I’m going to have to admit to getting this wrong initially, I think. The Fed looks to have been spot on in its timing of taper discussions, and although I’ve been right that the US housing market is slowing dramatically and that bond yields are rising far too fast, it could not have been left to run without more serious consequences down the track, a la Alan Greenspan’s overly slow response in 2004/5.

The US data coming in continues to be strong. Last night the services PMI, the non-manufacturing ISM, surged again:

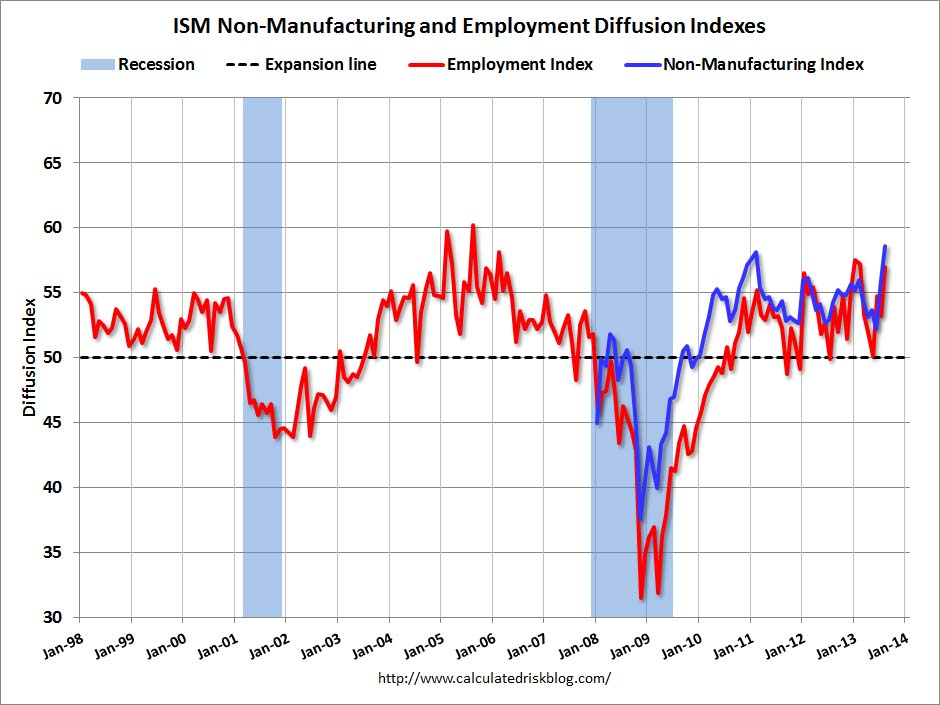

Economic activity in the non-manufacturing sector grew in August for the 44th consecutive month, say the nation’s purchasing and supply executives in the latest Non-Manufacturing ISM Report On Business®.The report was issued today by Anthony Nieves, C.P.M., CFPM, chair of the Institute for Supply Management™ Non-Manufacturing Business Survey Committee. “The NMI™ registered 58.6 percent in August, 2.6 percentage points higher than the 56 percent registered in July. This indicates continued growth at a faster rate in the non-manufacturing sector. This month’s NMI™ is the highest reading for the index since its inception in January 2008. The Non-Manufacturing Business Activity Index increased to 62.2 percent, which is 1.8 percentage points higher than the 60.4 percent reported in July, reflecting growth for the 49th consecutive month. The New Orders Index increased by 2.8 percentage points to 60.5 percent, and the Employment Index increased 3.8 percentage points to 57 percent, indicating growth in employment for the 13th consecutive month. The Prices Index decreased 6.7 percentage points to 53.4 percent, indicating prices increased at a significantly slower rate in August when compared to July. According to the NMI™, 16 non-manufacturing industries reported growth in August. The majority of respondents’ comments continue to be mostly positive about business conditions and the direction of the overall economy.”

That is wall to wall strength and is the highest reading since 2005. Chart from Calculated Risk:

Other data on the night was good as well. ADP Private Payrolls hit consensus:

Private sector employment increased by 176,000 jobs from July to August, according to the August ADP National Employment Report®. … July’s job gain was revised down slightly from 200,000 to 198,000….Mark Zandi, chief economist of Moody’s Analytics, said, “It is steady as she goes in the job market. Job gains in August were consistent with increases experienced over the past two-plus years.”

