Cross-posted from Kate Mackenzie at FTAlphaville.

A little over half of China’s population is urbanised, and the country’s leaders plan to urbanise vast numbers of people over the next decade – although both the time frame and the number of people in the plan vary, depending where you look —both 260m and 400m have been widely reported.

More clarity is expected at the Third Plenum of the 18th Central Committee of the Communist Party of China, probably in October. But could the country already have an excess of cities?

First up, a fascinating story from the WSJ:

Among the few business owners lured to a development park in Tieling New City is Bo Yuquan, the middle-aged owner of a flooring store.

“Where are the people? There’s no one here,” said Mr. Bo. “I’ll be out of business soon. My staff and I are discussing moving to Beijing to find work.”

Said Hu Jie, the designer of the new city’s landscape: “In 10 to 20 years, Tieling could be a good development, but only if you can manage to bring businesses in.”

A city can certainly be sustainable if businesses start to pop up — but how does that happen, and what if it doesn’t? Jobs, naturally, can be a problem in this situation; a fact illustrated in the NY Times report on the recently-designated town of Qiyan, where high-rise housing for 6,000 replaced a village of about 200 households (residents from surrounding areas were encouraged to move there, too). A lack of jobs meant residents in newly-constructed Qiyan homes huddled around open fires for warmth because they couldn’t afford electricity.

Okay, then, maybe Tieling and Qiyan are messed up, but so what — we’ve heard it all before, right — maybe they, along with the famed case of Ordos, are just outliers? China’s build-first approach hasn’t always gone drastically wrong. As the WSJ notes, “the towering new Pudong business district” was empty when built a decade ago, but later became a “symbol of China’s success”.

On the other hand, is it Pudong that is the exception and Ordos that is the norm, or at least a more common scenario in China’s many smaller cities? Hard data is hard to come by, but the WSJ asserts that the build-now-wait-for-growth strategy has “thrown up empty suburbs and ghost cities like Tieling New City across the country”.

A big Chinese developer also believes this is the case. From Bloomberg:

Mao Daqing, executive vice president of China Vanke Co., the biggest developer by market value traded on the country’s stock exchanges, told the forum some local governments may be hard pressed to pay for urbanization.

Taking Beijing as an example, Mao said that assuming 700,000 people moved into the city each year, it could cost the local government at least an extra 77 billion yuan a year in urbanization-related spending, equivalent to doubling its annual land sales or a 25 percent increase in tax revenue.

“This is totally beyond the affordability of a local government, Beijing can’t afford it,” Mao said. He also questioned whether China needs more cities when most migration has been to the 70 biggest conurbations.

“These big cities interest people because they have more job opportunities, education opportunities and medical resources,” Mao said. “Those other 610 cities can’t attract people even though they already exist,” he said, adding “it indicates some of those 610 cities have problems or can’t survive.”

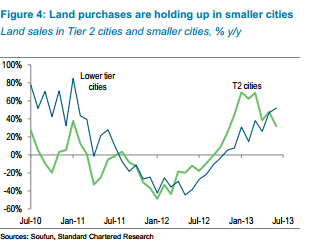

Data that would confirm whether Qiyan, Ordos, and Tieling New City, are common or outliers is very hard to come by, as Standard Chartered’s Stephen Green acknowledges. Green last month sought to gauge the health of the real estate market in the top three tiers of Chinese cities, and concluded that the picture is not so bad. He writes: “despite a few other ‘ghost city’ stories, the picture in smaller cities looks resilient”.

However Green’s focus has a couple of shortcomings for gauging the overall success of urbanisation. Firstly, two of his three methods of analysing real estate only look at the 30 – 40 biggest cities. The third method, which uses data on 300 cities, does find some problems in Tier 2 cities, but shows purchases by developers are holding up in the smaller cities:

Green infers this means there is confidence among developers about the demand outlook. That may be right, but for a couple of reasons none of this disproves the suggestions from China Vanke that the country may have an ‘oversupply’ of smaller cities. That’s partly because there are almost 400 cities not covered in the above chart, but also because the sale of apartments doesn’t necessarily say a lot about whether they will ultimately facilitate the economic, and social, development of the city

Many of China’s apartment sales are essentially forced because villagers’ land is seized and houses razed, plus the question is about what “urbanisation” means in many of these cities. For example, the family in Qiyan who spoke to the NYT mentioned the crippling debt they now held (their daughter had to quit college and take a sales job to help them repay their debt).

