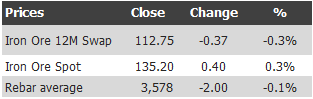

Find below the iron ore price table for September 11, 2013:

A pretty weak response to yesterday’s solid Chinese data, suggesting seasonal weakness holds sway.

However, in news, the Baltic Dry capesize component continues to moonshot:

Advertisement

The cost of shipping raw materials surged the most in more than four years as strengthening steel prices in China spur imports of iron ore used to make the metal, helping owners recover from the industry’s worst slump ever.

The Baltic Dry Index, a benchmark of commodity shipping rates, jumped 9.3 percent to 1,478 today, the biggest gain since June 2009, according to the Baltic Exchange, the London-based publisher of freight rates on more than 50 trade routes. The measure is now at the highest since January 2012, after collapsing from as high as 11,793 in 2008 because of a record shipbuilding program.

China’s imports of iron ore, the single-biggest source of demand for the vessels, expanded 8.1 percent to 526.7 million metric tons in the year to August compared with the same period a year earlier, customs data show. The increase is the result of strengthening steel output and prices in China, according to Fotis Giannakoulis, a New York-based analyst at Morgan Stanley.

“Steel production in China is defying a seasonal slowdown in prices, allowing mills to absorb high iron ore imports,” he said in an e-mailed report today. “As long as high steel prices offer attractive margins for steel mills, there is room for strong imports.”

Daily earnings for iron-ore carrying Capesizes, the largest ships tracked by the index, rose 17 percent to $25,426, the highest since December 2011, according to the exchange. Twenty-six of the vessels were booked last week, up from 16 the week before, according to Morgan Stanley. Spot bookings in the last three months rose 27 percent from a year earlier while the fleet expanded 5.5 percent, Giannakoulis said.

I gave up on the BDI a couple of years ago as oversupply broke the index’s link to activity. But, it has successfully forecast the last two material spikes in iron ore so it’s no longer to be ignored.

There’s no doubt that Chinese production is continuing on its merry way but it’s not as rosy as painted above with steel still in oversupply and pricing relatively weak. I expect the seasonal slowdown to still hold sway over prices but it may be less deep than my $120 thrown dart.

Advertisement

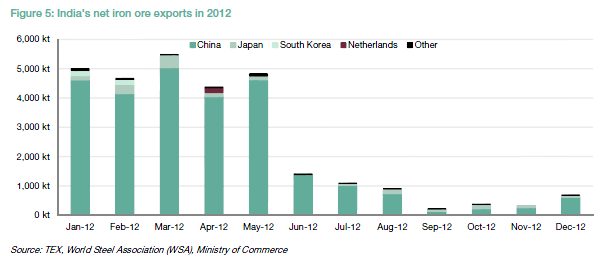

As well, there was a lot of chatter yesterday about a CBA report forecasting a return of Indian iron ore to the seaborne market. It was a useful history of recent Indian missteps and concluded:

Prior to the latest collapse in the Indian rupee, we had tentatively anticipated that India would need to import iron ore by 2019. But India’s government is under intense pressure to limit imports, encourage exports and lift foreign currency earnings.

Removing iron ore production and export bans, bottlenecks and hindrances seems to us a relatively straightforward move that could deliver more foreign exchange to India in a matter of months.

We maintain a close watching brief in the next few months for evidence of regulatory and governance changes, and increased production/exports.

Rising Indian exports will weigh on spot iron ore markets and prices relative to otherwise.

Mac Bank estimates that the withdrawal of Indian ore is worth $20 to spot. I think the problems of returning Indian ore to the market are greater than a “matter of months”. But within a year I reckon India could produce volumes in the 50 million tonnes plus range. At $50 per tonne cash cost that will add considerable pressure to spot prices.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.