We complete the portfolio’s rotation away from its exposure to high yield/defence & continue lifting exposure to earnings that are leveraged to either global growth or the emergence of a domestic recovery.

We have exited the long-held defensive/yield exposures to TLS and CCL. Also having inherited a NWS position post the News Corp split, we exit NWS also, although continue holding the O/W in FOX. We have rotated to a range of cyclical exposures by adding RIO, moving the portfolio to an O/W to Mining, given the portfolio‟s already significant O/W to BHP. As well we have added to the portfolio‟s domestic cyclical exposure via SEK & WES, while also adding FLT to the portfolio‟s long-standing large O/W position to “growth”.

Outlook

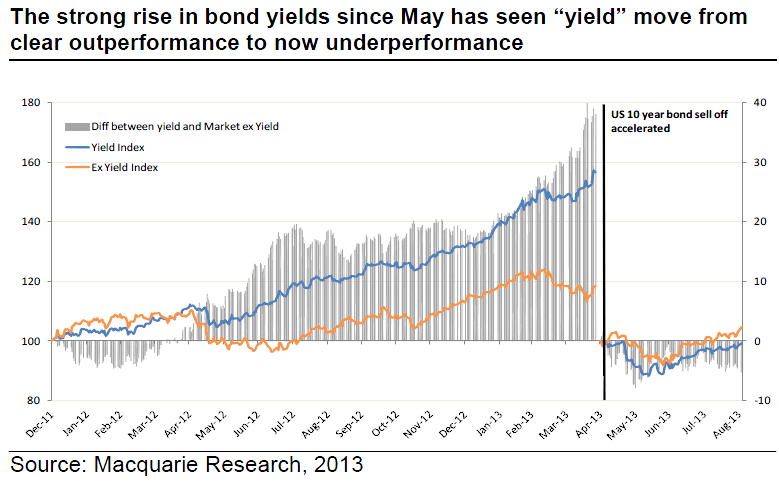

These changes to the Strategy portfolio reflect our view that the long grinding cycle down which has seen global growth running at sub trend is now progressing to the long grinding cycle up. The rise in bond yields globally, including Australia, is the clearest signal of this cycle turn and is a critical signal to equity investors to rotate from defence and toward risk. The modest improving economic signals driving this lift in bond yields, particularly China had led to the portfolio‟s now modestly positive stance on Mining through RIO.

Australia‟s GDPg has weakened and we expect growth will weaken further. However policy response, particularly interest rates and a weaker A$, will likely gain traction as we move into CY14 and hence we added selectively to our domestic cyclical exposures through WES & SEK.

Hmmm. I’m not convinced. Like Macquarie, I see the economy getting worse before it gets better. Unlike the millionaire’s factory I see monetary policy continuing its struggle to get traction (everywhere but Sydney property!) and thus cyclicals do not present themselves as a good option. In my view, even the risk that property rises spread to other cities does not proceed to higher growth. I expect households will keep the purse strings tight.

This leads to the conclusion that the dollar will have to keep falling or local growth won’t recover. Therefore Macquarie’s mining picks might be more attractive. In a separate note today it argues commodity prices are showing strength:

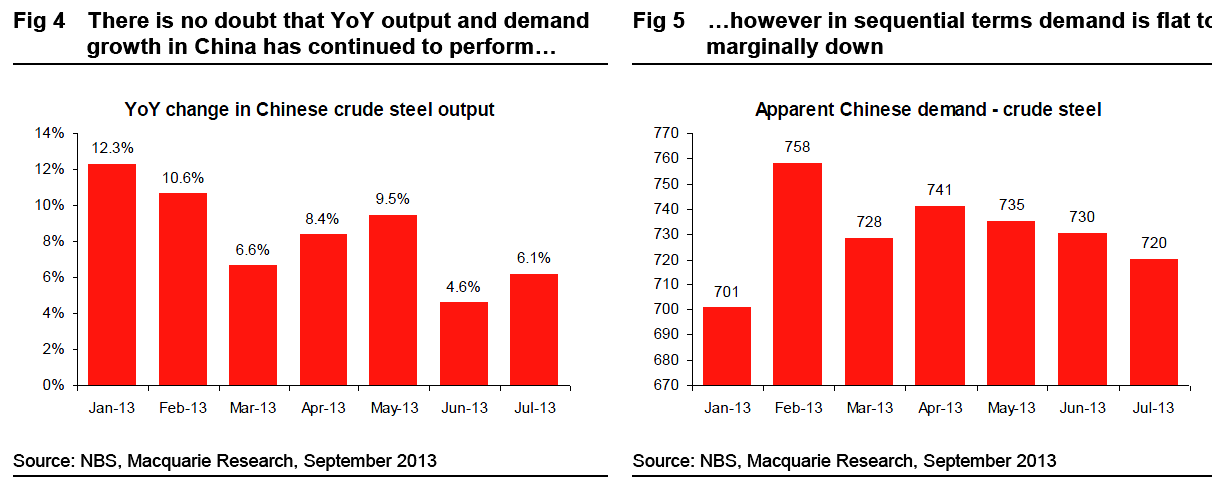

August proved a surprisingly strong month for metals and bulk commodity price, with better than expected macroeconomic data driving a rally in exchange traded commodities, backed up to a lesser extent by the majority of those set in the physical market. However, in many cases this was a reaction to data releases from July rather than demand breaking the shackles of supply. Certainly, the H2 2013 demand outlook is better than may have been expected, however this may only serve to provide stability rather than price upside.

In general, industrial metals prices move strongly one way or the other when China and ex-China are either picking up or reducing demand at the same time. Certainly, economic indicators for developed markets continue to improve, leading to a stronger „core buyer‟ for commodities. Moreover, sentiment in China remained very strong in the month, as government attitudes towards real estate continued to soften and order expectations improved (as highlighted in the Macquarie China Steel Sector Survey). However, it seems more that developed world investors, who had extremely low expectations for China and thus industrial commodities, were surprised by the strength of Chinese data points in the month.

This certainly led to a bout of short covering in exchange traded metals, with the LMEX base metals index recording its best MoM move for the year – up 4.2%. Aluminium underperformed, rightly in our view, as the market continues to undergo a rebalance as LME warehouses stop being a demand line in our supply demand model. Meanwhile tin rose more than 10% as concerns over Indonesian supply grew, however recent moves in the rupiah will take some pressure off producers in the coming months.

Advertisement

I agree with this thesis and see little that’s sustainable in China’s current bounce. Given the PBOC’s refusal to cut rates, rebalancing still looks like a Chinese priority to me and I continue to think that we’ll be confronting the same old questions about Chinese growth prospects as this pulse fades in the new year. I expect the same long, slow struggle in the US as it slogs through higher interest rates and any lasting rebound in Europe depends entirely whether the Germans are playing possum for their election.

The long and the short of all that is another year of subdued global growth, though better than this year. Certainly the iron ore producers are benefiting with the dollar down 15% and iron ore trading at $138. Having said that, the costs of the major miners are mostly in US dollars so the uplift is not as good as it looks. Combine that with the coming supply-side pressure on the iron ore price and next year is not favourable to miners either.

A shift into cyclicals is warranted but my favoured allocation remains dollar-exposed industrials.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.