More calls today to buy cyclical stocks, this from Morgan Stanley:

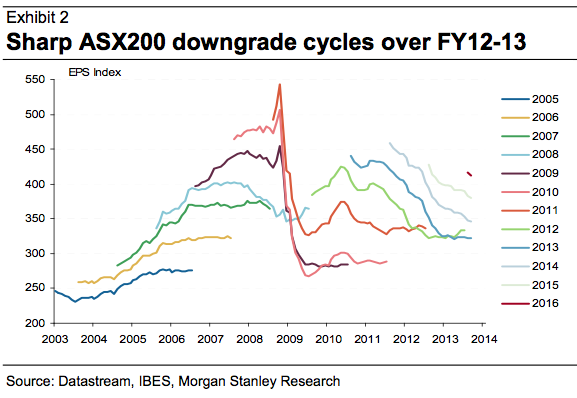

On a rolling 12 month basis the ASX 200 is up circa 20% TSR with the positive bias to index returns continuing in FY14 YTD up 9%. The Index rally has been against the backdrop of a meaningful downgrade cycle for equities, where aggregate EPS growth has not been seen since 1H11. Multiple expansion (like most other markets) has been the driver of returns – so much so, we now are presented with another year of decelerating EPSg (+8% in FY14e from +14% growth forecast in July) with the forward PE at 14.3x, after re-rating from 11.2x two years ago.

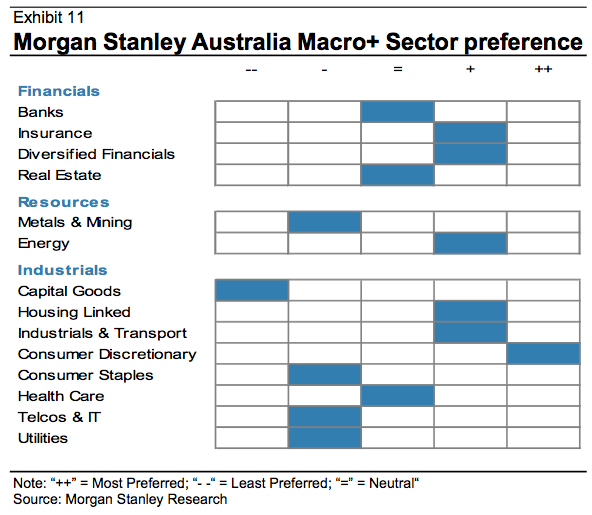

…in need of Earnings Upgrades: The most enduring themes of the last two years have been Financials and Industrials over Resources, yield compression and foreign earnings over domestic. In recent months there have been tactical tilts to even out the aggressive consensus resources underweight positioning. We also detect an increasing focus by investors on when earnings growth, and ultimately an upgrade cycle returns.

Proof Will be in The Domestic Cyclical Stocks

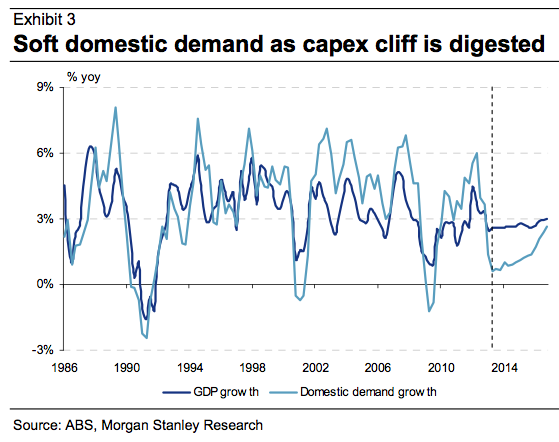

Our focus is on domestic cyclical stocks. We believe they will be leveraged to, and provide confirmation of whether Australia has successfully transitioned from the construction phase of the commodity boom, towards an east coast rebound that is being keenly targeted in monetary policy settings. Australia needs the activity multipliers from a genuine housing rebound and a pick up in the consumer, combined with a better-funded public infrastructure program to generate this rebalancing.

Hall Pass for FY14e and Backing a Successful Transition in FY15e

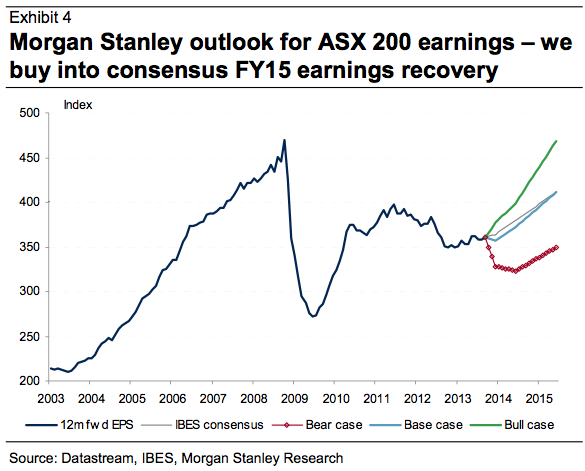

The FY14e market multiple of 14.3x suggests stocks are fairly valued based on likely growth to be delivered this fiscal year. And while a likely subdued upcoming AGM season may test short term sentiment around valuations and cap near term upside, we believe investors should give FY14e a Hall Pass and focus on the green shoots slowly emerging that support the case for FY15e being a year of potential upgrades.

ASX 200 Target Set at 5,500 (+7% Upside)

We set our rolling 12 month target for the ASX 200 at 5,500, which implies 12% total returns from current levels. For USD-benchmarked investors, matching this target to our global FX team’s 12 month forward AUD forecast of 0.84 implies flat USD-total returns for the ASX 200.

MS goes on to argue that cost-out and labour price deflation, interest expense reductions, margin and volumes growth and AUD depreciation will all contribute to the rebound in earnings. These are the typical dimensions of cyclical earning recovery. The question is is this a typical cycle?

I don’t think so. For a start, the capex cliff will not end in 2015. On the contrary, it may well steepen as LNG projects move into production. That’s what Saul Eslake sees. 2016 looks similar to me.

Advertisement

As well, house prices can rise for a while only. The best case is probably one year. At some point interest rates or unconventional policy will have to move, or build greater risk into the financial system via an increasing weight towards investors, higher LVRs, increased offshore borrowing or all three.

The China and iron ore factor remains as well. It is probable that China will begin to slow again mid next year as the current stimulus works its way through the economy. Rebalancing has not yet even begun but it likely will even as iron ore supply grows. The odds of a decent external shock next year are pretty good.

Once the taper talk resumes again, also mid next year at a rough guess, the dollar should resume its falls so that’s a positive.

Advertisement

In summary, my view of the cycle is that 2015 will look much like 2014 and, as such, that there will be little change in prudent consumer behaviour even if house price rises continue next year.

However, what I think matters little. What does matter is what everyone else thinks that everyone else thinks. As I said the other day when assessing Charlie Aitken’s hysterical bullishness:

Whether it’s wise to be “short Australia” at this point is a moot point. But the bull case is far less clear than Aitken’s argues. Having said that, I reckon we’re going to see six months of sunshine which will be enough to send the Aitken’s of this world nuts for cyclicals.

Advertisement

Do not underestimate the potential for a stretch in valuations surrounding cyclicals.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.