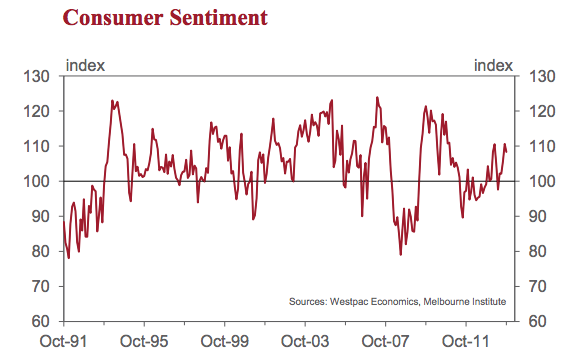

Westac Consumer Sentiment for October is out and fell by 2.1% from 110.6 in September to 108.3 in October.

This is a solid result. It follows the 4.6% jump in the Index in September – a result largely influenced by the expected election result. The Index is still 2.5% above the level in August and 9.2% above its level a year ago.

Apart from last month it is the highest read for the Index since March this year.

The modest fall in the Index is probably due to an expected retreat following the positive expectations around the election result. Other factors that might have weighed on the Index were the steady fall in the sharemarket through the survey week (down 2%) and the steady rise in the Australian dollar (up from USD 0.93¢ to 0.94¢) through the survey week.

The shutdown of the US government and media speculation around a US government default would also have unnerved

respondents.

Two index components rose in the month and three fell. The components tracking consumers’ assessments of the economic outlook over the next 12 months and next 5 years declined by 2.0% and 7.3% respectively. This adjustment probably reflects a little ‘cooling off’ following the anticipation around the election result.

Recall that these components rose by 8.7% and 7.1% respectively in September.

The disappointment last month was the failure of respondents to ‘mark up’ their confidence around their own finances. The subindex tracking consumers’ expectations for their finances over the next 12 months rose by only 1.6% in September whereas the subindex tracking assessments of finances relative to a year ago actually fell by 1.9%. In the October survey the 12 month outlook index dropped by a significant 5.5% while the comparison with a year ago improved by 0.7%. In fact both measures are now below their pre-election levels.

This lack of response around people’s assessments of their own finances raises some doubts as to whether the healthy reads of the overall index will spur consumers out of their current spending torpor.

There has been undoubted improvement in the sub-index tracking views on ‘whether now is a good time to buy a major household item’, improving by 6.9% in September and a further 3.2% in October. However, in this cycle, this index component has been consistently strong without any pick-up in consumer spending.

There was a shock around assessments of ‘whether now is a good time to buy a dwelling’. That index fell by 10.3% from 140.0 to 135.0. There were some big falls in individual states

– NSW down 22.5% and Queensland down 11%. There was a similarly sharp decline in this Index back in April following media speculation that the next move in interest rates might be up.

This month’s decline comes after reports of strong gains in house prices, particularly in Sydney, suggesting that deteriorating affordability and warnings by some commentators of the potential for a price bubble may be driving the shift in sentiment.

Respondents remain concerned about jobs. The Westpac Melbourne Institute Index of Unemployment Expectations rose in October by 0.6% in October, indicating more consumers expect unemployment to rise over the year ahead. The Index is 10.1% above the level in November 2011 (the date of the first rate cut in this cycle), indicating significantly more heightened concerns around job prospects than at that time.

That contrasts with the overall Consumer Sentiment Index which is 4.7% above its level in November 2011.

The Reserve Bank board next meets on November 5. While we expect that there will be further rate cuts in this cycle a cut is unlikely to come as soon as November. The Board is likely to await further information on the sustainability of the boost to consumer and business confidence, which occurred around election time and whether that boost is being reflected in hiring; investing; and spending decisions. Developments in the housing market, particularly around the recent uplift in Sydney property prices, will also be considered by the Bank. We expect that rate cuts will resume early next year. In those respects today’s survey shows a high outright level of overall consumer confidence although respondents remain cautious about their own finances.

There is also some early evidence that the gloss may be coming off the housing market as rising prices start to impact on affordability and confidence.

So, the election bounce is passing. Regarding property, and with respect to Bill Evans, there has been very little discussion about rising interest rates to suppress sentiment recently. I’d guess that confidence has tanked, especially in NSW, because of a combination of collapsing affordability and the righteous “bubble” narrative in the press.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.