The State Council, China’s cabinet, released a detailed plan on Thursday that aims to overhaul the country’s energy mix so that coal accounts for less than 65 per cent by 2017, down from just under 70 per cent.

To achieve that, the government said it would cut coal consumption and stop approving new coal-fired power plants in three key areas: Beijing and Tianjin in the country’s north, the Yangtze River delta around Shanghai and the Pearl River delta in Guangdong.

The plan’s release comes just a day after Premier Li Keqiang told high-level participants at the World Economic Forum in Dalian, north-eastern China, that environmental protection ranked alongside economic reform on his list of priorities. He said the government would use an “iron fist” to shut highly polluting and outdated factories.

…According to the plan, companies with poor environmental track records will be prevented from listing or raising finance. And local government officials will be judged on the improvement or deterioration of a province’s air quality. And the top 10 and worst 10 cities, in terms of air pollution, will be published in a list every month.

In the race to the lowest marginal cost of production that is closing its grip on all of Australia’s bulk commodity markets, spare a thought for thermal coal. It has led the way down with its boom time extrapolations of endless demand, its wasted shareholder capital, its over-supplied markets and assumption of rational market share responses.

Bank of America yesterday offered the following:

Advertisement

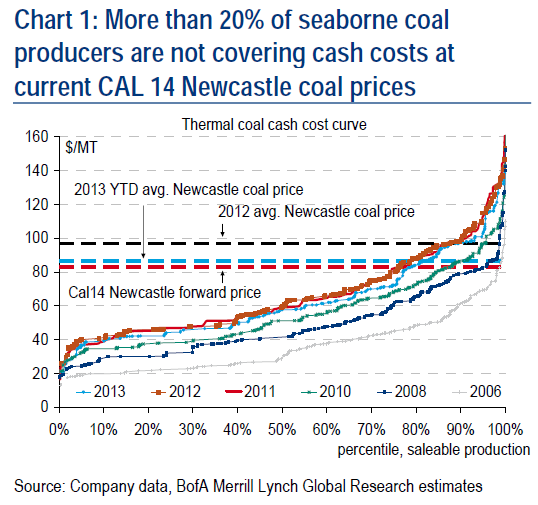

Seaborne thermal coal prices are hitting 4-year lows

After a gradual grind lower this year, thermal coal prices are sitting at very low levels. Ongoing mine ramp-ups, weaker producer currencies and a contango market structure suggest countries like Australia will remain slow at curtailing output. The fact that producers are still boosting coal production and exports is at odds with our updated global thermal coal cost curve. Despite a small downward shift in the cost curve in 2013 from last year, more than 20% of seaborne coal producers are not covering cash costs at current prices. We are lowering our forecasts for Newcastle thermal coal in 4Q2013 to $74/mt, from $84/mt prior, and in 2014 to an average of $82/mt, from $91/mt prior.

EPS impact: WHC into loss 2014; BHP & Rio modest trim …

On the back of our pricing cuts, WHC’s earnings have turned –ve in 2014 and modestly trimmed in 2015. BHP and Rio have only incurred modest earnings trims – Rio in 2013 and 2014 vs BHP in 2014 and 2015 (Table 1-4).

Lacklustre demand for coal in EMs

Supply is looking solid, demand for seaborne coal around the world is based on a more wobbly footing. China was happy to soak up excess seaborne supply in recent years but will unlikely act as the swing buyer going forward as it is structurally trying to support its domestic coal industry. Near-term, seaborne demand should be restrained anyway as domestic prices have collapsed and the import arb is closed. Moreover, India is suffering from a freefall in its currency, potentially reducing its appetite for expensive cargoes of seaborne thermal coal from places like South Africa. Thus we believe that thermal coal prices have further to fall.

Fx to give some relief to Australian companies

For instance, Newcastle coal prices have fallen by 19% YTD but given the 12% depreciation of the AUD, local coal prices have only seen a decline of 7%. The same goes for South African coal. Richards Bay coal in USD has dropped by 19% YTD but ZAR-denominated coal has only fallen by 5%. With miners’ profitability protected by the depreciation of their currencies, we have yet to see any meaningful declines in production.

I agree. This bust is not over. I’ve previously called for a price bottom in the $65 range and I still think that’s where we’re going. Even lower is possible until a lot of production comes out, some of it Australian. How much will depend upon the above chart. Look at the huge cost inflation over the past seven years that it illustrates. Notice too that 2012 was the peak and 2013 has fallen slightly. Much, much more of that coming down the pipe.

China’s shift to more environmentally sensitive energy policies is better news on other fronts. The energy package is big, north of $2 trillion yuan, half the size of the GFC stimulus, so it will help slow the price crash coming in iron ore and support coking coal on its way down. Gas may benefit a little but I expect China to generate a lot of internal shale gas resources relatively soon. Uranium too may find more support. This is the main reason I upgraded my Australian outlook for the first half of next year yesterday.

Tony Abbott can learn from Chinese direct policies. Renewable energy capex prices are falling faster as Chinese production gets more efficient and it will be more and more cheap to follow China’s example when the world offers us no choice but to do so.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.