From The Australian over the weekend:

FINANCE Minister Mathias Cormann has warned of a hit to the economy from the sharp rise in the dollar as he and his colleagues mull a delay in the next budget update to deal with the threats.

As global forces push up the currency, the Abbott government is confronting new risks to tax revenue as it proceeds with a commission of audit to cut spending and shake up the public sector.

…”Of course the level of the Australian dollar is for the market to determine, however, a stronger currency clearly has implications for our international competitiveness,” he told The Weekend Australian yesterday.

Tax revenue fell sharply from May to the budget update issued before the election, adding billions of dollars to the deficit and raising concerns about further changes in the next update.

The Weekend Australian understands there has been some deterioration in revenue since then.

This is not terribly surprising given the parlous state of the economy. The more important question is what will happen longer term to revenue and spending. Last week’s sensible (if hypocritical) backflip by new Treasurer Joe Hockey has lifted hopes that the new government will support growth via increased infrastructure spending. We already know that the mining investment cliff will draw down at a rate of 1-2% of GDP for the next three years. We can add to this other sectors which are still cutting back, driven by a high dollar, weak demand and the push for yield by investors.

Joe Hockey’s current project pipeline amounts to about 0.3%-0.4% of GDP, which could provide an offset. But a new report from Citibank shows that that hope faces two severe headwinds:

Declining spend near-term — With resource capex likely having peaked in FY13 and in decline from FY14, the onus is on infrastructure to help fill the gap. The change in Federal government looks positive for infrastructure spend, but doesn’t change the outlook for declining Australian infrastructure spend over FY14-15. Changes to the PPP model have increased private sector capital demand for road and rail projects, but long lead times mean we are unlikely to see Australian infrastructure spend stabilising until FY16.

Government infrastructure spend under pressure — The Federal Coalition’s intentions are encouraging for infrastructure spend. However, with 80% of government infrastructure spend funded by the states, and state infrastructure budgets declining 20% over FY15-17, the majority of infrastructure spend heavy lifting falls to the private sector. Government asset sales will play an increasing, but still somewhat limited funding role, given high value electricity poles and wires are off the near-term agenda.

Private sector to play bigger role in infrastructure funding — Government reforms to PPP financing and bid models have led to a better allocation of PPP risks between government and private sector, including government taking on traffic risk and contributing to project funding. This has increased private sector equity and debt capital demand for PPP projects like East-West Link and WestConnex. Given long lead times, it’s likely not until FY16 that the next wave of mega Road and Rail projects ramp up.

We forecast Engineering Construction spend to fall 13% over FY14-15e — Our forecasts for Engineering Construction spend (ex direct resources) to fall 4% in FY14 are unchanged. We downgrade FY15 from -6% to -9% due to weaker resource related Rail and Port, Power and Water capex. We forecast flat growth in FY16, with growth in Roads and Telco offset by declines in Power and Rail and Port. Over FY14-15 we forecast: Roads (-16%), Rail and Port (-24%), Power (-7%) and Telco (+19%).

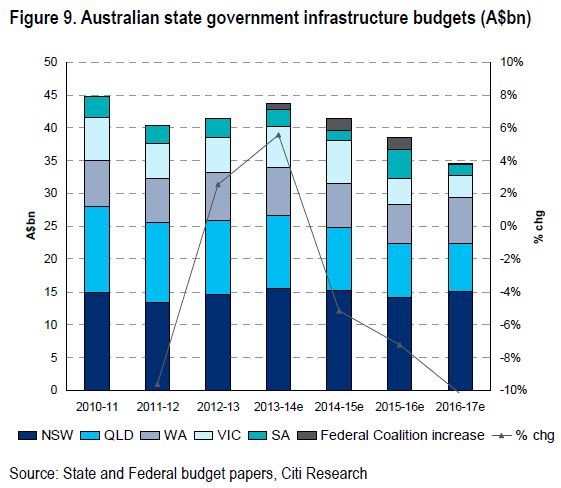

Here is the key chart summarising state and federal public capex:

\

\

What’s wrong with $40-odd billion in infrastructure investment some will ask? Nothing, except the level is secondary. What matters to growth is the rate of change and as you can see it is falling about $2 billion per annum for the next three years. That’s not a big withdrawal from growth, only 0.1-0.2% of GDP, but it sure isn’t providing any offset to the mining cliff.

This has several implications for investors. The first is that those looking for a bottom in engineering construction firm earnings had better think again. Second, there is virtually no chance that the economy is going to force the RBA to raise interest rates (though housing might). Third, those playing in the Sydney housing blowoff had better have itchy trigger fingers. Fourth, there is going to be a temptation for much higher federal spending and Hockey/Abbott could end up with very large deficits in their first term. Fifth, in this environment, cutting back the off-balance sheet spend around the NBN is crazy politics and if the Abbott government isn’t already thinking backflip it should do so pronto. Fifth, even with the added federal investment, the dollar will need to fall to 60 cents and below if we are to dodge a very nasty adjustment.