Macquarie Bank offers a useful little study of thermal coal today in which is asks why despite low prices production remains robust.

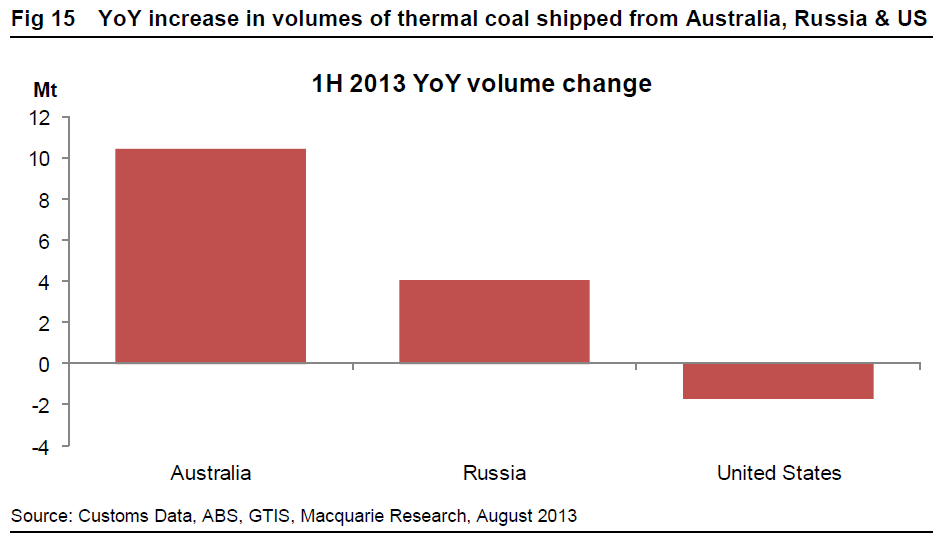

Total export volumes from the three highest-cost major producers were up 13mt YoY, with cuts from the US alone not anywhere near enough to provide greater balance to the market (Fig 15). While spot Newcastle prices remain above $75/t, we are unlikely to see much Australian supply cut. Furthermore, while Russia remains somewhat of a black box, a combination of structural factors appears to be mitigating lower prices.

We see the following elements as being more significant for the market balance:

Of the major suppliers, it currently appears that Indonesia is most likely to cut supply (or at least significantly slow supply growth). Although its output is generally considered low-cost, on an energy-adjusted basis some of the sub-bituminous tonnes are in fact marginal and government proposals to hike royalties on IUP holders – which we believe is likely to be implemented – would push many of the smaller producers out of the market in the medium term.

In China, lower domestic prices have helped to price out some domestic production. China‟s YTD output is down around 4% YoY, led by cuts from Inner Mongolia where trucked tonnes are currently cash negative. Continued falls in domestic production would further open the Chinese contestable market to imports.

Overall, while the market balance is unlikely to get significantly worse and demand-side indicators from India and China have been looking positive and improving respectively, it will certainly take a decent period of time to work through the current level of market oversupply.

Macquarie notes that:

Russia is the world’s third largest thermal coal exporter; it is also one of the highest cost suppliers globally. For illustration, spot thermal coal prices averaged just $78.5/t in the first half of the year basis 6000kcal NAR FOB Murmansk – the benchmark specification for coal from Russia‟s largest Atlantic coal port. Yet it is estimated that in 2012 around 80% of Russia‟s exported thermal coal was supplied at a cash cost in excess of $80/t FOB. Basic economics dictates that production and hence exports should come down in this environment.

But, Macqurie goes on, there several factors likely at work that lower this assumed cost including axes and charges can be lifted. US volumes are falling but only slowly.

Advertisement

None of this is a surprise to me. Other nations do not take kindly losing business and nearly always find ways of slowing the process, despite the hopes of Australian miners who appear to have hugely over-invested.

I expect the same drawn out pain for coking coal and, more importantly, for iron ore beginning H1 next year (not that that is an issue now!)

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.