Credit Suisse offers a new explanation for the current iron ore bounce today:

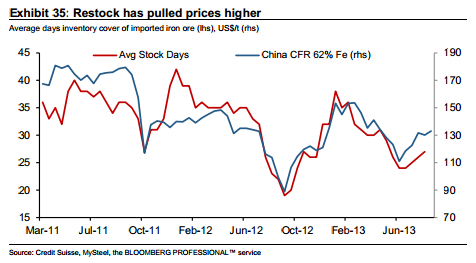

Iron ore’s spot price rally has continued to defy our earlier expectations, with mills’ restocking supporting a series of particularly strong physical tenders over the past few days.

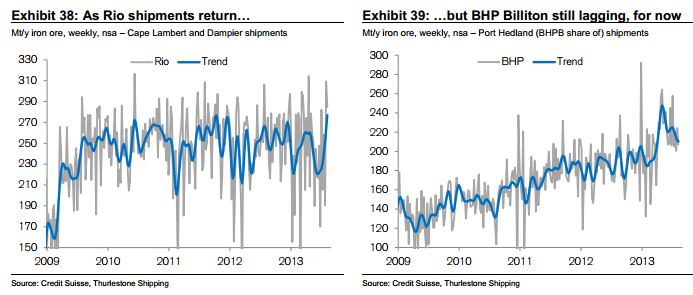

Crucially, this restock has come during a period of uncharacteristically weak Australian supply – the previously-flagged June softness has now been confirmed by the official trade data. More recent shipping numbers point to a gradual recovery in volumes but April’s heights are yet to be regained.

An end to maintenance at Rio’s ports has seen its shipments already moving higher and the upcoming advance in deliveries – due to start in September – should mean this trend continues. At Port Hedland, however, BHP Billiton’s volumes still appear to be falling back.

This is not a trend we expect to continue, as it should merely represent a pull back from the jump higher in Q2, when the company appears to have destocked 1-2 Mt of inventory.

Were shipments to run in-line with output, supplies should mimic longer-term trend growth over coming weeks, with the greatest likelihood a move higher in Q4 when the 35 Mt/y Jimblebar expansion should begin adding tonnage to the market.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.