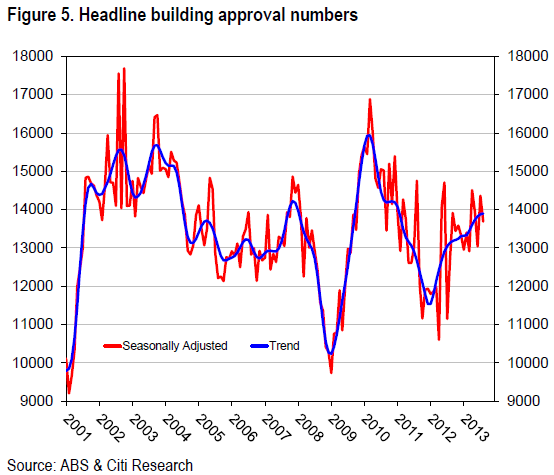

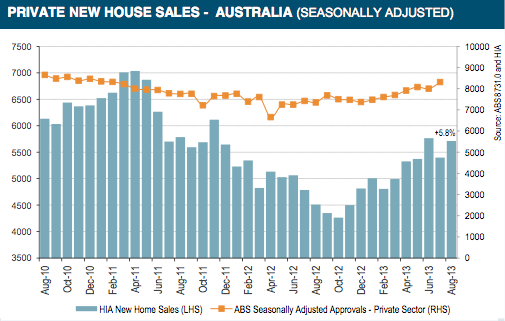

Despite the support for rising prices, it’s the last word that is the most important. Reform. Even with price rises, the supply response will be limited by structural factors including investor’s preference for established property owing to tax incentives and planning restrictions. It’s already obvious in plateauing new home sales and approvals:

Advertisement

It’s hard to believe the cycle will pull up already given the extent of population growth and fiscal incentives but it’s a very modest response.

Meanwhile, we risk bubble pricing growing away from the investment case even where it is strong, such as in Sydney, not to mention lousy economic fundamentals. It’s market perversion upon market perversion.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.