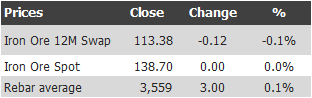

Find below the iron ore price update for September 3, 2013:

Rebar futures were down sharply to a new low for the move.

In news today (yesterday actually) , Rio has suddenly expanded its production guidance range downwards:

Rio, the nation’s biggest producer of iron ore, told analysts in Perth yesterday that the potential production range had widened at its vast network of mines, railways and ports in Western Australia’s Pilbara region.

Iron ore development chief David Joyce told analysts that annual exports from its most profitable business, WA iron ore, could range from 300 million tonnes to 375 million tonnes in 2018. This compares with the range of 360-375 million tonnes provided in May by Rio chief executive Sam Walsh.

The change indicates annual mine production in a worst-case scenario would only rise fractionally from the 290 million tonne level it plans to reach next year after a $US10 billion ($11.15bn) expansion is finished.

Yesterday, Rio gave no reason for the change or any other indications that an expansion halt was on the cards. But it clearly leaves the company’s options open for a more subdued iron ore production profile if conditions change markedly.

Rio has approved expansion of its Pilbara iron ore railways and ports to handle 360 million tonnes per year but has only approved mine expansions up to 290 million tonnes.

At iron ore prices of $US100 a tonne, 30 per cent lower than they are now, the revenue cost of not pursuing the extra mine expansions would be $US7bn a year.

This is Rio’s much celebrated Pilbara 360 project having a shadow cast over it. One presumes that this is part of management’s strategy to try to placate shareholders that want to see short term value realised versus suppressing competitors which want to build supply but are held back by Rio’s massive and swift expansion option. Can it have it both ways? Not for long you would think.

The $7 billion price tag for not going ahead will likely immediately be filled by Gina Rinehart’s Roy Hill, which is not as big but big enough at 55 million tonnes. Another largish producer selling to the Chinese is the last thing Rio wants.

I still say it will have to proceed. 290mtpa at $100 is $29 billion in revenue. 360 million tonnes at $80 is 28.8 billion in revenue, yet you better preserve the oligopoly going the latter route and will get the chance to gobble up other competitors along the way. Profits might take a shorter term hit but the new supply is supposed to reduce cost per tonne as well so that trade-off should be manageable. Long term everything is more profitable controlling supply.