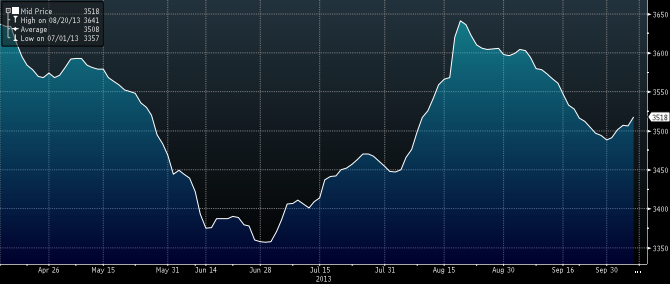

Don’t look now but rebar is recovering. That’s driving a rebound in ore paper markets and spot. Yesterday the 12 month swap put on another $1 to end at $113.87 and threatening to breakout. Spot was up .50 cents to $133.60 and rebar average continued its post Golden Week bounce, up 12 yuan to 3518:

Same deal for futures. Chinese port stocks were up lat week to 77.4 million tonnes.

In news, the SMH has neat roundup of the supply increases coming through in the Pilbara:

Australia’s “big three” iron ore miners are set to unveil a boost in third-quarter production and will mine even more in the fourth quarter, ignoring forecasts of a looming supply glut in favour of capturing greater economies of scale.

Rio Tinto this month upped annualised output of the steel-making raw material by 20 per cent to 290 million tonnes, while BHP Billiton and Fortescue Mining are in the midst of robust expansion work.

All three already mine ore at costs well below selling prices — thanks to a combination of rich grades and high volumes — and see any dip in prices as simply weeding out less competitive rivals.

Rio Tinto, which is set to post a 3 per cent rise in third-quarter output against the previous quarter to 53 million tonnes on Tuesday, is expected to announce a further mine expansion to 360 million tonnes a year by a December 3 meeting with investors.

“With the iron ore price holding up well as we move into Q4, we expect to see continuing growth from this key driver of earnings,” said RBC Capital Markets analyst Chris Drew, pointing to resilient demand from China.

Fortescue is set to unveil on Thursday a 20 per cent output increase to just under 30 million tonnes for the three months to end-September, and BHP Billiton a 4 per cent rise on October 24 to just under 50 million tonnes.

Makin’ bacon hand over fist right now but seasonal weakness is still likely unless the communists now control the weather as well.