Goldman today offers a take on Rio’s recent analyst tour with which I completely agree:

We provide our key takeaways from our site visit to Rio Tinto’s Pilbara iron ore business. Qualitatively, Rio’s Pilbara operations are impressive due to the sheer scale and quality of the assets and high morale across the business. In terms of impact on the investment case, our key takeaways were:

1. Pilbara 290 has commenced shipping and will be delivered on an accelerated ramp-up, producing an incremental c.10mn t in 2013.

2. Pilbara 360 infrastructure construction appears ahead of schedule and could be ready to ship late 4Q14 – worst case 1Q15.

3. Pilbara 360 ramp-up communication is unchanged. Rio has multiple mining options to fill the capacity. We expect no decision until late

2013/early 2014 and uncertainty to continue.

Implications

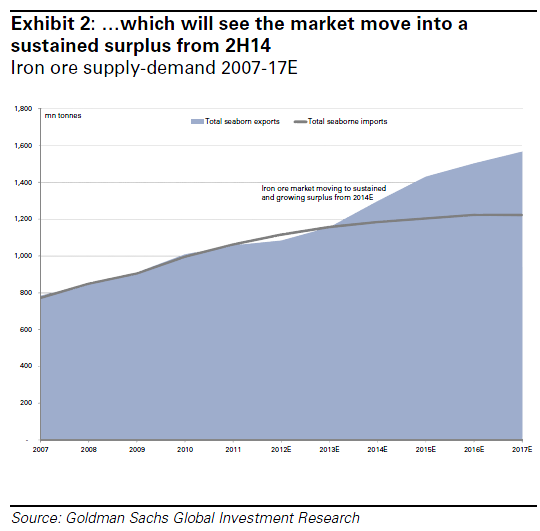

Focusing purely on the investment case, not that much changes – the iron ore price remains the critical factor. We know that Rio’s assets are high quality and the company’s recent execution record has been very strong – it’s hard to see any upside from better-than-expected execution by Rio. That puts all the focus on the iron ore price to move earnings, and we forecast c.400mn cumulative new tonnes by 2015 seeing the iron price decline to an US$80/t CFR average in 2015, a level at which we forecast Rio’s P/E would be c.13.4x (vs. 8-10x recent average). No change to Neutral rating on RIO.AX.

UBS offers us Rio’s riposte:

Chinese domestic iron ore supply: Rio believes Chinese domestic iron ore production is highly price sensitive. Based on third party research, it estimates there is ~340Mt of iron ore (62% equivalent) produced in China, of which ~70% is owned privately. It believes ~50% of this has a cash cost >$100/t and this is “increasing strongly” due to an appreciating currency, a move to underground mines, as well as rising power, wage and other input costs. Rio believes in the past (2010, 2011 and 2012) these producers have acted rationally and quickly to a changing price environment.

Rio admits Chinese production could be stickier than they think but falling Fe grade can’t be reversed. The key growth region in china is the coast. The usage of water is a key risk for China. Water usage is a key social, political factor impacting the mining industry. With ~70% of production private, Warwick Smith (MD, Sales & Marketing) struggles to see how Beijing will support a private mining industry like they did with steel/aluminium.

The one thing we can be nearly certain of is that the Chinese will not act “rationally”. They will fight tooth and nail for every tonne. We already have the example of the two coals to tell us that. Quite apart from the economic considerations of local governments, steel production is a strategic output for the CCP and I do not that they will be comfortable offshoring inputs to a died-in-the-wool US ally.

Advertisement

Whether he knows it yet or not, this will be the defining issue of Tony Abbott’s Prime Ministership.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.