Standard and Poors is out with another in its series of notes examining the potential fallout from deteriorating Chinese credit metrics.

China’s recent investment boom has left its corporate sector with a large debt hangover. Since the onset of the Global Financial Crisis, China’s top corporates have had easy access to credit, which has fuelled their strong investment levels. The country’s new administration, however, is attempting to put the economy on a more sustainable footing. To achieve this goal, it aims to steer the economy away from the previous investment-led growth model to a more balanced framework that includes higher levels of consumption.

China’s top corporates have been struggling with declining profitability amid increasing borrowings since 2008. They now face the challenge of managing their highly leveraged balance sheets amid slower economic growth rates. In this more challenging environment, Standard & Poor’s Ratings Services believes the capacity of China’s corporates to service their high debt levels has diminished compared with a year ago. However, some companies and sectors are likely to weather the downturn better than others, which is likely to lead to increased differentiation among China’s top corporates’ credit profiles.

Overview

China’s top 151 corporates accumulated high debt levels during the credit boom of the past five years. Facing lower economic growth and tighter profit margins, we believe they now have a reduced capacity to service their debt.

We believe the financial strength of the majority of these corporates will weaken further in the next 12 months. A sizeable minority with highly leveraged balance sheets and continued high investment appetites remain particularly vulnerable in the current slowdown.

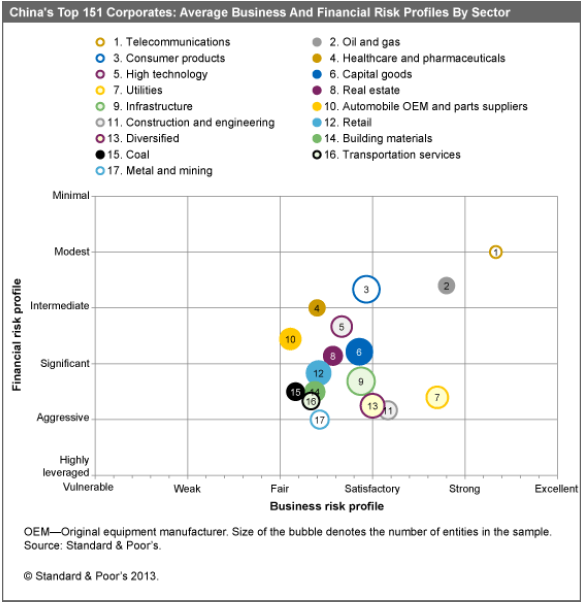

The impact of the slowdown on China’s industry sectors is likely to be uneven. In our view the better-placed sectors are telecommunications, oil and gas, consumer products, and healthcare and pharmaceuticals.

On the other hand, sectors struggling with overcapacity–such as building materials, coal, transportation, and metal and mining–are more exposed. The steel subsector is especially stressed by overcapacity and is vulnerable to potential government policy changes.

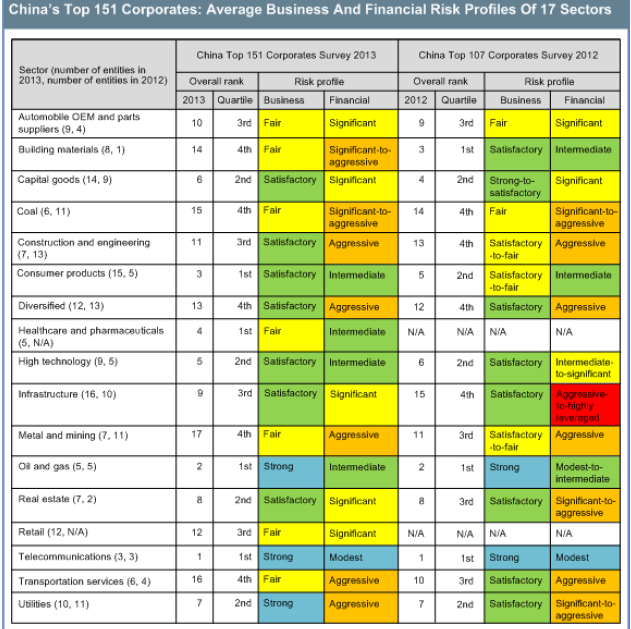

For this 2013 China Top Corporates survey, we have selected 151 major Chinese companies from a pool of the largest domestic bond issuers and biggest revenue-earners, as well as companies that we believe are representative of their industries. We have chosen a diverse sample to gauge the general credit strength of the significant industries in China. We believe the majority of the 151 corporates that we analyze in this survey are likely to weather the current economic slowdown. However, a sizeable minority of the companies in this survey have “aggressive” to “highly leveraged” financial risk profiles (these are the two lowest categories in our six-point scale for financial risk; see chart 1 for the six-point scales we use to assess companies’ financial and business risk profiles). We think these corporates will be more vulnerable in this more challenging operating environment.

As in our 2012 survey of China’s top corporates, the telecommunications and oil and gas sectors are the two strongest performers in this year’s survey (see chart 1).

Companies in these two sectors benefit from their oligopolistic market positions and strong financial positions. We regard the building materials, coal, construction and engineering, diversified, metal and mining (including steel), transportation, and utilities sectors as those with high financial risks.

Some of these sectors are struggling with excess capacity and depressed profitability. To promote consolidation in these industries, we believe the government may intervene to remove excess capacity by asking some state-owned enterprises (SOEs) to acquire weaker entities.

For the diversified, construction and engineering, and utilities sectors, financial risks are partially counterbalanced by their “satisfactory” or “strong” business risk profiles. Their business risk profiles reflect their good-to-strong market position, which, however, does not preclude weak or low profitability due to excess capacity. Pricing power for many companies in these sectors remains very limited.

If you have ever wondered why many top global hedge funds consider Australia a leveraged play on a Chinese slowdown then these charts should clarify it for you. Steel, infrastructure, and real estate all appear extended.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.