Plenty of growth was generated through the building of the apartments, the purchasing of the apartment and their now-unused TV but that might simply be misallocation. The central government’s “fast-track” urbanisation plans, with the apparent focus on smaller cities, may guarantee more such purchases — but if people can’t get jobs there, it’s not “urbanisation” in the way it is usually understood.

Which is what China Vanke’s Mao Daqing is getting at. It’s something that has been illustrated by Jinsong Du, Duo Chen, and Parker Ding at Credit Suisse in March. They wrote (our emphasis):

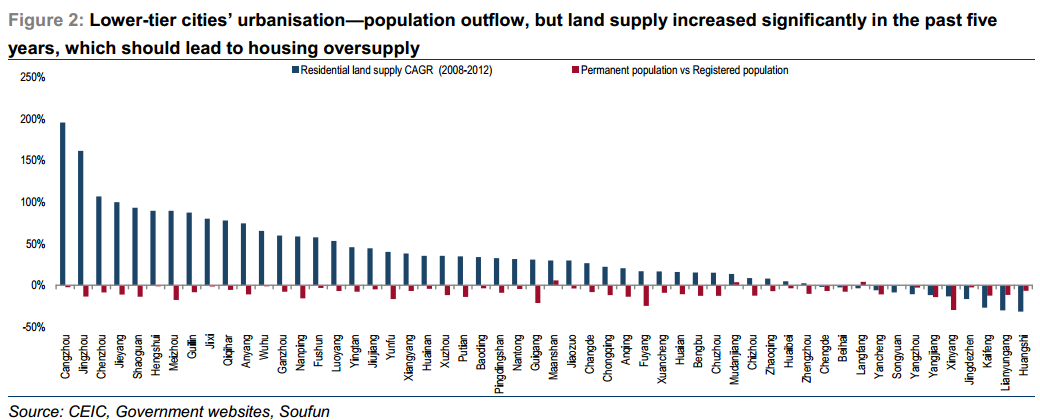

While common sense assumes China’s urbanisation pertains to rural people migrating to cities, the reality is quite different. Government official data shows that only a third of the newly urbanised population is migrant workers from the countryside. The remaining two thirds are mostly locally urbanised people, i.e., the city area has expanded to where they live. With more and better job opportunities in higher-tier cities, many lower-tier cities have actually been experiencing a net outflow of population while land sales there increased rapidly exacerbating the housing oversupply. Among the 287 cities that we managed to collect data on, only 97 (or 1/3rd) have more permanent residents than registered residents (or “local people”, i.e., those with a hukou (formal residence registration)). This means two-thirds or 190 of those cities may have experienced population net outflow.

Here’s a chart displaying some of those cities that experienced both population outflows, and big increases in land sold to developers:

Du and colleagues charted all the 287 cities but it’s much too big to fit here, so you’ll have to look in the usual place.

If the lack of sustainable income means residents spend 11 months of the year living in bigger cities, then as we explained in last year’s ‘China Myths’ series, it isn’t really the kind of growth that brings about sustained consumption, job creation and a “middle class”. This is largely due to the household registration system known as ‘hukou’, meaning those migrants to bigger cities exist there as second-class citizens.

While there have been reports of hukou reform, details remain vague and there are powerful forces set against deep changes to the system. From Bloomberg, again:

“Nobody wants such a big group of migrants to be their neighbors and share their so-called civilized space. This is a conflict of interest,” Li, director-general of the China Center for Urban Development under the National Development and Reform Commission, said at the forum on Aug. 10. “We are facing rejection from the hearts of so many mayors and city elites who have enough ability to influence decision making.”

This raises questions about whether one can create a more “developed” economy simply through moving more and more people into new apartment buildings — even if, as in Tieling New City, the local water supply is cleaned and appealing development parks are provided to attract businesses.