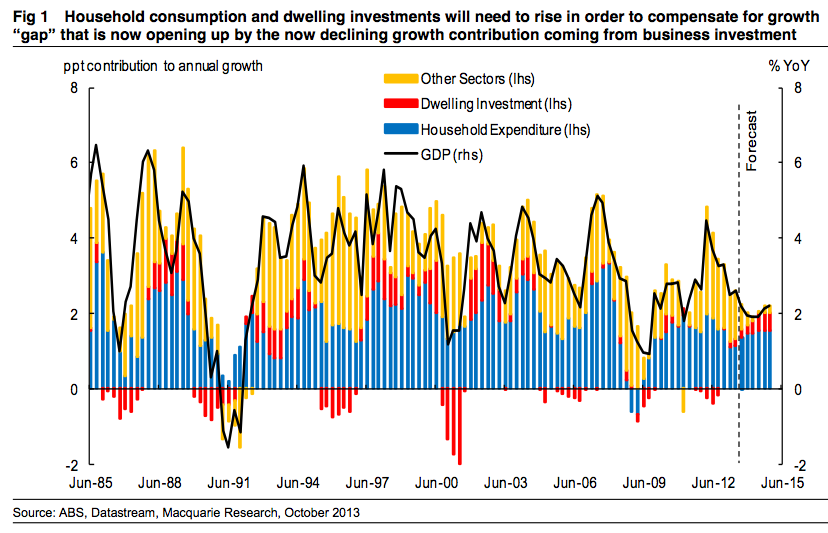

The growing bevy of consumptionista really are kidding themselves about Australia’s future growth prospects. Equities analysts, market and official economists relying on a consumer rebound to drive growth need a wake up call and yesterday Macquarie Bank produced a chart that does it for me:

Take a long hard look at this growth forecast and its components. Note, first, that Macquarie Equities’ forecast for growth is a smidge above 2% for the next two years. I’d make it three years.

That’s roughly a continuation of today’s economy so it would involve an ongoing rise in unemployment. Not too fast but rising nonetheless.

Now look at the composition of growth. Household expenditure represents three quarters of it. Add in dwelling investment, which is also based upon consumer demand, and it is 95% of expenditure in the economy.

Macquarie adds another bit for “other sectors” which will be a balance of the huge mining capex falls offset by government and non-mining expenditures.

Now look back over time and see if you can see any comparable period of growth composition. Nope.

One could mix and match these components. For instance, I reckon “other sectors” will quite possibly detract from growth and that from time to time consumption will be higher. But that is neither here nor there. The basic outlines here are correct. Australian growth will now hang entirely upon the consumer and this is where I am quite concerned. I do not believe that the consumer is strong.

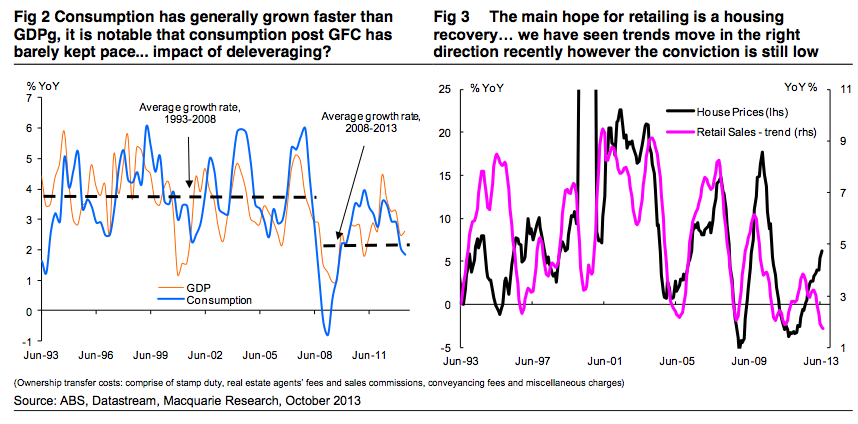

I could grab any number of charts to illustrate my point that the consumer has made a structural shift to higher savings rates. But Macquarie provides a couple of charts that make the point well enough:

The trends towards lower consumption growth are very clear. Those trumpeting a consumer-led rebalancing are implicitly relying upon a post-GFC trend break in household behaviour that I don’t think it is coming.

The cyclically focused will point to recent improvements in house prices and confidence as evidence that I’m wrong. And if the world motors along without disruption for the next three years they may be right.

But if the US fiscal debacle tells us nothing else it is that that is not the world we are now living in. The slow unwind of the thirty year build up of global imbalances will go on. Europe will face repeated fiscal reform questions. The US will face repeated fiscal retrenchment questions. Asia will face repeated debt and internal demand questions. And global interest rates will slowly rise.

Australian households know this in their bones. That is why their savings habits have not budged in the five years since the GFC. They will not break out and party now, rather, any flush of spending will prove fleeting and if the weather turns sour they will scurry for cover like so many meerkats.

And because our economy will hang on their every move, with no underpinning of sustained business investment growth to keep it ticking over, it too will be volatile. In this environment interest rates are very unlikely to rise so we will also see breakouts of exuberance, such as in Sydney right now, exacerbating the volatility.

This has several implications for investors. It means that all asset prices are vulnerable to quick reversals of fortune, hedging is vital and going long on particular local asset classes is more reckless now than at any time that I can remember. If rates do rise, duck.

It need not have been this way. Authorities could have innovated policy to lower the dollar and driven growth via a tradables investment rebound. The volatility I foresee will make a far deeper correction for the currency inevitable anyway, alas too late.

We all hang now on the delicate wave of the confidence fairy’s wand.