Markets continue to grapple with the coughs and splutters of two very large liquidity pumps on either side of the Pacific. In the US it’s the resurgence of QE prospects which is driving the share market rally. In China it’s bubbly asset markets and hot money inflows forcing the PBOC to drain reserves via ceased repo operations.

Observe, last night’s US data showed distinct shutdown impact. Bloomberg’s Consumer Comfort index plunged, wiping out all of the 2013 gains:

The Bloomberg Consumer Comfort Index declined to minus 36.1 in the period ended Oct. 20, the lowest since February, from minus 34.1. The report also showed more households were pessimistic about the economy than at any time in the past year even as lawmakers approved a deal that ended the partial shutdown of federal agencies.

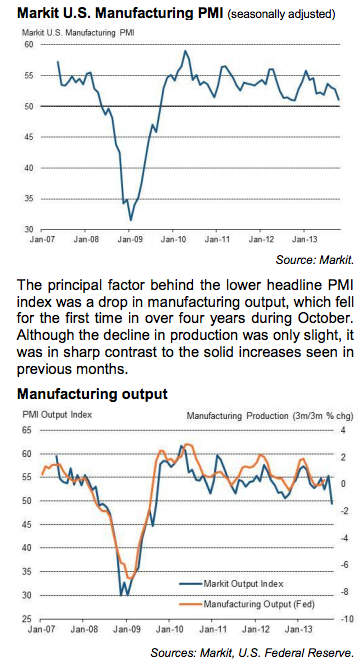

The US Flash PMI also fell sharply, especially production:

Advertisement

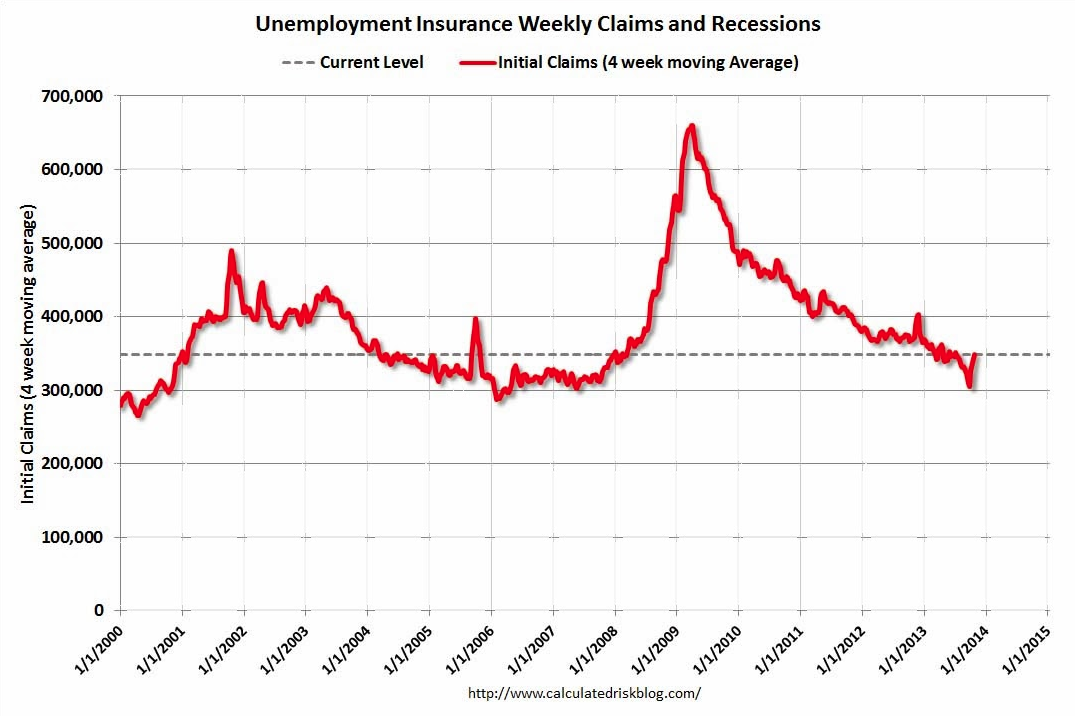

Weekly unemployment claims fell but not as far as markets hoped and remain elevated recently:

Advertisement

None of these are first tier data and they should rebound relatively quickly as public cash flows once more, although the lingering budget negotiations won’t help. Notwithstanding, this it’s hardly data to inspire a share market rally, which is what we got, unless it means that QE will be delayed. That has been clear in long Treasuries for a few days with yields breaking resistance lower (though rising last night 1% or so):

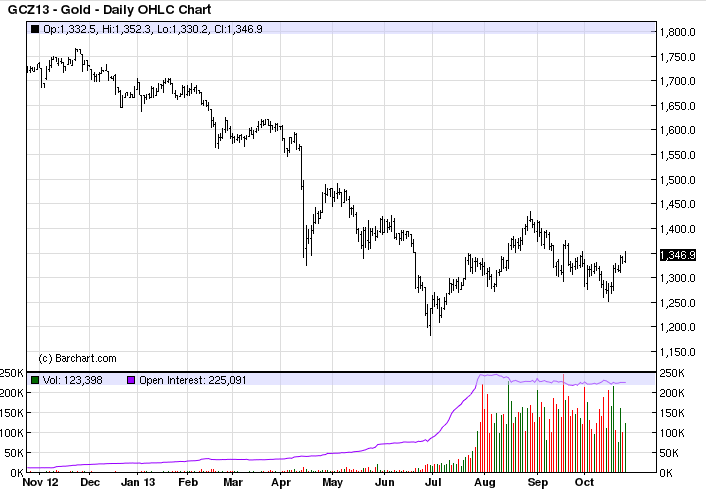

More QE was also very clear in the gold price last night, which rose another $15 and is enjoying a rebound from recent lows:

Advertisement

However, the Australian dollar did not follow. Indeed it fell half a cent and is struggling to hold 96 cents. The reason why is that the liquidity pump on the other side of the Pacific, in China, has run dry. From the FT:

The seven-day bond repurchase rate, a key gauge of short-term liquidity in China, opened at 5 per cent, a four-month high and up 150 basis points from the end of last week.

