Once again we are seeing more positive data out of Europe with the Flash PMIs coming out overnight.

Eurozone recovery gains momentum with fastest growth for over two years

- Flash Eurozone PMI Composite Output Index at 51.7 (50.5 in July). 26 – month high.

- Flash Eurozone Services PMI Activity Index at 51.0 (49.8 in July). 24 – month high.

- Flash Eurozone Manufacturing PMI at 51.3 (50.3 in July). 26 – month high.

- Flash Eurozone Manufacturing PMI Output Index at 53.4 (52.3 in July). 27 -month high.

The Markit Eurozone PMI Composite Output Index signalled the largest monthly increase in business activity for over two years in August, according to the flash estimate. The PMI rose for the fifth successive month, up from 50.5 in July to 51.7, the highest since June 2011. The above – 50 readings signal two consecutive months of rising output, in contrast to declining business levels over the prior 17 months.

Both manufacturing and services reported higher output in August, with goods producers reporting the larger increase. Manufacturers reported the fastest growth of output since May 2011, while service sector activity showed the largest increase since August 2011.

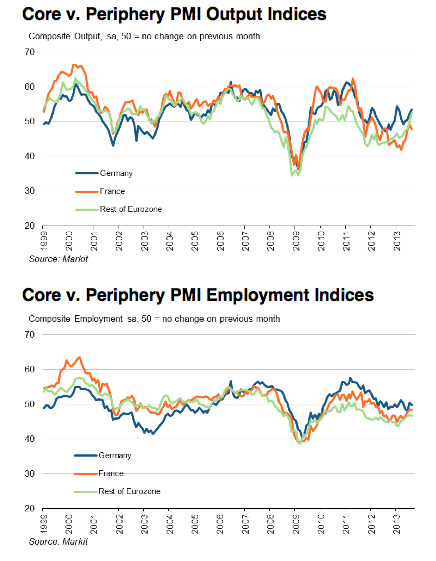

Germany saw output rise at the fastest rate since January as new orders posted the second – largest rise seen over the past two years. In manufacturing, the PMI rose to a 25 – month high, while services growth was the strongest for six months. In contrast, France registered a faster drop in output than in July. Services activity fell at a sharper rate and there was a renewed decline in manufacturing output, but the overall downturn in manufacturing (as signalled by the PMI) held steady at a marginal pace.

Output across the rest of the eurozone rose for the first time since May 2011. Growth of both manufacturing output and services activity was recorded, with the former rising for the second successive month and the latter showing the first increase since May 2011.

Comments from Markit Economic’s chief economist again provide a positive, yet guarded summary of the data.

“The euro area‟s economic recovery gained momentum in August, with manufacturing and service sector companies reporting the strongest pace of expansion for just over two years.

So far, the third quarter is shaping up to be the best that the euro area has seen in terms of business growth since the spring of 2011. The economic picture from the surveys is therefore coming into line with policymakers‟ expectations of a modest yet still fragile return to growth.

The upturn is being led by Germany, where growth accelerated again in August, driven in turn by rising domestic and export demand. A big question mark still hangs over France‟s ability to return to sustained growth. Although the French PMI is well above the lows seen earlier in the year, August saw a slight steepening in the rate of contraction, notably in services – which points to lacklustre domestic demand.

The dataflow continued to improve outside of France and Germany, suggesting that a long – awaited recovery seems to be taking shape in the “periphery”. Output and orders rose at the strongest rates since early – 2011, with a broad-based improvement in domestic and export sales suggesting that the recovery is also looking more sustainable.

So positive news again ? Yes, but again I feel the need to state the caveats on all of this. Firstly, as I covered in one of the first ever European economy posts I put on MB back in 2011, the major structural issue with the entire zone is that German surpluses must be, in a large part, recycled through the rest of eurozone. Secondly, and in tandem with this, other eurozone nations must be willing and able to service the corresponding deficits related to these surpluses in a fixed-currency environment.

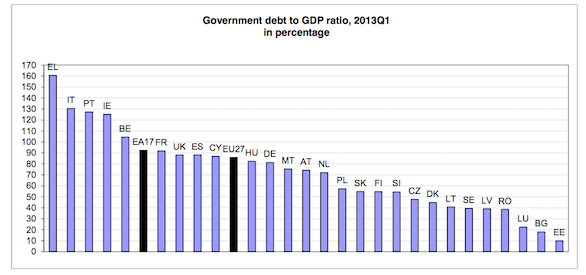

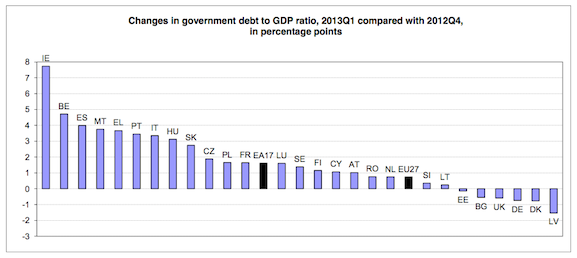

As mentioned earlier this week in a cross-post from the conversation, and something I covered back in July what we have seen over the last 6 months in the eurozone is a relaxing of austerity policy that has given extra time and larger buffers to government in many nations in order to meet their supposed treaty targets. As can be seen from the latest government debt figures , debt to GDP in many nations continues to rise at pace.

This relaxation certainly isn’t a surprise, in fact, as I stated back in December 2011 this was the inevitable outcome of Europe’s suicide pact.

So while there is no credible counter-balance for the effects of supra-European austerity any attempt to implement the new “fiscal compact” will make Europe’s economic issues worse. The continent is already on the way to recession and unless we see some additional action from the ECB, or a huge swing against this new framework, the push to implement the outcomes of the summit will simply accelerate that outcome. My assumption is that, if Europe does ratify this framework (there are a few stragglers), after 12-24 months of trying the effect will be so disastrous that they will eventually give up. But until then my base case for Europe is a significantly worse economic outcome.

The problem is, of course, that none of this actually fixes the underlying issues. The zone does appear to be returning to growth, but in most part due to the fact that governments have been allowed to let their automatically stabilisers work more effectively by letting deficits continue to grow, therefore assisting the private sectors of their economies, but not addressing major issue of debt imbalances.

The question I have been asking myself since the start of the year is whether this new strategy is a short term plan, based around the domestic politics of German, and therefore likely to rapidly be reversed come October, or whether it is something more long term. A recent article from a German daily gave me some hope that it is the later.

Greece’s third aid programme will likely be financed at least in part by the EU budget, German daily Sueddeutsche Zeitung reported Wednesday citing sources involved in the negotiations.

Germany’s finance minister, Wolfgang Schaeuble, said Tuesday that Greece will need a third aid programme once the current one expires at the end of 2014. At the same time, Schaeuble excluded another haircut on Greek sovereign debt.

“Making additional money from EU structural funds available to Athens is under discussion. With the money Greece could stimulate its economy while national funds would be freed up to service the debt,” the paper said.

In the absence of a haircut “real transfers from the EU-budget or budgets of partners” are the only remaining option, the paper said.

According to the paper, additional loans would not help as these would further drive up excessively high debt levels.

Any new programme would be significantly smaller than the previous two, the paper said.

So the transfer union you have, when you aren’t having a transfer union then? Time will tell, but if it is the case, it is yet another slow but subtle creep away from the previous delusional policies of the Eurozone. In short, the data is looking up, but it’s the post-election politics of Germany that matter now as to whether any of this is going to be sustained.

Full German , French and Eurozone PMI reports available at Markit Economics.