Once again the data coming out of the Eurozone is looking up, with the latest PMIs showing a broad improvement in both services and manufacturing indexes.

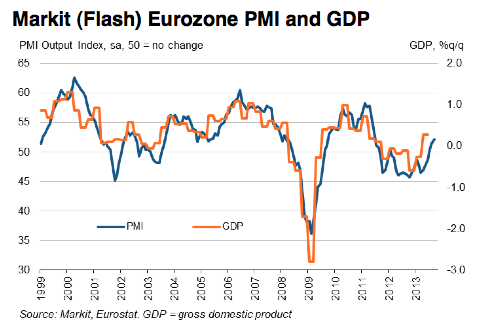

Flash Eurozone PMI Composite Output Index at 52.1 (51.5 in August). 27 – month high.

Flash Eurozone Services PMI Activity Index at 52.1 (50.7 in August). 27 – month high.

Flash Eurozone Manufacturing PMI at 51.1 (51.4 in August). 2 – month low.

Flash Eurozone Manufacturing PMI Output Index at 52.1 (53.4 in August). 3 -month low.

The Markit Eurozone PMI Composite Output Index rose to a 27 – month high in September, signalling the largest rise in activity since June 2011, according to the flash estimate. The flash PMI rose for the sixth consecutive month, up from 51.5 in August to 52.1. Business activity has now risen for three successive months, and September rounded off the strongest quarterly expansion since the second quarter of 2011

Higher levels of business activity were driven by faster growth of new business. New orders increased for the second successive month in September, growing at the fastest rate since June 2011.

The upturn was broad-based across services and manufacturing, although only the former saw growth accelerate in September. Services activity rose for the second month running, expanding at the fastest rate since June 2011. This was fuelled by a second monthly increase in new business placed at service providers. Further expansion is also likely in the coming months as expectations about activity in one year’s time improved to a one-and-a-half year high in the sector.

Manufacturing output meanwhile rose for the third straight month, although the pace of growth slipped from August’s 27-month high. Nevertheless, manufacturing has seen the strongest quarter of growth since the second quarter of 2011 in the three months to September, pulling firmly out of the downturn seen in the previous quarter. New orders in manufacturing likewise rose for a third consecutive month, though growth also eased from August’s recent high. New export orders for goods rose solidly, growing at a rate only slightly less than August’s 27-month peak.

So once again we are seeing some good data out of Europe. You can see my previous posts on this topic, but the basic premise is covered below:

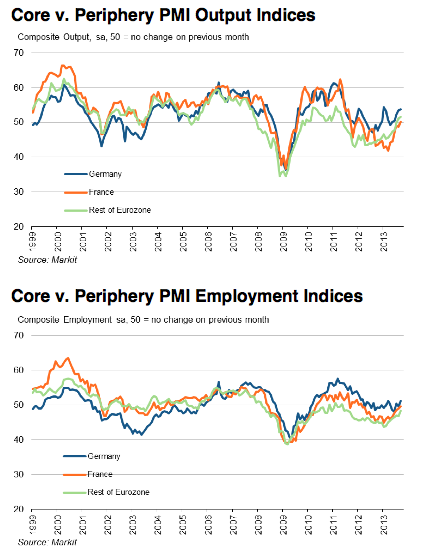

So positive news again ? Yes, but again I feel the need to state the caveats on all of this. Firstly, as I covered in one of the first ever European economy posts I put on MB back in 2011, the major structural issue with the entire zone is that German surpluses must be, in a large part, recycled through the rest of eurozone. Secondly, and in tandem with this, other eurozone nations must be willing and able to service the corresponding deficits related to these surpluses in a fixed-currency environment.

As mentioned earlier this week in a cross-post from the conversation, and something I covered back in July what we have seen over the last 6 months in the eurozone is a relaxing of austerity policy that has given extra time and larger buffers to government in many nations in order to meet their supposed treaty targets. As can be seen from the latest government debt figures , debt to GDP in many nations continues to rise at pace.

Advertisement

Nothing has changed in that regard. Most of the periphery continues to see rising government sector debt to GDP as a compensator for this growth. We’ve already seen the outcome of this in Greece, and without German support others will have to follow, even with this positive data.

As I’ve spoken about over the last few months the question now is exactly what post-election policy will be from Germany. Angela Merkel looks to have secured her position, although there is still some negotiation to be done over exactly what her coalition will be. But the big message out of the election, at least for me, is that the strength of the German economy has killed off any true anti-euro sentiment in the country, with anti-euro parties failing at this election. Whether truthful or not, Angela Merkel has won the political fight over who will set the agenda of Germany in Europe, the question for everyone else, of course, is exactly what that agenda actually now is.

After the election Merkel has already made a number of statements suggesting nothing has changed in her strategy, and given the recent good data that’s an easy sell. However, the fundamental issues of the Eurozone remain today, as they did three years ago. We have seen some timid steps towards a banking union, although the important parts, namely euro-wide deposit insurance and default resolution, remain distant dreams. Banks across much of the region remain under-capitilised and, as the ECB’s latest data shows, private sector lending continues to contract. In compensation for this, public balance sheets continue to grow, overall reaching 92% of GDP, with countries like Italy, a country with serious demographic and economic growth issues, continuing to lead the pack in the wrong direction.

Advertisement

A pickup in the global economy may well provide some support to the Eurozone as it has done over the last 2 quarters, but there are still no steps towards fiscal unification, and if Greece is any guide, any sort of public write-down of debt is still an unaddressed issue, with the preference to impede the private sector, which in turn further depresses the economy.

In short, we are still seeing good data, unemployment aside, on the back of external demand and a loosening of austerity. Whether that continues has quite a lot to do with what happens next in German domestic politics.

Chancellor Angela Merkel says she sees no need for change in Germany’s policy toward Europe after an election win that was impressive but leaves her needing a new coalition partner. Merkel’s Union bloc won 41.5 percent support Sunday and finished just short of an absolute parliamentary majority. However, Merkel’s coalition partner since 2009 crashed out of Parliament and she will have to seek a new alliance with center-left rivals.

Attention abroad is likely to focus on whether there’s any change to Merkel’s policy of aiding struggling European countries in exchange for austerity and reforms. Merkel said Monday she says she needs “no need for change” from her conservatives’ point of view but she won’t anticipate the outcome of coalition talks.