China. The name once evoked mysteries of the orient: opium, corruption and the ineffable other. Today it is more solid, touchable in the endless ream of steel it rolls out for itself and the world, as well as in the massive iron ore developments of the Pilbara. But it also remains a conundrum, with raging debates about how sustainable is its extraordinary rise? How long can it continue to invest in and build huge amounts of infrastructure and housing? How long can it buy hand over fist Australian bulk commodities? How durable is its state as it pursues both economic liberalisation and political totalitarianism?

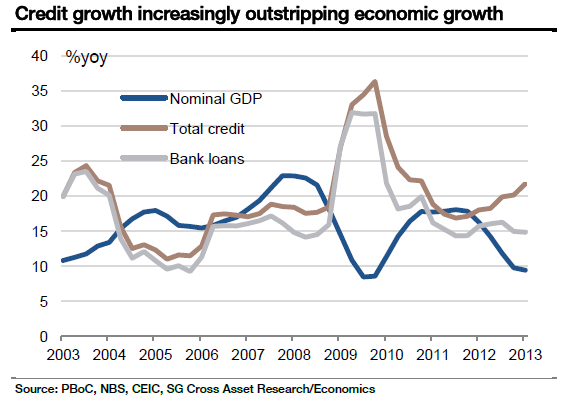

Over the past two years these questions have become more and more hotly debated in a contest between two economic narratives. The main point of contention is China’s extraordinarily high investment levels at 46% of its GDP growth (by comparison Australia is a measly 24%). The recent rebound in growth is, once again, driven almost exclusively by rises in publicly funded infrastructure.

The bearish school, led by Professor Michael Pettis of Peking University, argues that to keep its high growth rates going China has had to engage in a form of long term “financial repression”. By that he means that interest rates have been held at artificially low levels for a very long period to enable banks to keep lending to unproductive enterprises and governments, especially those engaged in building infrastructure.

The result has been very high levels of growth as investment has surged. Evidence for this viewpoint can be found in the declining growth on each borrowed dollar that China is receiving.

A second, more optimistic, school of thought sees China’s high investment rates not as a result of any policy machinations but the simple fruits of a development economy still in the early stages of its embrace of capitalist reform. High urbanisation and infrastructure investment rates are, they argue, the natural corollary of this condition and will fall in time as the economy moves up the value chain.

Development economics

Making a judgement about which of these two arguments is right is vital to the Australian economy and its reliance upon the bulk commodity exports that have fuelled China’s investment boom. To decide, let’s take in some history.

The rise of China is a well understood phenomenon. It began in the seventies with the embrace of capitalism. The reform era, as it is known, brought the Western ideals of private sector dynamism to together with the most abundant and cheap labour in the world. What followed was an explosion of economic growth that persists to this day.

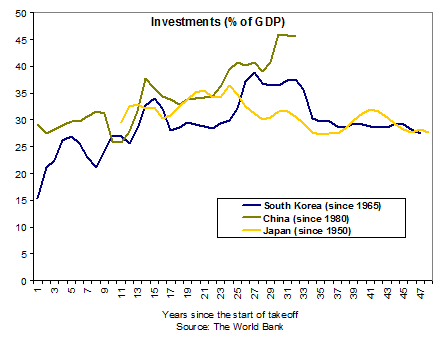

This was not some miracle, however. In fact, China simply followed a script of development written for it by Japan and then Korea decades earlier. Open up to trade and inwards investment, allow labour to be mobilised by foreign capital and unleash the productivity potential of the nation through heavy investment in urbanisation and infrastructure to modernise the economy.

In short, it is not difficult to invoke powerful growth in an under-developed economy. The dynamics are well understood. Many nations have succeeded at various times, including much of South America, Southern Africa and most of Asia. This is widely known as the economic policies of “catch up” growth.

But there is a problem. Although it is relatively easy to get such a transformation underway, once an economy reaches a certain point of success, when labour supply gets tighter and incomes have risen materially, it suddenly gets much harder to generate high rates of growth.

