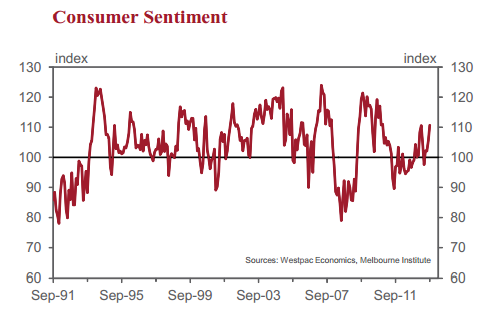

This is a very strong result. It is the highest print for the Index since December 2010. If sustained, it indicates that the Reserve Bank’s series of rate cuts which began in November 2011 are finally gaining strong traction with households. The Index has now increased by a respectable 13.8% since the Bank began cutting rates and it is now 9.9% above its average over the period since that first rate cut.

Of course the important new factor this month is the recent Australian election. Note that the survey was conducted over the period September 2 to 8. It was really only the last day of the survey that covered the actual election result although media coverage pointed strongly to a Coalition victory throughout the survey period. Responses collected on the last day of the survey showed a further marked lift in sentiment although the sample size is too small for this to be a statistically valid result. Suffice to say that the level of the Index over the first 6 days of the survey printed 109.7, slightly below the 7 day print of 110.6.

I think it is reasonable to conclude that the election result played an important if not leading role in this strong boost to Consumer Sentiment.

The result is comparable with the boost to the Index in March 1996 when the Coalition was returned after 13 years in opposition. On that occasion the Index jumped from 108.0 to 115.0 – a rise of 6.5%. That survey covered March 3 to March 9 following the election on March 2. As a result the whole survey covered a period when the election result was known.

As a further indicator that the election was a significant factor in today’s results we note that over the month the confidence of Coalition voters surged by 19.1% compared to a fall of 10.3% for ALP voters. That compared with comparable changes in 1996 of +25.3% and –17.2% respectively when the full result was known for the entire survey.

A concern for much of this year has been that while consumer sentiment has been steadily improving, even before today’s strong result, households’ assessments of job security has remained very weak. For example, while Consumer Sentiment had increased by 8.7% to August from the time when the Reserve Bank began cutting rates, households’ unemployment expectations had deteriorated by 9.6%. This wedge has vexplained some of the listlessness of consumer spending despite the improvement in Consumer Sentiment. For September, the Westpac Melbourne Institute Index of Unemployment Expectations fell from 152.7 to 142.6 – a 6.6% improvement in this measure of job security.

However, the Index is still 2.4% above the level of October 2011 indicating that households are still more concerned about rising unemployment than when the Reserve Bank first started cutting rates in November 2011.

The components of the Index indicate that the improvement in confidence is dominated by rising optimism about prospects for the economy rather than how households feel about their own finances. Looking across the five sub-indexes: those tracking views on ‘family finances vs a year ago’ and ‘family finances over the next 12 months’ fell by 1.9% and increased by 1.6% respectively whereas those tracking views on ‘economic conditions over the next 12 months’ and ‘economic conditions over the next 5 years’ increased by 8.7% and 7.1% respectively.

There was also more confidence about buying conditions with the sub-index tracking views on ‘time to buy a major household item’ up 6.9%.

Confidence is also high around the housing market. The sub-index tracking assessments of “whether now is good time to buy a dwelling” jumped 6.5% to its highest level since August 2009. Every quarter we also get a read on what major news items were recalled by respondents. In September, the economy dominated respondents’ attention with 52.5% recalling news items on this topic. Next most followed was ‘budget and taxation’ (27.9%) with international conditions (16.5%) and interest rates (15.6%) also figuring prominently.

There was considerable improvement across the board in perceptions of all these categories with the improved perceptions about news on the economy and interest rates standing out.

We also survey households’ assessments of the wisest place for savings. In September this showed a marked decline in the proportion of households who see ‘low risk’ options as the wisest place for savings. The proportion preferring bank deposits fell by 4.6ppts to 29.3%. That proportion is now down by 9.7ppts since September last year. The proportion favouring ‘pay down debt’ was down 2ppts to 13.8% and is now down by 6.7ppts since September last year.

At the same time the proportion favouring real estate rose from 24.6% to 27.5% with this now up by 7.7ppts since September last year. Even shares were marginally more popular, up from 8.4% to 8.8% and up 3.3ppts over the year.

The Reserve Bank board next meets on October 1. The Board will keep rates on hold at that meeting. There are a number of aspects to this survey that will give the Board encouragement that the series of rate vcuts, complemented by the confidence boost from the election make policy settings about right. However conditions around the labour market; business investment; and actual consumer spending are still soft and the Board will require more time to assess the underlying strength of the economy.

Looks like rate cuts are off for the foreseeable future.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.