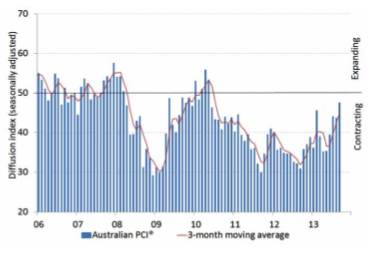

The Australian Industry Group’s three PMIs are all bouncing sharply. Last week we saw the manufacturing (up 5 points to 51.7) and services (up 8 points to 47) PMIs jump. Today it’s the Performance of Construction Index (PCI) which has bounced, up 3.9 points to 47.6. Two of the indexes obviously remain in recession but the second derivative improvement is unmistakable:

The national construction industry moved closer to stabilising in September, recording the slowest rate of decline in almost three and a half years. The seasonally adjusted Australian Industry Group/ Housing Industry Association Australian Performance of Construction Index (Australian PCI®) increased by 3.9 points in September to 47.6 points. Although this is still below the critical 50-point level that separates expansion from contraction, this was the highest reading for the Australian PCI® since May 2010.

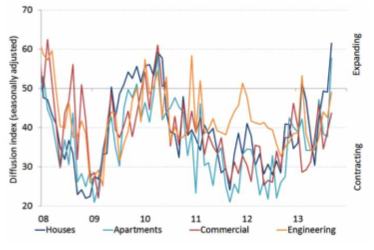

In September, growth in new orders drove an expansion in activity for the first time since April 2010. Despite the overall improvement in operating conditions, employment continued to contract in the month. September saw a return to growth in both the house and apartment building sectors. House building activity recorded its first expansion since February this year (and its highest reading since May 2010) while growth in the apartment sector followed 3½ years of decline. Continued falls in activity were recorded for commercial and engineering construction, although for both sectors the rates of decline moderated in September, relative to August.

Businesses reported increasing levels of incoming work and a pick-up in new tender opportunities. House builders reported an increase in enquiries and an improvement in home buyer sentiment. Nevertheless, a range of impediments continue to weigh on the industry, with widespread reporting of tight credit conditions, a lack of public sector building activity and weak investor sentiment in the commercial construction sector.

Activity is up especially in houses and apartments:

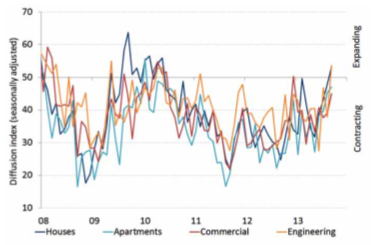

New orders are led by houses and engineering:

Advertisement

And the internals are all looking up:

Were this a regular cycle you would say it was game on. With the capex cliff looming, however, the headwinds ahead are awesome. At least there is some little momentum creeping back into the economy before it gets too steep.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.