This week will see a major update to Australia’s capex profile with the release Wednesday of the quarterly ABS capex report. Mac Bank has a short note today describing why some in the market are more sanguine about this than others:

There are two key concerns still floating through the minds of investors and analysts alike. First, how quickly will mining investment decline over the next year, and second, if investment outside of the resource sector is capable of offsetting the negative impact to growth. Normally, the Capex survey has the potential to provide powerful insights into both of these questions. In our view, however, the June quarter survey‟s usefulness may be limited.

Analysis

Normally, each Capex survey contains estimates for two financial years, but this week‟s release will contain the 7th (final) estimate for total private business investment for FY12/13 and the 3rd estimate for Y13/14. For FY12/13, planned Capex is expected to be around $160b, which could have been deduced quite easily from the 6th estimate given that data for 3 out of the 4 quarters of the FY12/13 were also available at this time.

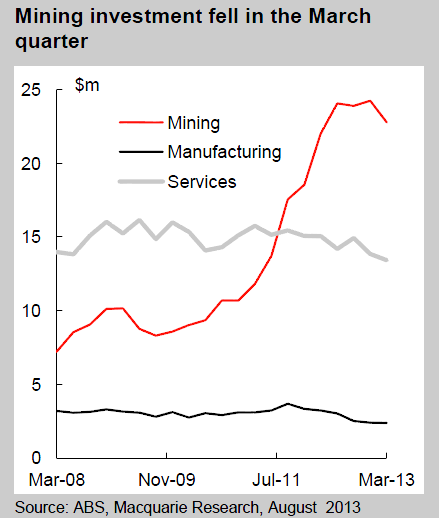

With investment falling in the December and March quarters, and an implied decline in spending in the June quarter as well, it seems clear that business investment is on a declining trend for FY13/14. But while we think this is perfectly clear, that view is not held universally.

This is because there are different ways of interpreting the published investment plans. Specifically, analysts can use either an average realisation uplift ratio or simply compare corresponding estimates to previous years. Using the latter leaves us with investment falling around ~10% which is consistent with what actual activity has been over the past 6 months. Using the former method, however, results in an investment outlook which is less pessimistic.

The giveaway to the deceiving nature of the realisation ratio is its inaccuracy when applying it to FY12/13 Capex 6 months ago. When this is done, growth in Capex in the year computes to 12%, rather than the 3% it will most likely be. With this in mind, analysts should be asking themselves whether mechanically applying average realisation ratios is a sensible thing to do when determining the realistic outlook for investment.

You will find all of the bullish forecasters using the average realisation ratio which is perhaps defensible in some petri-dish of intellectual perfection but has little to do with what’s actually happening out here in the real world this year. Year on year is the best representation when deviating from trend.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.