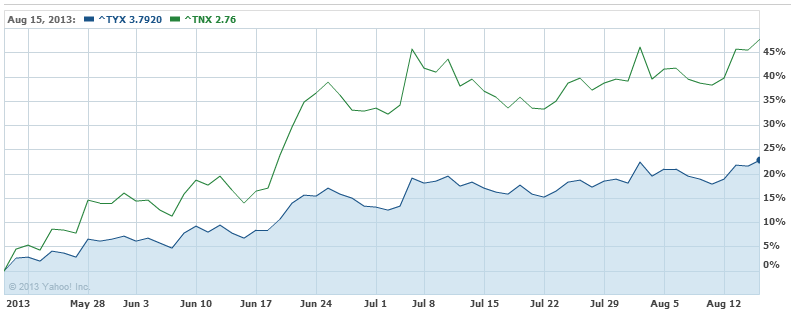

The talk today in markets is all about the bond outflows that are gathering pace as the US taper looms. Last night US 10 year and 30 year yields both spiked to new highs despite pretty mediocre data:

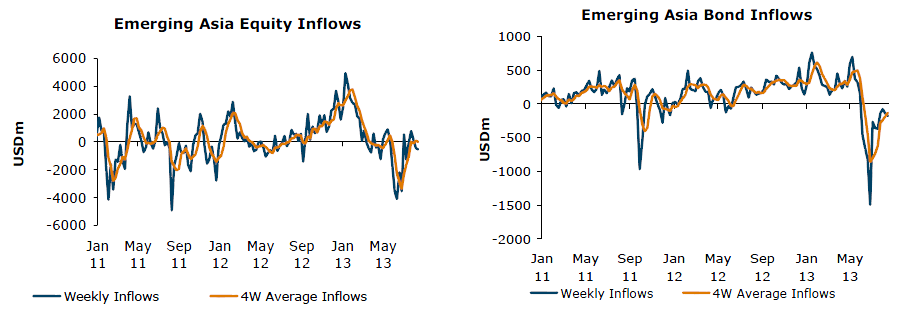

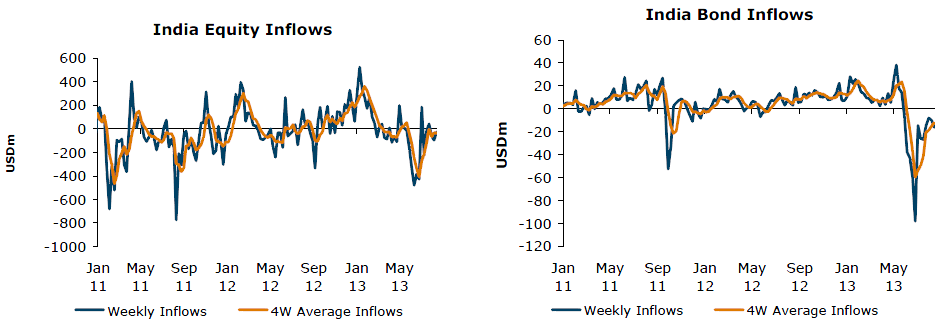

The steepening in shorter term yields is causing all sorts of trouble for emerging markets, which have themselves enjoyed strong bond and equity flows throughout the northern hemisphere crises, but are now reversing. ANZ has a neat document showing the carnage over the past week:

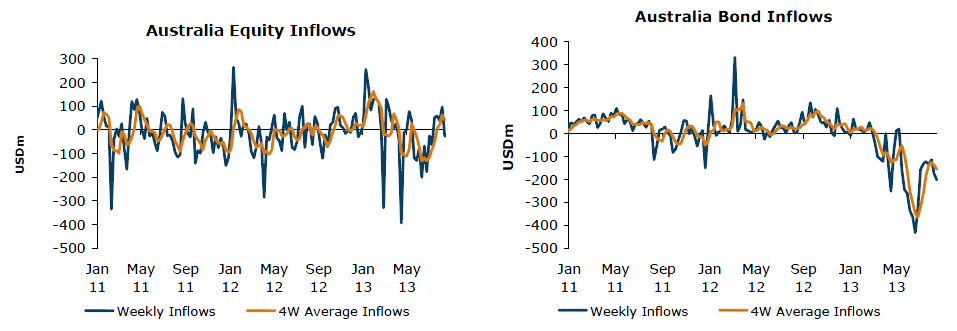

However, a special place seems to be reserved for that darling of the safe haven flows, the Australian bond market, which is getting absolutely crucified:

This helps explain why we have a run out of emerging markets yet no run into US assets. Hence the US dollar is so far not benefiting from the taper, as many including me thought it would. Perhaps in time as these flows subside normalcy will return.

This in turn helps explain why the Australian dollar is not falling as you might expect that it would in these circumstances. Markets have all but priced out further rate cuts as well.

Basically, the major safe haven trades are unwinding simultaneously, except for gold, which has already unwound and is now enjoying the weakening US dollar.