The AFR has few quotes this morning from currency stirrers:

The Coalition victory, more positive economic data from China and a diminished case for tapering the United States’ massive stimulus program have conspired to keep the currency above US90¢ and poised to rise.

Perennial Value managing director John Murray sees no reason the currency won’t trade higher on the confluence of events over the past three days. “I’ve been thinking for quite some time going forward, [the Coalition victory] in itself that would be seen to be a positive thing.

…“Importantly, that will be received as a positive by overseas investors as well. That’s something that’s been a little bit forgotten, just as domestic participants in the economy have lost confidence, overseas investors have done the same thing.”

Mr Murray increased his exposure to resources stocks after a trip to China two months ago left him with the impression that investors were overly bearish on its economic outlook.

Poppycock! Unless an election is going to influence the economy’s fundamentals then it’s going to have a brief effect or none at all.

Still, the election is a timely moment to revisit our five drivers model of the currency’s value. What do they say now?

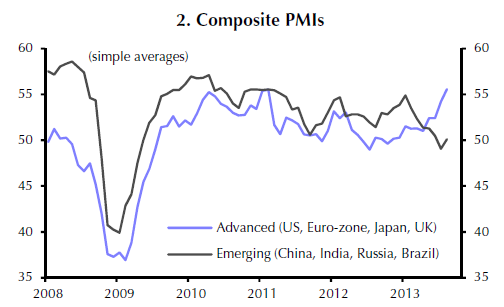

The first driver is global growth and China in particular. Global growth in prospect is stronger with PMI momentum strong. From Capital Economics:

As you can see, the bounce is concentrated in developed markets is unlikely to push up commodity prices past the current rebound, so the influence on the dollar should be limited. In terms of China, the dollar fell very heavily in April-June in part because of China’s credit crunch. Australian bank funding costs spiked as well. Since then, as China has stabilised, the dollar and funding costs have too while other commodity currencies have been much weaker than the Aussie. We’ll need to see a greater shift away from rebalancing from the new government for this to be an ongoing driver.

The second driver is the value of the US dollar. This has been less clear cut that many thought as the deflating Treasury bubble has prevented tightening policy from pushing up the greenback. But the Fed will not stop discussing the taper whether or not it goes ahead this month and bond yields have already priced a lot of the shift so I’d expect the US dollar to remain in an up trend.

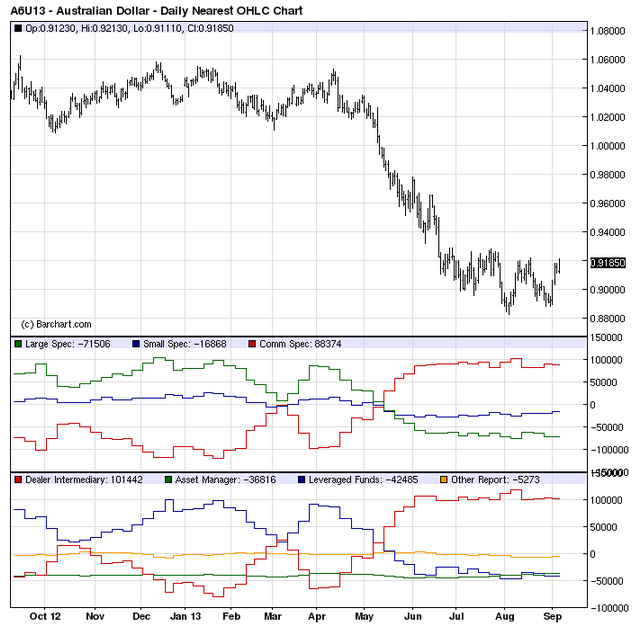

The third and fourth drivers are technicals and sentiment. As I noted last week, the dollar has a double bottom pattern in place that could support a rebound but the overall trend remains firmly down. In terms of sentiment, on the weekly Commitment of Traders report, large and small speculators remain very short the Aussie which could be taken as supportive or ripe for short covering:

The fifth driver is monetary policy. Will the RBA keep cutting or is there a chance that it will have to hike rates? That is all about housing. If the current momentum in the market builds, then the RBA will be forced to act some time mid next year. That will put upward pressure on the currency, in fact the prospect of it will, so it could be a factor by the end of this year. We already know that local interest rate markets have begun pricing rate hikes one year hence.

However, we know that the RBA thinks (rightly) that without a lower dollar the economy will not be able to grow through the capex cliff so it is going to be loath to raise rates. If this conundrum does develop (my base case remains that a weak economy will retard housing) then the chances are that the RBA will be forced to follow the RBNZ into an embrace of macroprudential policy. Still, this scenario will put upwards pressure on the Aussie in the mean time.

The balance of the risks remains weighted to the downside in the short term, but it’s not as clear cut as it was a few short months ago. In the medium term, Australia will have to do whatever it takes to get the currency down: rate hikes, macroprudential policy, fiscal reform or recession. Until we reach such a point, some kind of range trading between 89 and 93 cents seems a decent bet.