Charlie Aitken eat your heart out this morning as Mac Bank produces a much more sober take on the economy we’re in and the prospects for cyclical stocks:

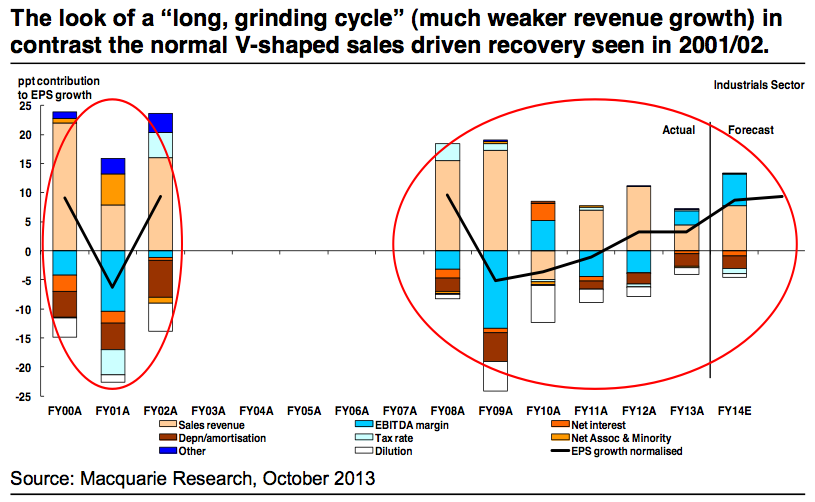

The recent profit reporting season reinforced the point that the Australian market is now beyond this cycle‟s earnings trough. Investors have now turned to the prospect of a cyclical EPSg upswing. In this research note we compare the magnitude of the earnings recovery seen to date & as forecast, with past upswings. Most critically we analyse the “anatomy” of these prior cycle upswings with the current and the implication that a “long grinding cycle up” might have on both EPSg and valuations, most particularly for cyclicals.

Impact

This cycle‟s profit recovery will in our view remain fundamentally different from the cycle recoveries of the last 20 years. A weaker recovery in sales will limit the quantum of the earnings upswing. In turn, this will keep pressure on costs, with further EBITDA margin expansion a critical and differentiating support for EPSg. If our analysis proves correct then this has critical implications for share price performance, particularly for cyclicals that are competitively weak.

Outlook

In a more muted recovery characterised by modest revenue growth, the prospect of cyclicals benefitting equally from any upswing, in our view, is unlikely. Given the share prices of many domestically focussed cyclicals are already pricing the early stages of an earnings recovery, it is critical to identify those offering the highest quality and most reliable growth into FY14 & FY15.

Our detailed EPSg decomposition analysis presented in this note suggests the market may already be pricing too much of an earnings recovery for some cyclicals… and yet the “best” cyclical earnings don‟t appear to have the highest valuations. Stocks notable here include JBH, SEK, PPT, FBU, MGR & to a lesser degree TOL, while expensive &/or lower “quality” cyclicals of note are HVN, QAN, BLD, BTT, DJS, & PMV.

Spot on. Macquarie goes on:

