Paul Bloxham has produced a new document aiming to debunk fears of an Australian housing bubble. Find it below. There’s nothing new here but the conclusion is extraordinary:

The RBA would not be too worried about the current rate of housing price growth. In fact, the rise in housing prices would be largely as expected and somewhat desirable, given the need to rebalance growth.

Recent comments made by RBA Assistant Governor Malcolm Edey support this. He warned, at a recent conference, about being unrealistically alarmist about a housing bubble and, for effect, stated the obvious: that “we shouldn’t be rushing to reach for the bubble terminology every time the rate of house price increase is higher than average, because by definition, that’s 50% of the time”. Indeed.

I would take this with a grain of salt. Junior governors at the bank have been selling the “no bubble” message furiously and without cease for many years. More senior governors have been more circumspect. Glenn Steven’s himself warned household against higher leverage recently and the recent FSR also warned against price rising ahead of income. Back to Bloxo:

Advertisement

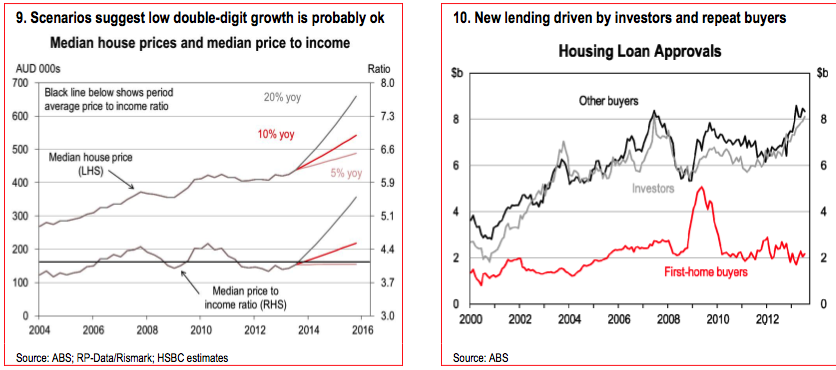

Some simple scenario analysis helps to reveal why the RBA is unlikely to be worried about the current pace of growth, in itself. Given the fall in housing prices between late 2010 and mid-2012, there is some catch-up required just to maintain a steady price-to-income ratio (Chart 9). To get back to the previous peak in the dwelling price-to-income ratio by the end of 2015, as one might expect to occur in a housing price upswing, would require growth of +10% this year and in each of 2014 and 2015, assuming average growth in household disposable incomes.

But the price level itself is unlikely to be the main concern anyway. The RBA’s concern will likely be more with the amount of leverage involved in driving housing prices higher. The broad lesson from the global financial crisis (and earlier episodes) was that it is not asset price misalignments that matter in themselves, but the leverage associated with any misalignments that can do the most damage.

Simplistic scenario analysis more like. Would the RBA like to see leverage on household balance sheets climb to records? No. Would it let it? I don’t think so. Bloxo is right that prices don’t matter, imbalances do. But his analysis is overly simplistic in the capex cliff world in which either households will act on the housing boom and spend more, driving growth but creating a bigger current account deficit in the process, or they won’t and unemployment will keep climbing and choke off house prices. You can’t have it both ways. Back to Bloxo:

New lending has been a key driver of the recent pick-up in housing prices. Housing loan approvals have risen by 18% over the past year. The bulk of the rise in new lending has so far been driven by investors and repeat buyers, rather than first home buyers (Chart 10).

The lack of first home buyer interest may be somewhat surprising, given the improvement in affordability. To some degree it may reflect the elevated unemployment rate, particularly for younger cohorts. The weaker labour market may have held back household formation, as lower job security has held back confidence and higher unemployment has made it more difficult to save a deposit. In short, current job prospects mean more twenty something’s living with their parents or in shared accommodation.

While a high unemployment rate may have held back first-time buyers from entering the market, it hasn’t led to a significant deterioration in banks’ loan quality. In fact, despite a high unemployment rate, loan arrears have drifted lower since 2011 (Chart 11). This is likely to reflect a number of factors, including that: the bulk of Australia’s household debt is held by high income households; lower interest rates have reduced the repayment burden sufficiently to offset the impact of lost income due to rising unemployment; and, Australia has full recourse loans, which should encourage mortgage holders to maintain repayments.

The new lending that has occurred in recent quarters has also generally been at lower loan-to-valuation ratios than in the past, which should also limit concerns about risks amongst banks’ housing lending. New housing lending in the 80-90% LVR category has held steady over the past few years, while new lending in the 90%+ category has drifted lower since the recent peak in 2009 (Chart 12). Australian households have also maintained a fairly high saving rate in recent year and many households with mortgages are well ahead on their mortgage repayments. Recent estimates from the RBA suggest that liquid balances in mortgage offset and redraw facilities – ‘mortgage buffers’ – are 14% of outstanding mortgage balances, which is equivalent to 21 months of scheduled repayments at current interest rates.

At this stage it seems that the financial system is broadly working as it should. Low rates have encouraged a lift in demand for housing, which in turn has driven a pick-up in housing prices. Higher house prices are beginning to attract more developers to the market and approvals for new housing construction have begun to rise.

Bottom line

Australia’s housing boom is beginning. We expect high single-digit housing price growth this year and low double-digit growth over 2014.

This is trickling through to housing construction and we expect a further lift in coming quarters.

We remain firmly of the view that Australia does not have a housing bubble.

But we see concerns about inflating a housing bubble as enough to make the RBA reluctant to deliver more rate cuts.

Advertisement

Too simplistic. This cycle has not been at all typical. House prices have been very slow to respond to rate cuts, which is why the RBA has had to keep chopping. Another reason why rates are so low is the dollar remains far too high for the economy. Income growth is very slow as well. The absence of FHBs is another keen signal that this is an investor driven, financially repressed, rally and as such is vulnerable to a sudden reversal. Placing this cycle unquestioningly within the old housing cycle framework does nobody any favours.

Even for those playing the cycle, such as it is, I would warn them to discount this possibility. One thing I can say is that if national or even Sydney house prices are rising at double-digit rates mid next year, the panic within regulatory ranks will be palpable and intervention will be on the cards in one form or another.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.