From UBS today comes a useful preview of next week’s CPI:

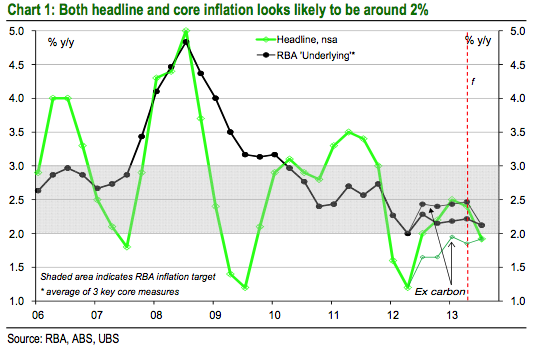

This week we highlight UBS’s Q3 CPI survey, ahead of official data on 23 October. With Q3 being a seasonally high quarter, and petrol prices up almost 7% (largely due to a lower AUD), our survey shows headline CPI rising 0.9% q/q, its fastest in a year (& its fastest in two years, ex carbon). Nonetheless, the y/y pace eases to 1.9% from 2.5%, its slowest since mid 2012, pre the introduction of the carbon tax.

For the more important underlying CPI (which adjusts for seasonality & volatility), we find the RBA’s statistical core average increased 0.5% q/q (similar across the trimmed mean & weighted median) – the sameas the past few quarters. With the carbon tax-inflated 0.8% gain from Q312 ‘dropping out’, the core average eases to 2.1% y/y in Q313 from 2.4% in Q2 (albeit only marginally below our ex-carbon estimate for Q213). Including CPI (ex vol), ‘underlying’ inflation in Q3 (0.6% & 2.1% y/y) is likely to be ‘in line’ with the RBA’s forecast of 2¼% y/y by end 2013.

Of note, the current worryingly high (4.3% y/y) pace of non-tradable inflation should drop to 3.5% in Q313, as Q312’s carbon tax introduction ‘drops-out’, easing concerns over domestic inflation pressures. This is only partly offset by a renewed rise in tradable (or imported) inflation (now -0.7% y/y), which should edge up to -0.4% y/y (ahead of further rises over the coming year as the lagged impact of a lower AUD is passed through). On balance, the macro backdrop suggests slight downside risk to the official inflation print – with weak domestic demand in 1H13, business surveys showing weak price trends, slower wages growth, & lower global inflation. However, the recently improving trends in business & consumer confidence, domestic housing, and the global data (US politics aside) still likely sees the RBA on hold for now, absent core CPI with a 1-handle y/y (0.3% q/q).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.