Advertisement

We already know that analysts are seeing this as controlled tightening by the PBOC, in part to damp hot money inflows. This turn of events is weighing on the Australian dollar, which has been on a tear, but there is little indication of further stress. In June, when SHIBOR last spiked, Australian bank CDS prices launched:

No such movement this time so far.

Advertisement

FTAlphaville has some more speculative and unsettling analysis about events in China:

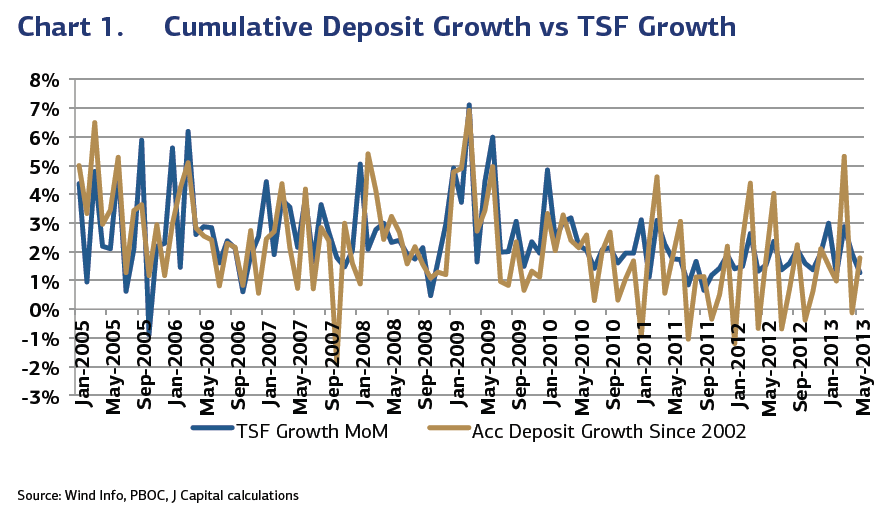

Let’s assume that then and take the extra time and infinite space we have here to mention the slowing rate of China deposit growth. Consider the following chart from Anne Stevenson-Yang at J-Cap:

That shows that on a cumulative basis since 2002, when the statistic started being kept, deposit growth has slowed from around 5 per cent in 2009 to less than 2 per cent now. That 2 per cent appears to come from new loans rather than from corporate earnings or individual disposable incomes says Stevenson-Yang who adds:

On travels throughout China last week, bankers all talked about the pressure to find deposits. They discount the national statistic showing mid-teens annual growth in new deposits, saying that “core” deposit growth, from savings, has been flat to negative for two years. An increasing portion of bank deposits are synthetic, created from the banks’ own commercial notes, short-term borrowings, and even a bit of fraud.

What this means is that banks have less cushion than it might appear against defaults, whether in the wealth management market or by borrowers. It also means that, while Chinese investment continues to soar in order to push forward a sputtering economic engine, savings are actually stagnant. Recall in the earlier decades of reform, it was China’s high household savings rate that enabled high levels of asset investment. Today, the savings are subsiding, but the investment is accelerating. That is not good news for the economy…

Banks have “little” audits at the end of each month and “big audits” at quarter end, and to meet the audit requirements, they often borrow, whether from local corporations or other financial institutions. Some of them complain that their end-of-quarter borrow rates have squeezed higher, as companies know that banks are going around hat in hand. Companies that are cash-rich have therefore learned to bid out their deposits by calling around to the banks to see who will pay the highest rate…

Almost three-quarters of deposits now are made up of “quasi-money,” which includes commercial bills, wealth management products, and other liquid instruments rather than cash and cash deposits. This rising proportion of quasi-money in deposits is not necessarily alarming in itself, but in China, the quasi-money has been put to work in highly illiquid investments such as subway projects, new cities, and real estate, which cannot pay out in the short term required to make these bank currencies liquid. Instead, banks have to keep issuing more to cover the old.

Over the last 18 months, the pace of quasi-money creation has outpaced total deposits, which could mean that, increasingly, economic entities are trading virtual instead of real currencies. Between Q4 2011 and Q1 2013, over RMB 5 trillion was created that did not end up as bank deposits. Some of the disappearing money might represent capital flight.

Might be of interest, particularly if hot money is filling the gaps Yang suggests are there to be filled. Or if, heaven forbid, the PBOC is less in control than we’d like… say if they haven’t quite grasped the scale of shadow money in the system and how it keeps the gears turning.

But for now it appears that China and the US have simply traded liquidity positions again. The US is back on an expected loose or even loosening monetary path and China on a tightening one. Shares and currencies are responding accordingly. Thankfully the Australian dollar has been caught between the two giant eddies and has stalled.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.