At last some sense on the Australia gas panic from Morgan Stanley. For some time I’ve been arguing solo that the premisses of the eastern states gas debate are fallacious. Particularly because the desperate push to mine more gas will do nothing to lower prices owing to its more expensive production costs (no matter where it ends up).

MS examines just how expensive:

Shale gas is high cost for the following reasons:

1. Many wells are required for commercial production. Low production rates and recoveries of small volumes per well characterize shale gas fields. Many wells per field are required to achieve sufficient production. A typical shale gas well may initially produce at rates in the order of 2-10 MMscf/d, decline at 80% p.a. and recover a total volume of 2-8 Bcf over 20 years, depending on the geology.

2. Shale gas wells are more expensive. In most cases, shale gas wells require a horizontal section to be economically viable. Horizontal sections require a bigger (more costly) drilling rig. These wells often use more consumables such as casing, cement, drilling fluid, etc. because they are longer and take more time to drill. Hydraulic fracturing (fracing) adds to the well cost due to the equipment and chemicals required. We estimate that a 3,800m deep vertical well in the Cooper Basin, drilled over 60 days costs circa US$10m (excluding fracing). Approximately 80% of the cost is variable and related to day-rates or depth (Exhibit 8). Rig mobilisation costs, access roads, fracing and well testing adds to the cost. We estimate vertical well costs including fracing and testing are likely to be in the order of US$15m with horizontal wells more expensive again, in the order of US$20m.

3. Infield infrastructure costs. Large numbers of wells dictate a higher investment into field gas-gathering facilities, processing and compression. There are economies of scale if gas processing is centralized, however, a particular challenge is optimising field gathering systems to handle the ‘peaky” production profile from shale wells. Optimum investment into gathering and processing requires stable long-term production, so that operational capacity can be fully utilized for the maximum time. Individual shale wells are not well suited to deliver base load production.

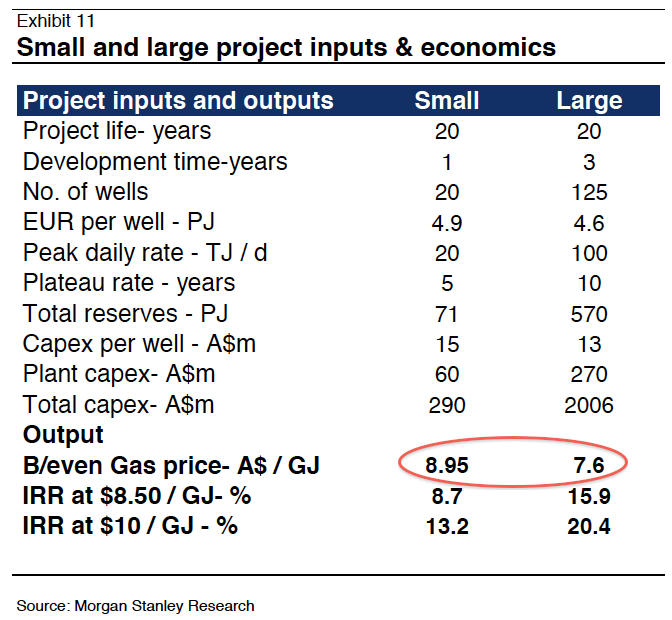

MS models a small and large scale project and these yield the following numbers:

Check out the break even prices which equate to roughly $8 and $7mmbtu. These are the asme as the netback prices for current gas export projects meaning:

We expect competition from US exports, and other new entrants will effect to attenuate global LNG price structures. We expect oil-linkage to remain but the linkage to ease. We assume current Asian LNG prices in the US$15-$16/mmbtu range ease back to the US$12-$13/mmbtu range after 2017. These are delivered prices into Asia. For domestic LNG netback pricing parity, we back out shipping and processing costs, which results in net-back prices into the plant approximating US$8-$9/mmbtu. This translates to A$9.1/GJ – A$10.2/GJ at current conversion rates. We think domestic prices longer term will be capped at these levels. Any higher, and marginal gas molecules destined for export would be diverted to the domestic market.

Precisely. Mining more gas won’t do squat. No doubt protection will be the policy of choice.