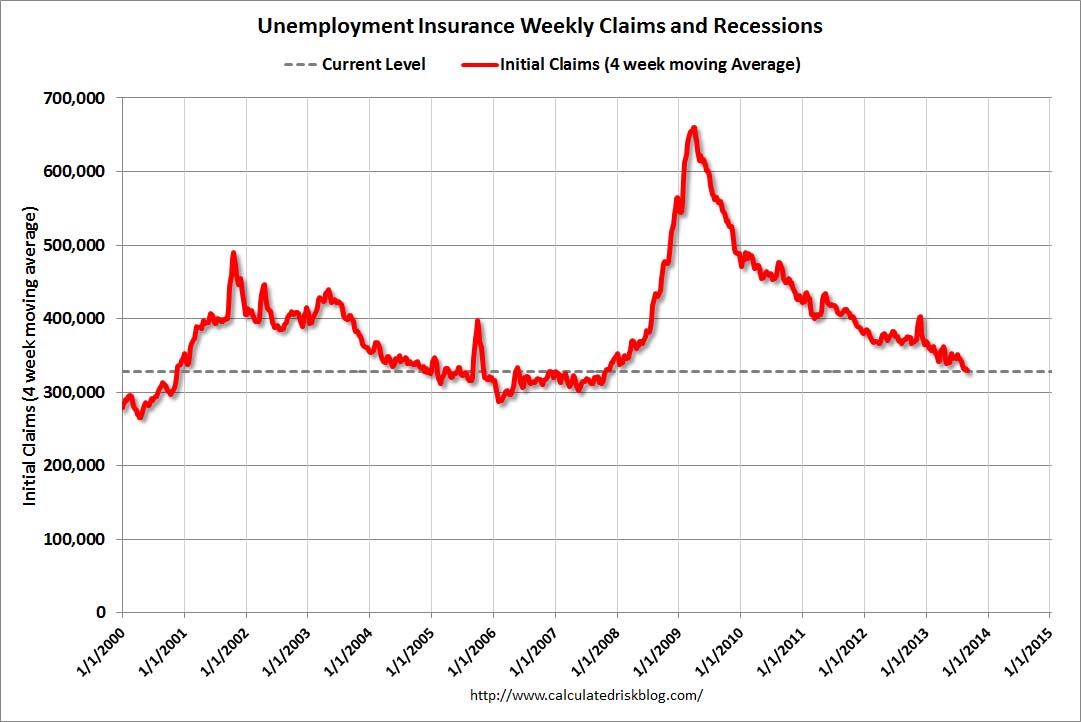

This is hardly tearaway and is the fly in the taper timing ointment. ADP has never been a great guide to the official employment report, released tonight from the BLS, but it’s holding up and that will likely be enough for the Fed. Also last night, weekly DOL inintial unemployment claims fell again:

In the week ending August 31, the advance figure for seasonally adjusted initial claims was 323,000, a decrease of 9,000 from the previous week’s revised figure of 332,000. The 4-week moving average was 328,500, a decrease of 3,000 from the previous week’s revised average of 331,500.

Again the chart from Calculated Risk:

So, data is increasingly looking good enough for the Fed to dip its toe into some tightening. It won’t be swift or large, I suspect, but it doesn’t need to be when the bond bubble is deflating so quickly. Last night, 10 year yields rocketed 3% to a new high of 2.98%. 30 year yields are poised to break out as well, rising 2% to 3.88%.

The tightening has already happened. There is nothing to stop the Fed from making it official.

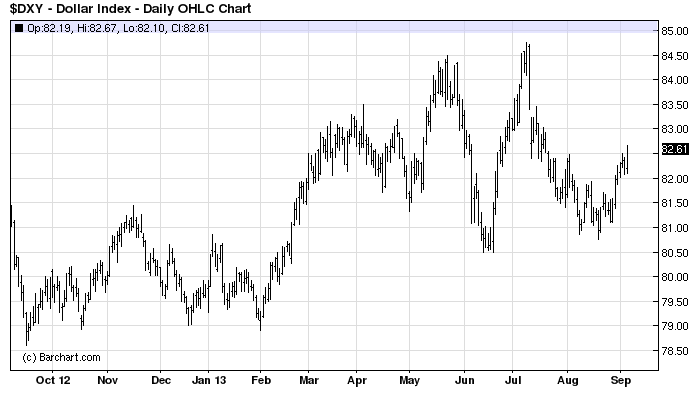

What does it bode for markets? Despite the safe haven unwind, a rising US dollar is surely a real chance. It leaped last night, remains in an uptrend and has plenty of headroom:

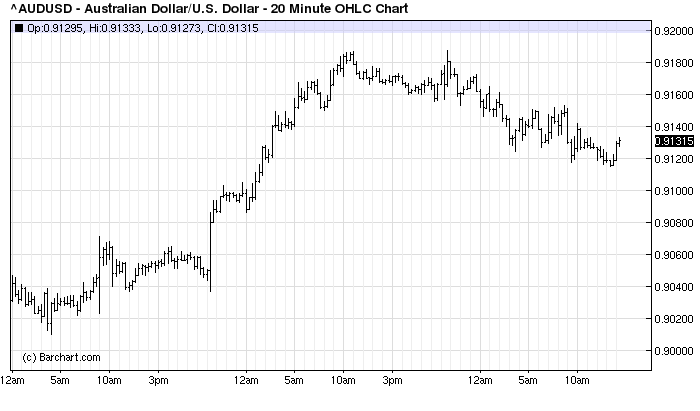

And, thankfully, it will be damn near impossible for the Aussie to make any headway as this environment develops. It was down a half cent last night, with more to come if the Fed pulls the trigger:

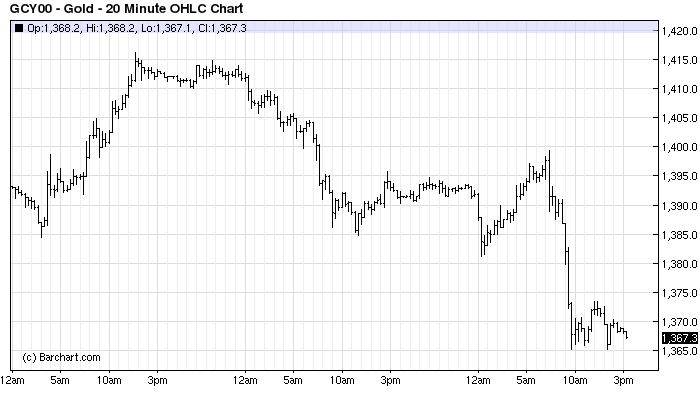

Gold got poll-axed:

The stock market has held up well in recent weeks but I’d be wary of that continuing.

All in all, US activity remains short of most of the Fed’s thresholds for tapering and it is going to slow on rising bond yields but, supported by the moderate developed economy recovery currently underway, the Fed is right to taper and to do it now.