16 October 2013 2

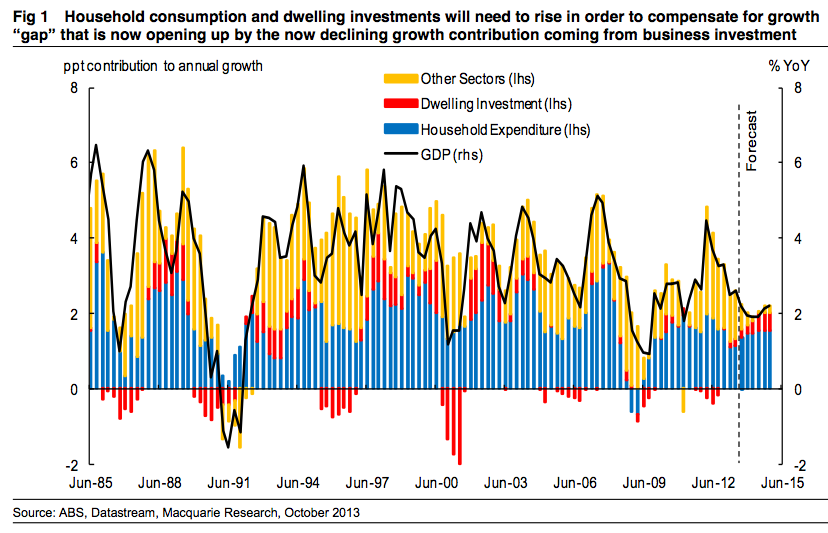

“Same same but different”: The changing drivers of Australian GDPg…

In the current cycle we have consistently noted in our research for some time that the behaviour of households appear to have changed. Notably the lack of any major response of households to the current long and deep cycle of interest rate cuts. And yet over the long run household consumption has driven more than half of Australian GDPg. Since 1960, household expenditure has contributed on average nearly 60% of Australian GDPg, while housing construction has also played a role in supporting the upswing in growth.

It is critical therefore that we assess the outlook for Australian GDPg, particularly the role that consumption and housing construction will play in this next economic upswing. It is also critical to compare and contrast the expected contribution that both consumption and housing may make in any economic cycle upswing given the “LGC” (long, grinding, cycle) environment, with the GPDg upswings of the past. Isolating the contributions of these sectors to Australian‟s GDPg over the last nearly 30 years is set out in Figure 1 below. We particularly examine the role these sectors played as “drivers” of GDPg recovery over two distinct periods of upswing (2001 – 2002 & 2009 – 2010) vs the recent period of strong GDPg. Our analysis highlights that:

Housing construction has been notably absent as a positive contributor to Australian GPDg since 2007 compared to its role in previous economic growth upswings. During the economic recovery in 2001-2002 and indeed post the last period of recession in Australia (1992 – 1994), housing (dwelling investment) contributed nearly 15% to rising GPDg, thus playing a key role in supporting these two periods of economic upswing. Since 2007 however housing has made little to no contribution to Australia‟s economic growth, with just the last two quarters showing the first signs of any positive GDPg contribution from dwelling investment.

Consumption is ultimately key driver of economic upswing in Australia. Particularly as we expect below trend GDPg in the coming years, the role of consumption and housing construction will be exacerbated. The analysis presented in Fig1 highlights that consumption has been the earliest sector to turn and to contribute the most significantly to the recovery of GDPg in Australia over the last 30 years. As seen clearly in Fig 1 on average +1.6ppts of the GDPg recoveries seen in 1991–94, 2001–02 (+1.9ppts), and 2009 – 10 was directly attributable to consumption. We expect this to be more moderate in this cycle.

“Other sectors” (aka business investment) have been key to the recent upswing in GDPg. Indeed business investment‟s contribution to Australia‟s GDPg in the last three years has been both large and dominant, accounting for more than half of Australia‟s overall GDPg, a direct impact of the strong and unprecedented current mining investment boom. As mining investment swings from the recent period of large and positive contribution to GDPg, to a sustained period of modest to negative contribution going forward, however, it begs THE question confronting policy makers: which part of the economy can and will pick up the slack in growth?

This is my base case for the Australian economy in the next three years, 2% plus growth. It may get on the high side occasionally but much more likely it will undershoot, especially if there is an economic shock. If economic growth hangs entirely on the consumer then any external disturbance could resonate very quickly through Australian economic activity. This is why I have a higher recession risk probability than most. The composition of growth ahead is much more vulnerable than that of the recent past.

Advertisement

As I said yesterday, in the short run the equities cheer squad will quite possibly have its way with cyclicals. And traders might consider this an opportunity. But sustained earning growth faces big structural headwinds, to put it mildly.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.