As analysts and official entities like the World Bank continue to downgrade their forecasts for medium-term growth in China, I have been asked increasingly often for the reasons I believe that 3-4% average annual growth rates is likely to be the upper limit for China during the adjustment period, In this issue of the newsletter I want to explain how I arrived at my numbers. The analysis is fairly straightforward and those looking for a very complex econometric model are likely to be disappointed, but I have always believed that, unlike physics or cooking, anything in economics that cannot be easily explained to an educated layman with 9th-grade algebra and a little bit of calculus is likely to be useless (and if he knows some probability theory, the most beautiful branch of math in my opinion, he is able to soar).

Before beginning I should make two points. First, for many years I assumed that the “adjustment” period would begin shortly after the beginning of the administration of President Xi Jinping and Premier Li Keqiang, that is, from 2013 or 2014, and would run through the presumed end of their term in 2023.

In fact I may have been overly pessimistic. It now seems to me that China actually began adjusting economically, although in a very limited way, in 2012, when we first started to see growth slow as Beijing became increasingly worried about the astonishing increase in debt.

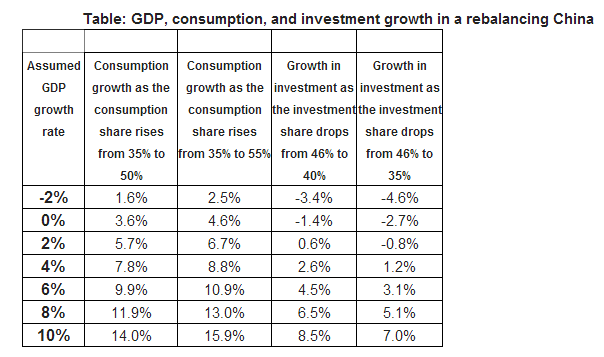

Under specified rebalancing assumptions for China it is possible to calculate arithmetically the annual growth rate for consumption and investment under different GDP growth scenarios. This allows us to decide whether these scenarios are plausible or not.

If we believe, for example, that China’s GDP growth during President Xi Jinping’s administration (2013-23) is likely to range on average between 6% and 8%, and if we believe that China has ten years to rebalance by the minimal amount necessary to approximate levels similar to those of countries at its level of development, we are implicitly assuming that household consumption will grow by 10-12% a year on average and investment will grow by 4-5-6.5%. Although these numbers are not impossible, I believe the debt growth needed to achieve this level of investment growth over a decade – starting from such an astonishingly high base – is unsustainable.

More importantly, absent a massive, and politically unlikely, transfer of wealth from the state sector to the household sector, I do not think it is possible for household consumption to grow at 10-12% a year for ten years, especially because growth in household consumption is correlated with investment growth, especially in the inland provinces, on which the most wasteful investment seems to be lavished, and such a sharp decline in investment growth will make it hard for household consumption growth to surge to these levels.

Assuming the same minimum level of rebalancing, 3-4% GDP growth implies that household consumption will grow by 7-8% a year on average and investment will grow by less than 2.5%.

It will not be easy to maintain this level of consumption growth, but it can be attained in principle. However this suggests that 3-4% GDP growth over the presumably 10-year administration of President Xi is likely to be the upper limit for a rebalancing Chinese economy.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.