The RBA’s biannual Financial Stability Review is out and, disappointingly, omits of any mention of macroprudential rules. What it does do at least is identify Sydney and SMSFs as a building risk:

Over the past year or so there has been an increase in property market activity. This is not surprising given the reductions in interest rates. The pick-up in demand, which has been sharper in New South Wales and from investors more generally, has been associated with recent increases in housing prices. It is important that those purchasing property do so with realistic expectations of future dwelling price growth.

In this issue of the Review, a particular focus has been placed on the self-managed superannuation fund (SMSF) sector. Although this sector does not currently pose material risks to financial stability, it is important for the financial position of the household sector and has a number of aspects that warrant careful observation in the period ahead.

Changes to legislation in recent years have permitted superannuation funds, including SMSFs, to borrow for investment, for example to purchase property. Since then, property holdings by SMSFs have increased and this type of investment strategy is being heavily promoted. The sector therefore financial stability review represents a vehicle for potentially speculative demand for property that did not exist in the past. SMSFs and other retail investors have also been the dominant class of purchasers of hybrid securities recently. These investors seem to have been attracted by the higher yields offered on hybrids compared with conventional debt securities; it is important that they fully appreciate and price in the risks embedded in these more complex products.

So much for the obvious. What are we going to do about it? Talk, it seems.

Some signs are emerging that the low interest rate Graph 3.15 environment and recovery in asset prices have encouraged a slight shift in household preferences towards riskier investments. Survey data suggest that over the past year or so, the share of households that believe that paying down debt is the ‘wisest’ use of their savings has decreased, while the share favouring equities has increased, though it still remains quite low at around 9 per cent (Graph 3.14). While increased financial risk-taking is an expected outcome of lower interest rates, it is important that households understand, and appropriately account for, the financial risks they take.

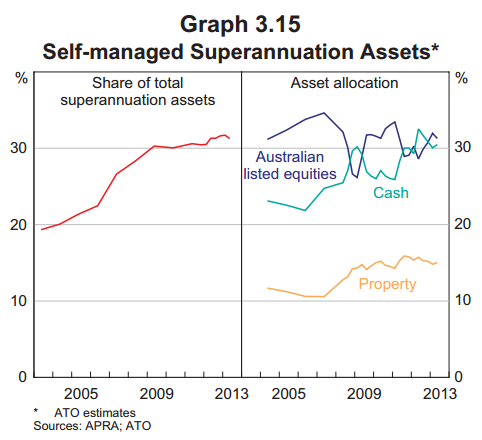

An avenue through which households may be taking more risk is in the management of their superannuation assets. Over the past decade, there has been a sizeable movement of assets into SMSFs from other fund types; the number of SMSFs has roughly doubled over this period and the sector now accounts for almost one-third of the $1.6 trillion in superannuation industry assets in Australia (Graph 3.15). SMSFs allocate a relatively large share of their assets (15 per cent) to direct property holdings (both commercial and residential); this share has increased over the past six years, partly driven by legislative changes that have allowed superannuation funds to borrow under limited recourse conditions (see ‘Box D: Self-managed Superannuation Funds’ for more details).

One risk of the increase in property investment by SMSFs is that at least some of it is a new source of demand that could potentially exacerbate property price cycles. It also raises consumer protection concerns in the event SMSF members are exposed to greater financial risks than they envisage. An Australian Securities and Investments Commission (ASIC) report, released in April, identified that while most advice given to individuals about SMSFs was of good quality, there were pockets of poor advice, particularly related to geared residential property investment. In response, ASIC has expanded the information on its MoneySmart website to highlight the rules, costs and relevant considerations around SMSFs and residential property investment. It has also recently released a consultation paper that sets out proposals to impose disclosure requirements on advisers, including on matters that may influence an individual’s decision about whether to set up an SMSF.

In addition, ASIC commissioned research to examine the minimum cost-effective balance for an individual to set up an SMSF and is also proposing to provide guidance that advisers inform individuals of the costs associated with having an SMSF.

There is also evidence that SMSFs have been a large part of the recent demand by retail investors for the non-common equity capital being issued by banks, as well as hybrid securities more generally. These instruments attract a high yield as they combine features of debt and equity, and are also quite complex products that carry higher risk than more traditional debt securities. It is therefore important that these risks are adequately communicated to, and understood by, the purchasers of these products.

For the financial system, the direct near-term risks arising from lending to SMSFs are likely to be small. Despite overall lending to SMSFs having grown strongly for several years, it still accounts for a small share of overall bank lending. In addition, any increased risks to banks posed by limited recourse arrangements are largely offset by their frequent requirements for personal guarantees from SMSF members; minimum fund net asset requirements; and lower maximum loan-to-valuation ratios (LVRs) than often imposed on other property lending. In any case, the rapid growth of the sector warrants ongoing monitoring, and it is important that banks maintain sound lending standards and practices.

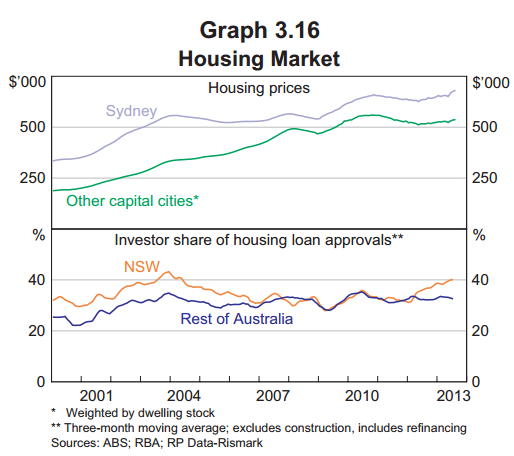

In addition to SMSFs, there has been a broader increase in residential property market activity over the past year or so. The increase in investor activity in New South Wales appears to have been particularly sharp; investor housing loan approvals now account for around 40 per cent of the value of loan approvals in the state, a share last recorded in 2004, although some of this no doubt reflects a decline in first home buyer activity (Graph 3.16). The increase in investor activity has been associated with a recent pick-up in Sydney housing price growth and reports of sale prices exceeding price guidance and valuations by wide margins. An increase in housing market activity more generally is not surprising given reductions in interest rates. However, it is important that those purchasing property maintain realistic expectations of future dwelling price growth; in contrast to the decades leading up to the crisis – when dwelling prices grew rapidly in response to disinflation and financial deregulation – long-run future growth in dwelling prices might be expected to be more in line with income growth.

Advertisement

I think it is already clear that Sydneysiders won’t give a hoot about income growth, until you make them.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.