The reason why is not complex either. Rising wages reduce competitiveness and formerly dynamic but labour intensive export industries begin to wane before the economy has made the jump to the more sophisticated value-add activities in exports and services that are the hallmark of developed economies.

As well, if the nation has a natural resource endowment (as many do) then extractive industries can hog capital and favoured political decision making, as well as drive up currencies, again hitting competitiveness. The vested interest problem can apply to other industries too that have benefited from the early phase development and are threatened by renewed creative destruction. All of these weights can combine to retard swift growth in what is known as the “middle income trap”.

Far fewer nations have made the leap from fast early-phase development economics to equally fast post middle-income development. Japan and Korea are outstanding examples but many more have failed or stagnated for long periods.

The secret of those that did make the transition was that when they reached the point at which growth began to slow, they did not rest on their laurels. Reform turned from opening up to capital, mobilising cheap labour and heavy investment in infrastructure to liberalising capital markets so that they may prioritise returns on investment, labour was driven to higher value-add industries through shifting investment to soft infrastructure like education and health and the overall economy was mobilised for innovation and productivity gains. These, in turn, drove income growth and ongoing high growth rates.

As a result, the infrastructure investment that drove much of the high speed growth in the early phase of development begins to fall, though investment rates remain high. This is where China finds itself today:

China’s choice

Returning to our central question then, what will China choose to do, the first observation we should make is that the two schools of thought about China’s current challenge are much closer together than they appear. Whether you are focussed on the debt and macro settings governing capital allocation or you’re focussed on the development economics of urbanisation, the next phase of Chinese development requires the same basic reforms: liberalised finance, innovation policy and soft infrastructure investment.

The difference is in the forecast outcomes. The pessimists see growth falling to developed economy levels. The optimists see growth continuing at 7% or more for another decade.

Importantly, however, for Australia and Australian investors, the outcome is more clear cut. If the pessimists are right, Chinese growth will fall along with infrastructure investment and commodity prices will too. However, if reform proceeds as the optimists demand, fixed asset investment will still fall but be replaced more swiftly by other forms of less commodity intensive growth. In short, China will be fine but commodity prices will not be.

Either way, Australia and its miners lose.

So, is it a no-brainer then to sell miners? No, it’s not. Timing is everything. China is sending very mixed signals about when it intends to seriously embark on the reform process. Both the former leadership of Wen Jai Bao and that of the new in Li Keiqing have openly acknowledged the problem, yet both have continued to roll out mini-stimulus packages aimed at fixed asset investment and propping up the old model of growth, making the risk of stagnation worse.

This article is not long enough to enquire into the intense machinations of Chinese politics but it appears that China is bitterly divided between the reform-minded new government and those interests aligned with former President Jiang Zemin, which included the recently retired Prime Minister Hu Jintao. Zemin is heavily associated with the Shanghai elite that benefited spectacularly from the old development model and will lose if economic liberalisation is embraced.

Premier Li is a reformer and the theory runs that the current flush of Chinese stimulus is designed to give the new regime enough time to corner its opponents so that reform can be prosecuted with the greatest vigour once political dominance is established.

That leaves us with two potential scenarios for Chinese growth:

- the reformers win and begin the rebalancing project in earnest, causing large falls in bulk commodity prices from mid-2014 (as well as the supply deluge already pushing them down) but either high or moderate growth continues in China

- the reformers lose and China lurches from stimulus to stimulus through another cycle that supports bulk commodities for several more years, culminating in stagnation and a Chinese financial crisis.

What should investors do?

Predicting the timeline for these events is impossible. But in the short term the massive supply response in the bulk commodities is likely to pressure prices even if China elects to postpone its adjustment. Earnings for the miners could still be good and given low valuations a decent rally is possible as markets focus on the cyclical over the structural.

It is also possible that such a process will see the Australian dollar stabilise at current levels until China’s structural challenge reasserts itself.

But in the medium and long term, the probable outcome is that Chinese reformers will prevail in the view that the costs of reform now outweigh the costs of the status quo. Either that or crisis ensues sooner or later.

Long term investors are thus better served looking beyond local miners for gains and can still be confident in a lower Australian dollar within an acceptable time frame.

This article is not investment advice.